Risk Management Is Not Protection... It’s Your Edge!!!Most traders treat risk management like a seatbelt.

Something you use just in case.

🧳Professionals treat risk management as their main edge.

Because in trading, you don’t get paid for being right...

you get paid for staying in the game long enough for probabilities to work.

1️⃣ Risk Is Defined Before the Trade Exists

Before you think about entries or targets, one question must already be answered:

Where am I wrong?

If you don’t know where your idea fails,

you’re not managing risk... you’re hoping.

Professionals define risk first.

The trade only exists after invalidation is clear.

2️⃣ Small Risk Creates Big Freedom

When risk is small and predefined:

- hesitation disappears

- emotions calm down

- execution improves

Why?

Because no single trade matters anymore.

You stop needing trades to work, and that’s when trading becomes objective.

3️⃣ Risk Management Turns Losses Into Data

Losses are unavoidable.

Damage is optional.

A controlled loss is not a failure; it’s information.

Every loss tells you:

- the market condition wasn’t right

- the timing was early

- or the structure changed

When risk is managed, losses educate instead of punish.

4️⃣ Consistency Is Built on Risk, Not Wins

Winning streaks feel good.

They don’t build careers.

Surviving losing streaks does.

Proper risk management ensures:

- drawdowns stay shallow

- confidence stays intact

- discipline stays repeatable

That’s how traders last long enough to improve.

💡The Real Truth

You don’t need a better strategy.

You need better control over downside.

Risk management is what allows:

- imperfect strategies to work

- average win rates to grow accounts

- traders to evolve instead of quit

⚠️ Disclaimer: This is not financial advice. Always do your own research and manage risk properly.

📚 Stick to your trading plan regarding entries, risk, and management.

Good luck! 🍀

All Strategies Are Good; If Managed Properly!

~Richard Nasr

Wave Analysis

Global Soft Commodity Trading: Dynamics and StrategiesUnderstanding the Global Soft Commodity Market

Soft commodity markets operate on a global scale, with production concentrated in specific regions and consumption spread worldwide. For example, coffee production is dominated by Brazil, Vietnam, and Colombia, while cocoa largely comes from West African nations such as Ivory Coast and Ghana. Sugar production is led by Brazil and India, whereas wheat and corn are heavily produced in the United States, Russia, and parts of Europe.

This geographical imbalance between producers and consumers makes international trade essential. Prices are generally discovered on major commodity exchanges such as the Chicago Board of Trade (CBOT), Intercontinental Exchange (ICE), and Euronext. These exchanges provide standardized futures and options contracts that allow producers, consumers, traders, and investors to hedge risk or speculate on price movements.

Key Drivers of Soft Commodity Prices

Soft commodity prices are influenced by a wide range of interconnected factors:

Weather and Climate Conditions

Weather is the single most important factor affecting soft commodities. Droughts, floods, cyclones, frost, and changing rainfall patterns can significantly impact crop yields. Climate phenomena such as El Niño and La Niña often cause global supply disruptions, leading to sharp price volatility.

Supply and Demand Dynamics

Changes in population, income levels, dietary habits, and industrial usage directly affect demand. For instance, rising coffee consumption in Asia or increased ethanol production boosting corn demand can alter global price trends.

Government Policies and Trade Regulations

Export bans, import duties, subsidies, and minimum support prices play a crucial role, especially in emerging economies. Policies in major producing countries like India, Brazil, or the United States can influence global supply availability and price stability.

Currency Movements

Since most soft commodities are priced in U.S. dollars, fluctuations in currency exchange rates impact international trade. A weaker dollar generally supports higher commodity prices, while a stronger dollar can suppress demand.

Logistics and Geopolitical Factors

Transportation costs, port congestion, trade routes, and geopolitical tensions can disrupt supply chains. Conflicts, sanctions, or shipping bottlenecks often translate into sudden price spikes.

Market Participants in Soft Commodity Trading

The global soft commodity market includes diverse participants, each with different objectives:

Producers and Farmers use futures contracts to hedge against adverse price movements and protect their income.

Processors and End Users such as food manufacturers and textile companies hedge to stabilize input costs.

Traders and Merchants act as intermediaries, managing storage, transportation, and arbitrage opportunities.

Speculators and Investors, including hedge funds and institutional investors, aim to profit from price movements and market trends.

Retail Traders increasingly participate through online platforms offering commodity derivatives and ETFs.

Trading Instruments and Strategies

Soft commodities can be traded through several financial instruments:

Futures Contracts are the most common, providing standardized exposure to commodity prices.

Options allow traders to manage risk with limited downside.

ETFs and ETNs offer indirect exposure for investors who do not wish to trade futures directly.

Spot and Physical Trading is mainly used by large commercial participants.

Successful soft commodity trading often relies on a blend of strategies:

Fundamental Analysis, focusing on crop reports, weather forecasts, acreage data, and inventory levels.

Technical Analysis, using price charts, trends, support-resistance levels, and momentum indicators.

Seasonal Trading, which takes advantage of recurring patterns related to planting and harvesting cycles.

Spread Trading, involving the price difference between related commodities or different contract months.

Risks and Volatility in Soft Commodity Markets

Soft commodities are known for high volatility due to their dependence on uncontrollable natural factors. Sudden weather changes or policy announcements can cause rapid price movements. Additionally, leverage in futures trading can amplify both profits and losses. Effective risk management through position sizing, stop-loss strategies, and diversification is essential for long-term success.

Another key risk is market uncertainty due to climate change, which has increased the frequency of extreme weather events. This has made price forecasting more challenging, increasing both risk and opportunity for traders.

Role of Emerging Markets and Sustainability

Emerging markets play a growing role in global soft commodity trading, both as producers and consumers. Rising incomes in Asia and Africa are driving demand for food commodities, while technological advancements are improving agricultural productivity.

Sustainability and ESG (Environmental, Social, and Governance) considerations are also reshaping the market. Ethical sourcing, carbon footprints, and sustainable farming practices increasingly influence investment decisions and trade flows. Certifications such as Fair Trade and organic labeling are becoming important price differentiators in global markets.

Future Outlook of Global Soft Commodity Trading

The future of global soft commodity trading is expected to be shaped by several long-term trends: climate variability, population growth, technological innovation in agriculture, and digitalization of trading platforms. Data analytics, satellite imagery, and AI-driven weather models are enhancing market transparency and decision-making.

At the same time, increased financial participation is likely to keep volatility elevated, offering both risks and opportunities. Traders who can combine strong fundamental understanding with disciplined technical execution will be better positioned to navigate these evolving markets.

Conclusion

Global soft commodity trading is a dynamic and multifaceted market that reflects the intersection of nature, economics, and finance. From coffee and cocoa to grains and sugar, these commodities are essential to everyday life and global trade. While the market carries significant risks due to volatility and uncertainty, it also offers substantial opportunities for informed and disciplined traders. A deep understanding of global supply chains, weather patterns, policy impacts, and market behavior is essential for success in the ever-evolving world of soft commodity trading.

A Strategic Approach to Profiting from Market InformationNews Trading Without Noise

In modern financial markets, news travels faster than ever. Economic data releases, central bank statements, corporate earnings, geopolitical developments, and even social media posts can move prices within seconds. While news creates opportunities, it also creates noise—misleading signals, emotional reactions, rumors, and short-term volatility that can trap unprepared traders. News trading without noise is the disciplined practice of extracting high-quality, actionable information from news while filtering out distractions, overreactions, and irrelevant data. This approach allows traders to participate in major market moves with clarity, confidence, and consistency.

Understanding the Difference Between News and Noise

Not all news is equal. Markets react strongly only to information that changes expectations. Noise, on the other hand, consists of repetitive commentary, speculative opinions, exaggerated headlines, and minor developments that do not materially alter fundamentals. For example, a central bank interest rate decision that deviates from expectations is meaningful news, while repeated media debates about possible outcomes before the announcement are often noise. Successful news traders focus on what is new, unexpected, and impactful, rather than what is loud or popular.

Noise is dangerous because it triggers emotional trading—fear of missing out (FOMO), panic selling, or impulsive entries. News trading without noise requires emotional detachment and a rules-based mindset, where decisions are driven by predefined criteria rather than instant reactions.

Focusing on High-Impact News Events

A noise-free news trading strategy begins with selectivity. Traders should focus only on high-impact, scheduled, and well-defined events such as:

Central bank interest rate decisions and policy statements

Inflation data (CPI, PPI), employment reports, and GDP figures

Corporate earnings from market leaders

Major geopolitical events that affect global risk sentiment

Low-impact data releases and speculative breaking news should be ignored unless they directly affect market expectations. By limiting attention to a small set of powerful events, traders reduce cognitive overload and improve decision quality.

Trading Expectations, Not Headlines

Markets move based on the gap between expectations and reality. A positive news headline does not always lead to rising prices if the market had already priced in better outcomes. News trading without noise means understanding consensus forecasts, market positioning, and sentiment before the event.

For instance, if inflation data comes in high but slightly below expectations, markets may rally despite inflation remaining elevated. Traders who focus only on the headline number may misinterpret the move, while those who analyze expectations understand the true driver. This expectation-based approach helps traders align with institutional flows rather than fighting them.

Using Price Action as the Final Filter

Price action is the most reliable filter against noise. Before acting on news, traders should observe how the market reacts in the first few minutes or hours. Strong, sustained moves with high volume often indicate genuine institutional participation, while sharp spikes followed by quick reversals usually signal noise-driven volatility.

News trading without noise does not mean reacting instantly. Instead, it means waiting for confirmation. Breakouts above key resistance levels, breakdowns below support, or continuation patterns after news provide clearer, lower-risk entry points. Letting price validate the news helps traders avoid false signals.

Timeframe Alignment and Patience

Many traders lose money by trading news on timeframes that do not match the event’s significance. Short-term scalping during major news releases is extremely risky due to slippage and whipsaws. Noise-free news traders often prefer higher timeframes—15-minute, 1-hour, or even daily charts—where the true impact of news becomes clearer.

Patience is critical. Not every news event needs to be traded immediately. Sometimes the best opportunity emerges hours or days later, once the market digests the information and establishes a clear trend.

Risk Management Over Prediction

A core principle of news trading without noise is accepting uncertainty. News outcomes are unpredictable, and even correct analysis can result in losses due to unexpected market reactions. Therefore, risk management is more important than prediction.

Traders should use predefined stop-loss levels, conservative position sizing, and avoid overexposure during high-volatility periods. Protecting capital ensures longevity and reduces emotional pressure, making it easier to stay disciplined and ignore noise.

Avoiding Media and Social Media Traps

Financial media and social platforms often amplify noise. Sensational headlines, conflicting expert opinions, and real-time commentary can distort perception and push traders into impulsive decisions. Noise-free traders limit exposure to such inputs, relying instead on primary data sources, official releases, and their own analysis frameworks.

Developing a personal trading plan and sticking to it is the best defense against external influence. When traders know exactly what they are looking for, irrelevant information naturally fades into the background.

Building a Structured News Trading Framework

To trade news without noise, traders should create a structured framework that includes:

A predefined list of tradable news events

Clear rules for pre-news preparation and post-news execution

Specific technical levels for confirmation

Strict risk management guidelines

This structure transforms news trading from reactive gambling into a professional, repeatable process.

Conclusion

News trading without noise is not about being the fastest or reacting to every headline. It is about clarity, selectivity, and discipline. By focusing on high-impact information, understanding expectations, waiting for price confirmation, and managing risk carefully, traders can turn news from a source of confusion into a powerful trading edge. In an age of information overload, the ability to filter noise is not just an advantage—it is a necessity for consistent success in financial markets.

EURUSD: Wave Structure Education - Understanding Wave CountsEducational breakdown of wave structure counting using current EURUSD as a live example.

📚 WAVE STRUCTURE FUNDAMENTALS

Understanding wave counts is essential for identifying high-probability setups. Let's break down the key concepts using EURUSD's current structure.

🌊 WAVE 1 - The Foundation

Most Important Aspect: Wave 1 has two variations

Variation 1 - ABC Pattern:

Wave 1 forms as a corrective ABC structure before the main trend establishes.

Variation 2 - Straight Away:

Bearish: Higher High (HH) directly to Lower Low (LL)

Bullish: Lower Low (LL) directly to Higher High (HH)

Why This Matters:

Identifying which Wave 1 variation you're seeing helps you understand the strength and nature of the trend forming.

📈 EXTENSION WAVES - The Power Moves

Bearish Extension Pattern:

The sequence for bearish extensions:

Lower High (LH)

Higher Low (HL)

Lower High (LH)

Lower Low (LL)

Bullish Extension Pattern:

The sequence for bullish extensions:

Higher Low (HL)

Lower High (LH)

Higher Low (HL)

Higher High (HH)

Key Principle:

Extensions follow a specific pattern. Recognizing these sequences allows you to anticipate the completion point and trade accordingly.

💼 CURRENT EURUSD WAVE COUNT

Position: Bearish Wave 2 Extension (3 of 5)

What This Means:

We're in Wave 2 of the larger structure

Wave 2 is extending (showing the extension pattern)

Currently at position 3 within the 5-wave extension sequence

More downside expected to complete the extension

Trading Application:

Understanding we're in position 3 of 5 tells us:

Two more wave points to complete (4 and 5)

Wave 4 will be a pullback (selling opportunity)

Wave 5 will be the final leg down in this extension

🎓 Educational Takeaways:

1. Wave 1 Sets The Stage:

Always identify which Wave 1 variation you're seeing. ABC or Straight Away? This determines your initial bias.

2. Extensions Follow Patterns:

Both bullish and bearish extensions have specific sequences. Learn to recognize them.

3. Count = Roadmap:

When you know where you are in the wave count (like "3 of 5"), you know what's coming next.

4. Practice Required:

Wave counting takes time to master. Watch price action create these patterns repeatedly until recognition becomes second nature.

Summary:

Wave 1 has two variations: ABC or Straight Away (HH→LL / LL→HH)

Extensions follow patterns: Specific sequences for bullish/bearish

Current EURUSD: Bearish Wave 2 Extension, position 3 of 5

Next: Expect Wave 4 pullback, then Wave 5 completion

👍 Boost if you found this educational

👤 Follow for more wave structure lessons

💬 Questions? Drop them in comments

Why the Market Loves to Trap Traders!!!If trading ever feels personal, it’s not.

The market isn’t hunting you; it’s hunting liquidity.

Understanding this single idea changes how you read charts forever.

1️⃣ The Market Moves Toward Liquidity, Not Logic

Most traders expect price to move because a pattern is “complete” or a level is “perfect.”

In reality, price moves to where orders are sitting.

Where is liquidity usually found?

- Above obvious highs

- Below obvious lows

- Around round numbers

- Near breakout levels everyone is watching

The market goes where the orders are, not where traders hope it goes.

2️⃣ Breakouts Are the Most Common Liquidity Pools

When price approaches a clear resistance, traders place:

- breakout buys above

- stop-losses from shorts just above

That creates a liquidity magnet.

Price spikes above the level, fills those orders…

and often reverses sharply once liquidity is consumed.

That’s not manipulation... that’s mechanics.

3️⃣ Traps Reveal Who’s Really in Control

A trap happens when price:

- breaks a key level

- fails to follow through

- returns back inside the range

This tells you something critical:

➡️ The side that should have won… didn’t.

4️⃣ Professionals Don’t Chase; They Wait

Retail traders react to the breakout.

Professionals wait for the reaction after the breakout.

They ask:

- Did price accept above the level?

- Did momentum expand or fade?

- Did structure shift or snap back?

Patience turns traps into opportunities.

📚The Core Lesson

The market’s job is not to reward anticipation. It’s to test conviction.

Once you stop trading where everyone else enters and start observing who gets trapped,

price action becomes clearer, calmer, and more logical.

⚠️ Disclaimer: This is not financial advice. Always do your own research and manage risk properly.

📚 Stick to your trading plan regarding entries, risk, and management.

Good luck! 🍀

All Strategies Are Good; If Managed Properly!

~Richard Nasr

ESG and Carbon Credit TradingThe New Architecture of Sustainable Finance

In the modern global economy, sustainability has shifted from being a moral consideration to a strategic and financial imperative. At the center of this transformation lie ESG (Environmental, Social, and Governance) principles and carbon credit trading, two closely linked frameworks that are reshaping how businesses, investors, and governments measure value, manage risk, and pursue long-term growth. Together, they form the backbone of sustainable finance and climate-aligned markets.

Understanding ESG: Beyond Profits

ESG refers to a set of non-financial criteria used to evaluate a company’s operations and long-term resilience.

Environmental (E): How a company manages its impact on nature—carbon emissions, energy usage, waste management, water conservation, and biodiversity.

Social (S): How it treats employees, customers, and communities—labor practices, human rights, diversity, workplace safety, and customer responsibility.

Governance (G): How it is managed—board structure, executive compensation, transparency, shareholder rights, and ethical conduct.

Unlike traditional financial metrics that focus mainly on short-term profitability, ESG frameworks aim to capture long-term sustainability and risk-adjusted performance. Investors increasingly believe that companies with strong ESG practices are better positioned to handle regulatory changes, reputational risks, climate shocks, and social disruptions.

Why ESG Matters in Capital Markets

ESG has become a decisive factor in global capital allocation. Institutional investors, sovereign wealth funds, pension funds, and asset managers now integrate ESG scores into portfolio decisions. This shift is driven by three powerful forces:

Risk Management: Climate change, social unrest, and governance failures can destroy shareholder value. ESG analysis helps identify hidden risks.

Regulatory Pressure: Governments worldwide are mandating ESG disclosures, forcing companies to report sustainability metrics alongside financial results.

Investor Preference: A growing base of investors prefers companies aligned with ethical, environmental, and social responsibility.

As a result, ESG is no longer a “nice-to-have” feature—it directly affects stock valuations, borrowing costs, and access to global capital.

Carbon Credit Trading: Putting a Price on Pollution

Carbon credit trading is a market-based mechanism designed to reduce greenhouse gas emissions by assigning a monetary value to carbon dioxide and other greenhouse gases.

A carbon credit typically represents the right to emit one metric ton of CO₂ (or equivalent gases). Companies that emit less than their allowed quota can sell surplus credits, while high emitters must buy credits to offset excess emissions.

There are two major carbon markets:

Compliance Markets: Mandated by governments (e.g., cap-and-trade systems). Companies must comply with legally binding emission limits.

Voluntary Carbon Markets (VCMs): Companies voluntarily purchase credits to meet sustainability goals, net-zero pledges, or ESG commitments.

By attaching a financial cost to emissions, carbon trading incentivizes businesses to innovate, adopt cleaner technologies, and improve energy efficiency.

The Link Between ESG and Carbon Credit Trading

Carbon credit trading is a practical tool that directly supports the Environmental pillar of ESG. Companies with strong ESG strategies often use carbon credits to:

Offset unavoidable emissions

Achieve carbon neutrality or net-zero targets

Demonstrate measurable climate action to investors

Improve ESG ratings and sustainability scores

In essence, carbon markets convert climate responsibility into a tradable financial instrument, aligning environmental goals with market incentives.

Carbon Credits as a Financial Asset

Over time, carbon credits have evolved from regulatory instruments into tradable assets. They are now bought and sold by:

Corporations managing emissions

Financial institutions and hedge funds

ESG-focused investment funds

Commodity traders and exchanges

This financialization has increased liquidity, price discovery, and global participation, while also introducing volatility and speculation. Carbon prices now respond to policy changes, economic growth, energy transitions, and geopolitical developments—much like traditional commodities.

ESG Ratings and Corporate Strategy

Companies are increasingly embedding ESG into their core strategies rather than treating it as a compliance exercise. Carbon credit trading plays a critical role in this shift:

Operational Strategy: Firms invest in renewable energy, efficiency upgrades, and carbon offsets to reduce exposure to carbon costs.

Reputation Management: Transparent use of high-quality carbon credits enhances credibility with stakeholders.

Capital Access: Strong ESG performance lowers financing costs and attracts long-term investors.

However, the effectiveness of ESG depends on authentic action, not cosmetic compliance.

Challenges and Criticism

Despite their promise, ESG and carbon credit markets face several challenges:

Greenwashing: Some companies exaggerate ESG claims or rely excessively on low-quality carbon offsets.

Lack of Standardization: ESG ratings vary widely across agencies, creating confusion and inconsistency.

Carbon Credit Quality: Not all credits deliver real, additional, and permanent emission reductions.

Market Transparency: Voluntary carbon markets still lack unified oversight and pricing benchmarks.

These issues have sparked calls for stricter regulation, better disclosure standards, and improved verification mechanisms.

The Role of Technology

Technology is accelerating trust and efficiency in ESG and carbon markets:

Blockchain: Ensures traceability and prevents double-counting of carbon credits.

AI and Data Analytics: Improve ESG scoring, emissions tracking, and risk assessment.

Satellite Monitoring: Verifies forest conservation, renewable energy output, and land-use projects.

These innovations are helping transform ESG and carbon trading into more reliable and scalable systems.

Future Outlook: ESG and Carbon Trading as Economic Pillars

Looking ahead, ESG and carbon credit trading are expected to become central pillars of the global financial system. As climate risks intensify and governments tighten emissions regulations, carbon prices are likely to rise, making sustainability a competitive advantage rather than a cost burden.

Key future trends include:

Integration of carbon pricing into mainstream financial models

Expansion of regulated carbon markets across emerging economies

Greater convergence of ESG reporting standards

Increased investor scrutiny of carbon offset quality

Conclusion

ESG and carbon credit trading represent a fundamental shift in how markets define value, risk, and responsibility. By embedding environmental and social costs into financial decision-making, they bridge the gap between economic growth and planetary limits. While challenges remain, their evolution signals a future where sustainability and profitability are no longer opposing goals—but interconnected drivers of long-term success.

In this new financial architecture, companies that adapt early and authentically will not only comply with regulations but also gain strategic, reputational, and financial advantages in a rapidly changing world.

Why Risk–Reward Matters More Than Win Rate!!One of the biggest myths in trading is this:

“I need to win more trades to be profitable.”

✖️You don’t...

Some of the most profitable traders in the world win less than 50% of their trades.

So what’s the real edge?

👉 Risk–reward.

1️⃣ Win Rate Without Risk–Reward Is Meaningless

A trader who wins 70% of the time but risks 3 to make 1 is still bleeding slowly.

Meanwhile, a trader who wins only 40% of the time

but risks 1 to make 3 can grow consistently.🪜

Win rate tells you how often you’re right.

Risk–reward tells you how much it matters when you are.

2️⃣ Risk Defines the Trade Before Entry

Professionals don’t start with targets.

They start with invalidation.

They ask:

- Where is my idea wrong?

- Where does structure break?

- Where must I be out?

Only after risk is defined, do rewards become meaningful.🏆

If you don’t know where you’re wrong,

you don’t know what you’re trading.

3️⃣ Good Risk–Reward Creates Emotional Stability

When your risk is small and predefined:

- losses feel normal

- hesitation disappears

- overtrading drops

Why?

Because no single trade can hurt you badly❗️

Risk–reward doesn’t just protect your account.

It protects your mindset.

4️⃣ Risk–Reward Is What Builds Consistency

Consistency doesn’t come from winning streaks.

It comes from surviving losing streaks.📉

Proper risk–reward ensures:

- drawdowns stay shallow

- confidence stays intact

- discipline stays repeatable

That’s how traders last long enough to let probabilities work.

📚The Big Lesson

✔️You don’t need to be right more often.

✖️You need your winners to matter more than your losers.

When risk is controlled and reward is logical, trading stops feeling like gambling and starts feeling like execution.

⚠️ Disclaimer: This is not financial advice. Always do your own research and manage risk properly.

📚 Stick to your trading plan regarding entries, risk, and management.

Good luck! 🍀

All Strategies Are Good; If Managed Properly!

~Richard Nasr

Pharmaceutical Stocks: Growth, Stability, and OpportunitiesThe Healthcare Market

Pharmaceutical stocks represent companies engaged in the research, development, manufacturing, and marketing of medicines and healthcare products. These stocks play a crucial role in global equity markets because healthcare is a basic necessity, largely independent of economic cycles. As populations grow, age, and face new health challenges, the demand for medicines continues to rise, making the pharmaceutical sector one of the most resilient and strategically important industries worldwide.

Nature and Importance of the Pharmaceutical Sector

The pharmaceutical industry is built on innovation and scientific research. Companies invest heavily in research and development (R&D) to discover new drugs, improve existing treatments, and address unmet medical needs. This long-term focus makes pharma stocks unique compared to other sectors. While technology companies innovate in software or electronics, pharma firms innovate in human health, often requiring years of clinical trials, regulatory approvals, and large capital investments.

Pharma stocks are important not only for investors but also for society. Breakthrough drugs for cancer, diabetes, cardiovascular diseases, and infectious illnesses can significantly improve quality of life and extend life expectancy. Governments and healthcare systems depend on pharmaceutical companies to maintain public health, which ensures consistent demand for their products.

Types of Pharmaceutical Companies

Pharmaceutical stocks can broadly be divided into different categories. Large-cap pharmaceutical companies, often called “big pharma,” have diversified product portfolios, global distribution networks, and strong balance sheets. These companies usually provide stable revenues, regular dividends, and lower risk compared to smaller firms.

Mid-cap and small-cap pharma companies often focus on niche therapies, generic drugs, or contract manufacturing. While they carry higher risk, they can deliver higher growth if they succeed in expanding markets or securing regulatory approvals. Biotechnology companies, which are closely linked to pharma stocks, focus on cutting-edge research such as gene therapy, vaccines, and biologics. These stocks can be highly volatile but offer substantial upside potential.

Drivers of Growth in Pharma Stocks

Several factors drive the growth of pharmaceutical stocks. One of the most important is demographic change. Aging populations, especially in developed countries, increase demand for chronic disease treatments such as diabetes, arthritis, and heart-related conditions. At the same time, rising healthcare awareness and improving access to medicines in emerging markets support long-term growth.

Innovation is another key driver. Companies that successfully develop patented drugs enjoy pricing power and exclusivity for several years, leading to high profit margins. Vaccines, specialty drugs, and biologics have become major growth areas, particularly after global health crises highlighted the importance of rapid drug development.

Government healthcare spending and insurance coverage also influence pharma stocks. Increased public and private investment in healthcare infrastructure supports pharmaceutical sales. In many countries, policies encouraging generic drug use create opportunities for companies specializing in cost-effective medicines.

Risks Associated with Pharma Stocks

Despite their defensive nature, pharmaceutical stocks carry specific risks. One of the biggest challenges is regulatory uncertainty. Drug approvals depend on strict regulatory authorities, and delays or rejections can significantly impact a company’s share price. Even after approval, drugs may face post-marketing safety issues that lead to recalls or legal action.

Patent expiration is another major risk. When a blockbuster drug loses patent protection, generic competitors enter the market, sharply reducing revenues. This “patent cliff” can negatively affect earnings if companies fail to replace lost sales with new products.

Pricing pressure is also a growing concern. Governments and insurers often push for lower drug prices to control healthcare costs. This can reduce profit margins, particularly in developed markets. Currency fluctuations, especially for companies with global operations, can further affect financial performance.

Pharma Stocks as Defensive Investments

Pharmaceutical stocks are often considered defensive because demand for medicines remains relatively stable during economic downturns. Unlike sectors such as real estate or luxury goods, healthcare spending cannot be easily postponed. As a result, pharma stocks tend to show lower volatility during market corrections and provide portfolio stability.

Many large pharmaceutical companies pay consistent dividends, making them attractive to long-term and income-focused investors. Their strong cash flows allow them to reinvest in R&D while also rewarding shareholders. During periods of high inflation or market uncertainty, pharma stocks are often viewed as a safe haven.

Role of Emerging Markets and India

Emerging markets play an increasingly important role in the pharmaceutical industry. Countries like India and China have become major hubs for generic drug manufacturing and contract research. Indian pharmaceutical companies, in particular, are known for producing affordable medicines and supplying a large share of global generic drugs.

For investors, pharma stocks in emerging markets offer a balance of growth and cost efficiency. Expanding healthcare access, government support, and export opportunities contribute to long-term potential. However, these stocks may also face regulatory scrutiny from international markets, especially related to quality standards.

Investment Approach to Pharma Stocks

Investing in pharmaceutical stocks requires a long-term perspective. Fundamental analysis is crucial, focusing on a company’s product pipeline, R&D capabilities, regulatory track record, and financial strength. Diversification within the sector helps reduce risk, as not all drugs or companies succeed at the same time.

Some investors prefer large-cap pharma stocks for stability, while others allocate a smaller portion of their portfolio to high-growth biotech or specialty pharma companies. Monitoring clinical trial results, patent timelines, and policy changes is essential for informed decision-making.

Conclusion

Pharmaceutical stocks occupy a unique and powerful position in the global equity market. They combine elements of stability, innovation, and long-term growth driven by healthcare needs. While the sector faces challenges such as regulatory risks, patent expirations, and pricing pressures, its fundamental importance to society ensures sustained demand.

For investors, pharma stocks can serve as a defensive core holding while also offering opportunities for capital appreciation through innovation and emerging market growth. With careful analysis and a balanced approach, pharmaceutical stocks can play a vital role in building a resilient and diversified investment portfolio.

Why the Reaction Matters More Than the Level!!!Most traders spend their time hunting for the perfect level.✖️

Support. Resistance. Demand. Supply.

They draw the zone… and assume price must react.

But professionals know something crucial:

The level itself is not the edge.

The reaction is.

Here’s why.

1️⃣ Levels Are Common Knowledge

Everyone sees the same support.

Everyone sees the same resistance.

If levels alone were enough, everyone would be profitable.

A level is just a location.📍

It doesn’t tell you who is in control.

2️⃣The Reaction Reveals Intent

What matters is how price behaves at the level.

Ask yourself:

- Does price reject immediately or hesitate?

- Are candles impulsive or overlapping?

- Does price leave the level with strength or drift away slowly?

A strong reaction tells you:

➡️ One side stepped in aggressively.

A weak reaction tells you:

➡️ The level exists… but conviction doesn’t.

3️⃣ Clean Rejections Beat Perfect Levels

A slightly imperfect level with a violent reaction

is far more valuable than a textbook level with no follow-through.

Professionals wait for:

- sharp rejections

- momentum expansion

- structure confirmation

They don’t assume... they observe.

4️⃣ Failed Reactions Are Warnings

When price reaches a level and does nothing…

that silence is information.

Failed reactions often lead to:

- level breaks

- deeper moves

- trend continuation

The market is telling you:

➡️ “This level no longer matters.”

📚The Big Lesson

Levels tell you where to look.

Reactions tell you what to do.

If you shift your focus from drawing levels to reading behavior at levels,

your trading instantly becomes clearer and more objective.

⚠️ Disclaimer: This is not financial advice. Always do your own research and manage risk properly.

📚 Stick to your trading plan regarding entries, risk, and management.

Good luck! 🍀

All Strategies Are Good; If Managed Properly!

~Richard Nasr

Risk Psychology and Performance in Global Markets1. Defining Risk Psychology

Risk psychology, sometimes referred to as behavioral finance, examines how emotions, cognitive biases, and mental frameworks shape perceptions of risk and influence decision-making. Traditional economic theory assumes that market participants are rational actors who always make decisions based on complete information and logical analysis. However, decades of research, particularly by psychologists like Daniel Kahneman and Amos Tversky, have shown that human behavior often deviates from rationality. Traders may overreact to news, underestimate the probability of rare events, or follow herd behavior—actions that directly impact performance in global markets.

Risk psychology can be divided into several key dimensions:

Risk Perception: How individuals interpret and assess potential losses and gains.

Risk Tolerance: The degree to which an individual or organization is willing to accept uncertainty or potential financial loss.

Cognitive Biases: Systematic errors in thinking, such as overconfidence, anchoring, or confirmation bias.

Emotional Responses: Reactions such as fear, greed, panic, or euphoria that can override logical decision-making.

2. Cognitive Biases and Market Behavior

One of the central insights from risk psychology is that cognitive biases can significantly distort market performance. Some of the most influential biases include:

Overconfidence: Traders often overestimate their knowledge or forecasting ability, leading to excessive risk-taking or frequent trading. In global markets, overconfident investors may underestimate geopolitical risks or macroeconomic uncertainties, which can result in large losses.

Loss Aversion: This is the tendency to weigh potential losses more heavily than equivalent gains. In volatile markets, loss-averse behavior can lead investors to exit positions prematurely, missing potential recoveries.

Herding: Many investors follow the actions of the majority rather than independent analysis, leading to bubbles and crashes. The 2008 global financial crisis and other market corrections illustrate how herding behavior amplifies systemic risk.

Anchoring: Market participants often rely too heavily on a reference point, such as a stock's past high, when making decisions. This can lead to mispricing in fast-moving global markets.

These biases illustrate that market performance is as much about managing internal psychological factors as it is about external economic conditions. Recognizing and mitigating these biases is essential for achieving consistent performance.

3. Emotional Drivers in Global Markets

Emotions are another powerful factor affecting performance. Fear and greed are two dominant emotions influencing trading decisions:

Fear: Sudden market downturns, geopolitical events, or economic crises can trigger fear, leading to panic selling. Fear-driven actions often exacerbate volatility and can result in substantial losses.

Greed: Conversely, the desire for high returns can push investors into over-leveraged positions or speculative assets. Excessive greed may lead to ignoring warning signals, contributing to financial bubbles.

In global markets, these emotions are amplified by the 24/7 nature of trading, high-speed information flow, and exposure to international geopolitical and macroeconomic events. Investors must develop emotional discipline to withstand market volatility and maintain long-term performance.

4. Risk Tolerance and Portfolio Management

Risk psychology directly informs risk tolerance, which is crucial for portfolio construction and investment strategy. Understanding one’s own risk profile—or that of an organization—is essential for aligning investment choices with financial goals and market conditions.

Conservative Investors: Prefer stable, low-risk assets even if returns are modest. They may underperform in bullish markets but avoid significant drawdowns during crises.

Aggressive Investors: Willing to take on higher risk for the potential of greater returns. Their performance can be stellar in favorable conditions but highly volatile during downturns.

Institutional Risk Management: Large global institutions often implement structured risk management frameworks that combine quantitative models with psychological insights to mitigate irrational decision-making among traders.

Balancing risk tolerance with market opportunities is a core component of consistent performance. Investors who fail to match their strategies with their psychological profile often make impulsive decisions that negatively affect returns.

5. The Impact of Risk Psychology on Market Trends

Risk psychology doesn’t just affect individual investors—it can influence global market trends. Collective human behavior, shaped by shared perceptions of risk and sentiment, can drive market cycles:

Bull Markets: Optimism and reduced risk perception fuel buying, often inflating asset prices beyond fundamental values.

Bear Markets: Pessimism and heightened fear lead to selling, creating sharp declines.

Volatility Spikes: Emotional reactions to unexpected events, such as geopolitical crises or central bank announcements, can result in abrupt market swings.

Market sentiment indicators, like the Volatility Index (VIX), are essentially measures of collective risk psychology. Traders and institutions often use these tools to gauge sentiment and anticipate potential market movements.

6. Strategies to Mitigate Psychological Risk

Given the profound influence of risk psychology on performance, it is crucial for market participants to implement strategies to manage these effects:

Education and Awareness: Understanding common biases and emotional triggers helps investors make more rational decisions.

Structured Decision-Making: Using checklists, rules-based systems, and quantitative models reduces the influence of emotion on trading decisions.

Diversification: Spreading investments across asset classes, geographies, and strategies mitigates the impact of unexpected events and reduces stress.

Regular Reflection and Journaling: Tracking decisions, outcomes, and emotional states helps identify patterns and improve future performance.

Stress Testing: Simulating adverse scenarios allows traders and institutions to anticipate emotional responses and refine risk management.

7. Conclusion

Performance in global markets is a complex interplay of economic fundamentals, technical analysis, and, importantly, human psychology. Risk psychology illuminates the ways in which emotions, cognitive biases, and perception of uncertainty influence market behavior. Traders and investors who cultivate self-awareness, emotional discipline, and structured decision-making frameworks can navigate market volatility more effectively and improve long-term performance.

Global markets are inherently uncertain, and even the most sophisticated models cannot fully predict outcomes. By understanding risk psychology, market participants gain a powerful tool: insight into their own behavior and the collective behavior of others. This understanding not only enhances individual performance but also contributes to a more stable and resilient financial system.

In essence, mastering risk psychology is not about eliminating risk—it’s about managing human responses to risk, aligning decisions with long-term goals, and leveraging an understanding of human behavior to thrive in the complex world of global finance.

Leading Diagonals: Confusing Traders since 1880sSInce mid Nov 2025, traders have found it almost impossible to predict the pattern in Bitcoin, Coreweave, NBIS kind of charts and rightly so, because leadign diagonal has entered the room.

So what is a leading diagonal . In Elliot wave theory, a leading diagonal appears at the start of a new trend. In short,

- It looks like a wedge with overlapping waves

- Forms when a trend is trying to begin but lacks full conviction

- Indicates early positioning before broader participation

- Is usually followed by a strong, decisive move once belief catches up

Think of it as the market testing new direction, before committing to it.

How the market feels when a leading diagonal is forming:

Conflicted rather than confident. Price is moving in the direction of the new trend, but the underlying conviction isn’t fully there yet.

1. Early believers vs. skeptics

A new trend is trying to start, but most participants are still anchored to the prior trend. Early buyers (or sellers) step in, yet they’re repeatedly met with profit-taking and countertrend pressure.

2. Momentum exists, but it’s uneven

You’ll often see overlapping waves, shallow follow-through, and corrective pullbacks that feel premature. This reflects commitment without consensus.

3. Volatility stays elevated

Because conviction is low, price tends to swing more than it should in a healthy impulse. Stops get hunted, and false breaks are common.

4. Participation is selective

Smart money is probing. Retail is hesitant. Volume often fails to expand cleanly because positioning is still being tested rather than fully deployed.

5. Pressure quietly builds

Each push forward that doesn’t fully fail chips away at skepticism. By the time the diagonal completes, positioning is often lopsided, setting up the sharp move that usually follows.

In short ,

A leading diagonal feels like a market arguing with itself. Direction is emerging, but belief hasn’t caught up yet. That internal debate is exactly why the structure looks messy and why the resolution afterward tends to be decisive.

So how to identify a leading diagonal technically:

1. Wave count: Five waves (1–2–3–4–5), but waves overlap (Wave 4 overlaps Wave 1).

2. Shape : Price compresses into a wedge (contracting or expanding).

3. Momentum : Progress is directional but uneven, with shallow follow-through.

4. Trendline s: Upper and lower boundaries converge or diverge, not parallel like an impulse.

5. Confirmation : The move after the diagonal is typically sharp and fast, validating the pattern.

6. Usually, : Wave a or 1 is longest and wave c or (iii) cannot be shortest amount the up waves

In essence, if price is advancing, overlapping, and compressing early in a move,while still making progress, you’re likely looking at a leading diagonal.

What do indicators show when a leading diagonal is forming ?

RSI

-Often shows weaker momentum on Wave 3 than expected.

- May produce early divergence even though price is still advancing.

- Tends to stay capped (bullish case) instead of trending strongly.

MACD

- Momentum expands initially, then fails to accelerate.

- Histogram peaks early and flattens as price continues.

- Signal line crosses are frequent, reflecting overlap and indecision.

How to trade a leading diagonal ?

- Leading diagonals overlap and retrace deeply. If you size or manage it like a clean Wave 1, you’ll get chopped.

- The safest entry is from Wave 4 → Wave 5, Stops usually go beyond the Wave b or wedge invalidation level.

- Best approach WAIT: The highest-quality trade often comes after the diagonal finishes.

- What to wait for: Clean break of the wedge, Momentum expansion (RSI/MACD confirmation), Strong follow-through in the next impulse

- Breakouts inside the diagonal frequently fail so avoid chasing internal breakouts. If price breaks a boundary but momentum and volume don’t expand, assume it’s noise.

A leading diagonal is the market warming up. The real opportunity comes once it’s done arguing.

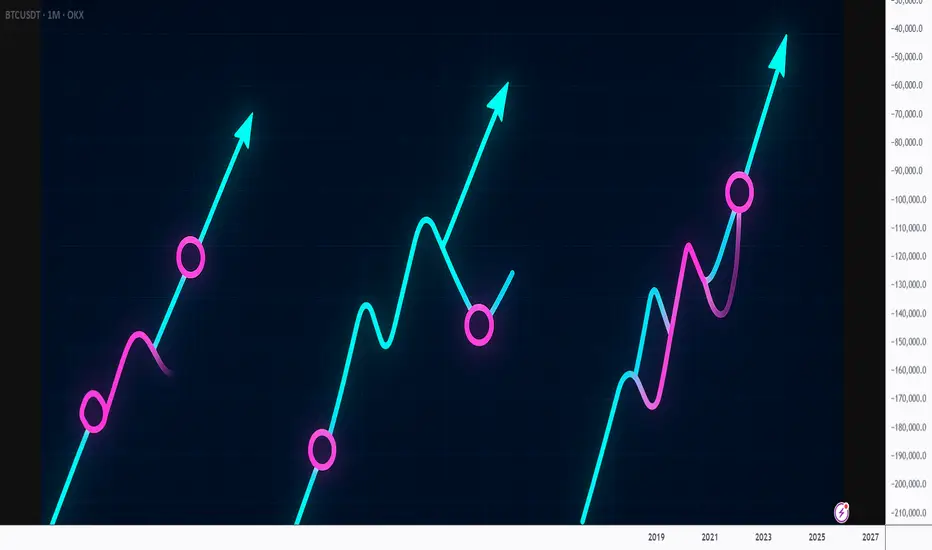

BITCOIN'S ALL TIME HISTORY CHART(KEY INSIGHTS)This is a breakdown of all major waves that have occurred in Bitcoin's History. This chart might explain why CRYPTOCAP:BTC has been the most successful coin while also answering if the growth will be sustained. This is a pretty standard 5 wave move- Waves 1 to 4 having been completed(shown in Red). We are on our last Major wave before it becomes a complete 5 wave impulse.

Wave 1(Red) was followed by a Zigzag correction for Wave 2, hence we expected a Flat correction For Wave 4. Keep in mind, this Flat correction had been predicted almost 2 and a half years before, when Wave 2 was completed! Wave 4 had 3 internal waves namely A,B and C- shown in Blue.

With Wave 4 complete, it was time to launch our 5th Wave of the Major impulse. This 5th Wave has 5 internal waves as is typical for impulses and are shown in Green. Once again, when Wave 1(Green) completes we see a Flat correction for Wave 2 meaning our Wave 4 would most likely be a Zigzag correction. Note that these two corrections are best seen on the Weekly and Daily Charts.

With Wave 4(Green) complete, what we are left with is Wave 5(Green) in its final developments. Once this Wave 5 is complete, this will be the Wave 5(Red) of Bitcoin. When this happens, it will be the end of the first impulse that started in 0ct. 2009 and the beginning of Wave 2, which will be a massive correction!

Volume Do Not Predict Price! - It Explains It!Most traders look at volume the wrong way.✖️

They expect volume to tell them where price will go next.

But volume’s real job is much more important:

Volume explains why price moved the way it did.

If you learn to read volume correctly, price action becomes clearer, not noisier.

1️⃣ Price Up + Rising Volume = Commitment

When price moves higher and volume expands, it means buyers are committed, not just reacting.

This is not random buying.

This is participation.

📈Rising volume during an impulse confirms that the move is supported by real interest, not just thin liquidity.

Strong trends are built on expanding volume.

2️⃣ Price Up + Falling Volume = Warning

When price continues higher but volume dries up, something changes.

The move still exists... but conviction doesn’t.

This often signals:

- exhaustion

- a potential pause

- or an upcoming correction

That’s when professionals stop chasing and start managing risk.

3️⃣ Sideways Price + Rising Volume = Accumulation or Distribution

This is where most traders get confused:

Price isn’t moving much, but volume is increasing.

That’s not boredom.

That’s positioning.

Large players don’t chase price.

They build positions quietly while price looks “dead.”

Breakouts that follow these zones tend to be fast and decisive, because the work was already done.❗️

4️⃣ Breakouts Without Volume Are Suspect

A breakout candle looks exciting.

But without volume, it’s just a move, not a decision.

Low-volume breakouts often lead to:

- fakeouts

- traps

- fast reversals

🏹Volume doesn’t need to explode... but it needs to confirm participation.

💡The Big Picture

Volume is not a signal by itself. It’s context.

Price tells you what happened, while Volume tells you how serious that move really was.

✔️When price and volume agree, trades feel easy.

✖️When they disagree, something important is hiding underneath.

⚠️ Disclaimer: This is not financial advice. Always do your own research and manage risk properly.

📚 Stick to your trading plan regarding entries, risk, and management.

Good luck! 🍀

All Strategies Are Good; If Managed Properly!

~Richard Nasr

Global Trade Costs, Inflation, and Interest Rates1. Global Trade Costs: What They Are and Why They Matter

Global trade costs refer to all expenses involved in moving goods or services from one country to another. These costs end up affecting product prices, competitiveness, and economic growth.

A. Components of Trade Costs

Transportation Costs

Shipping, aviation, trucking, rail freight

Fuel prices

Port handling and container charges

Insurance on cargo

When fuel prices rise or there is a shortage of containers (like after COVID-19), transportation costs shoot up sharply.

Tariffs

Governments impose taxes on imported goods. Tariffs can protect domestic industries but increase prices for consumers.

Non-Tariff Barriers (NTBs)

These include:

Quality standards

Product certifications

Customs procedures

Import quotas

Environmental and safety regulations

NTBs often add delays and compliance costs.

Exchange Rate Fluctuations

If a country’s currency weakens, its imports become more expensive; if it strengthens, imports become cheaper.

Political and Geopolitical Risks

War, sanctions, tensions between countries

Trade agreements collapsing

Piracy risks on shipping routes

These uncertainties raise risk premiums and insurance costs.

Logistical Efficiency

Countries with strong ports, roads, and customs technology have far lower trade costs.

B. Impact of High Trade Costs

Higher export and import prices

Reduced competitiveness in global markets

Lower consumer choices

Slowdown in global supply chains

Inflationary pressure, especially in import-dependent countries

Thus, trade cost is not just an economic number—it is a powerful driver behind global price movements.

2. Inflation: The Price Level That Affects Everyone

Inflation is the rate at which the general price level of goods and services rises over time. When inflation increases, money loses value, and purchasing power declines.

A. Major Causes of Inflation

Demand-Pull Inflation

When demand is higher than supply (e.g., festival season, economic boom), prices rise.

Cost-Push Inflation

When the cost of production increases—due to higher raw material prices, trade costs, or wages—producers raise prices.

Imported Inflation

Many countries depend on imports for food, energy, metals, or electronics.

If global trade costs increase or the currency weakens, import prices rise and inflation increases.

Supply Chain Disruptions

Events such as pandemics, geopolitical conflicts, and natural disasters break supply chains and reduce availability, leading to higher prices.

Monetary Factors

When central banks print too much money or keep interest rates too low, prices tend to rise.

B. Effects of Inflation

Reduced purchasing power

Higher cost of living

Lower savings value

Increased business uncertainty

Wage-price spiral

Pressure on governments and central banks to intervene

Moderate inflation is normal, but high inflation or hyperinflation can destabilize entire economies.

3. Interest Rates: The Financial Lever Controlling Inflation

Interest rates are the cost of borrowing money. Central banks (like the Federal Reserve, ECB, RBI, etc.) adjust interest rates to stabilize economic growth and inflation.

A. How Interest Rates Work

When interest rates rise:

Loans become expensive

Businesses reduce investments

Consumers cut spending

Savings become attractive

Economy slows

Inflation typically falls

When interest rates fall:

Borrowing becomes cheaper

Investment and consumption rise

Economy grows

If demand grows too fast, inflation increases

Interest rates are the primary tool used by central banks to fight inflation.

4. How Global Trade Costs, Inflation, and Interest Rates Interact

These three forces are deeply interconnected, and one change triggers reactions in the others.

A. High Trade Costs → Higher Inflation

When trade costs rise due to fuel surges, war disruptions, or container shortages:

Transportation becomes expensive

Imports cost more

Raw materials become pricier

Companies pass these costs to consumers

This leads to cost-push inflation, especially in developing countries dependent on imported commodities.

Examples:

Oil price increases raise transportation costs globally.

War in major shipping routes slow down container movement and raise freight rates.

B. Inflation → Higher Interest Rates

When inflation rises above a country’s target (usually 2–6%), central banks increase interest rates to cool the economy.

This is called monetary tightening.

Why?

Higher interest rates reduce demand in the economy and slow down price growth.

C. Higher Interest Rates → Higher Trade Costs

When interest rates rise globally:

The cost of financing ships, warehouses, and inventory increases

Multinational companies borrow less

Currency values fluctuate

Emerging markets face capital outflows

Trade slows, increasing per-unit shipping costs

Thus, interest rate hikes indirectly increase global trade costs.

D. Higher Interest Rates → Stronger Domestic Currency

This reduces imported inflation because foreign goods become cheaper.

But if a strong currency hurts export competitiveness, trade volumes may decline.

5. The Global Cycle: How One Factor Creates a Chain Reaction

A typical cycle looks like this:

Trade costs rise due to global disruptions.

This causes imported inflation.

Central banks respond by raising interest rates.

Higher interest rates:

slow down demand

reduce inflation

increase borrowing cost

Businesses cut production or trade volumes, which eventually lowers global trade costs again.

This balancing cycle is what keeps global markets stable over time.

6. Why These Factors Matter More Today

Global markets face many new challenges:

Fragmenting supply chains (“China+1” diversification)

Geopolitical tensions

Climate-related disruptions

Volatile energy prices

Uncertain global monetary policies

All these factors make the interaction between trade costs, inflation, and interest rates more unpredictable. Investors, traders, and policymakers must track them closely to anticipate market movements.

Conclusion

Global trade costs, inflation, and interest rates form a powerful economic triangle that influences every country, company, and consumer in the world. Trade costs shape prices, inflation determines purchasing power, and interest rates regulate economic stability. Their interaction drives global growth cycles, financial markets, and corporate strategies. Understanding this dynamic helps traders, economists, and students decode global market behavior in a clear, structured manner.

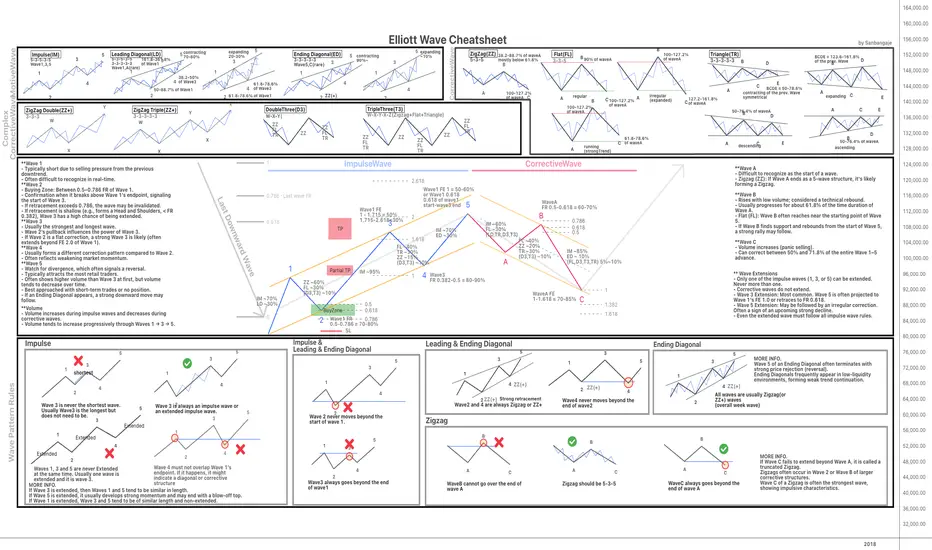

Elliott Wave Rules: Quick Cheatsheet for TradersHello everyone! I'm happy to share this Elliott Wave Cheat Sheet that I personally created during my journey. I hope this guide is helpful to the community.

This chart is designed to provide a quick, at-a-glance overview of the core Elliott Wave principles and patterns. Please note, it is just a summary of the main theories.

To dig into further and truly master the concepts, I highly recommend consulting the foundational texts:

* Elliott Wave Principle: Key to Market Behavior by A.J. Frost and Robert Prechter

* Mastering Elliott Wave by Glenn Neely

** Best viewed with QHD resolution (2560x1440)

** If the chart appears slightly squeezed vertically, you can adjust the aspect ratio by dragging the Price Panel (Y-axis) on the right side of the chart.**

**You can download the PNG version of this chart here:

drive.google.com

Happy Trading!

Swap Trading Secrets1. What Is a Swap?

A swap is a contract between two parties to exchange cash flows or financial obligations for a specified period. These exchanges typically involve interest rates, currencies, commodities, or credit risks.

Think of a swap like this:

You have one type of cash flow.

I have another.

We exchange them because each of us prefers the other’s structure.

This exchange helps both parties balance risk, stabilize cash flows, or lock in profits.

Swaps are custom-designed, traded over the counter (OTC), and not listed on exchanges.

2. Major Types of Swaps

To understand swap trading secrets, you first need to know the main types used globally:

1. Interest Rate Swaps (IRS)

Most common type.

Party A pays a fixed rate.

Party B pays a floating rate.

Useful for:

Hedging interest costs.

Managing debt efficiently.

2. Currency Swaps

Exchange principal + interest in different currencies.

Useful for:

Reducing currency risk.

Accessing foreign loans at cheaper rates.

3. Commodity Swaps

Fixed vs floating commodity prices.

Useful for:

Hedging input costs (oil, metals, agri).

Locking profit margins.

4. Credit Default Swaps (CDS)

Insurance against bond default.

Useful for:

Hedging credit risk.

Speculating on company survival.

5. Equity Swaps

Exchange equity returns for interest or another equity index.

Useful for:

Gaining exposure without owning the asset directly.

3. Why Swaps Are Considered a “Secret Weapon”

Swaps provide powerful advantages that many traders do not see:

A. Hidden Leverage

Institutions gain exposure to markets:

WITHOUT owning assets,

WITHOUT large upfront capital.

This makes swaps an efficient way to amplify returns.

B. Off-Balance-Sheet Benefits

Swaps can shift risks without moving assets on books, making financial statements look cleaner.

C. Customization

Unlike futures, swaps are tailor-made:

Amount

Duration

Payment structure

Asset type

Currency

This gives institutions almost unlimited flexibility.

D. Access to Better Pricing

Banks and hedge funds use swaps to:

Access lower foreign interest rates

Reduce borrowing costs

Hedge exposures cheaply

This pricing advantage is one of the biggest swap trading secrets.

E. Tax Optimization

Some institutions use swaps to:

Receive returns without triggering capital gains

Change income types for tax benefits

4. How Institutions Actually Use Swap Trading

Now let’s explore the real-world secrets of how swaps are used.

Secret 1: Hedging Interest Rate Risk Like a Pro

When interest rates rise or fall, companies with loans face huge cost changes.

So they use Interest Rate Swaps:

If expecting rates to rise → pay fixed, receive floating.

If expecting rates to fall → receive fixed, pay floating.

This stabilizes their cash flows.

Example:

A company with a floating-rate loan fears rising rates.

They enter a swap to pay 5% fixed and receive floating.

If floating rates shoot to 8%, the swap saves them millions.

Secret 2: Currency Swaps for Cheaper Global Loans

Corporations often borrow in foreign currencies.

But banks offer different interest rates in different countries.

So companies use currency swaps to borrow where rates are cheaper, then swap back to their local currency.

Example:

An Indian company might borrow yen at 1% instead of rupees at 7%, then swap obligations with a Japanese firm.

This cuts financing cost dramatically.

Secret 3: Equity Exposure Without Buying Shares

Hedge funds love equity swaps because they:

Get full market returns

Avoid ownership reporting

Avoid voting rights

Avoid taxes on buying/selling stocks

Can build secret positions

This is how some funds take huge equity bets without showing them publicly.

Secret 4: Commodity Swaps to Lock Prices Years Ahead

Airlines, manufacturers, and refiners use commodity swaps to stabilize costs.

Example:

An airline may fix jet fuel prices for three years through swaps, eliminating volatility.

This ensures consistent profit margins regardless of market swings.

Secret 5: Credit Default Swaps for Hidden Speculation

CDS contracts let traders “bet” on whether a company will default.

Professionals use CDS to:

Hedge corporate bond exposure

Take leveraged positions on credit quality

Profit from market panic or recovery

Some hedge funds made billions during the 2008 crisis via CDS trades.

5. Secret Trading Strategies Using Swaps

Let’s break down advanced strategies used in swap trading.

A. Swap Spread Trading

Traders exploit differences between:

Swap rates

Government bond yields

If swap spreads widen or narrow unexpectedly, traders enter opposite positions to profit from mean reversion.

B. Curve Steepening / Flattening Strategies

Traders use interest rate swaps to bet on the shape of the yield curve.

Steepener: receive fixed (long end), pay fixed (short end)

Flattener: opposite

These are used when expecting macroeconomic shifts.

C. Currency Basis Arbitrage

Banks exploit differences between:

Currency forward rates

Interest rate differentials

Swap rates

This arbitrage generates low-risk profits.

D. Synthetic Asset Exposure

Traders use swaps to create:

Synthetic bonds

Synthetic equity positions

Synthetic commodities

This avoids capital requirements and tax implications.

E. Hedged Carry Trades

Funds borrow in low-rate currencies and swap into higher-rate currencies while hedging currency risk.

This generates predictable “carry” income.

6. Key Risks in Swap Trading

Swaps are powerful, but they carry risks:

1. Counterparty Risk

If your swap partner defaults, you lose.

(This is what happened with Lehman Brothers.)

2. Liquidity Risk

Swaps cannot be easily sold like stocks.

3. Interest Rate / Market Risk

If the market moves against your swap position, you face large losses.

4. Valuation Complexity

Swaps require mark-to-market calculations.

5. Legal & Operational Risk

Documentation errors can cause disputes.

7. Why Retail Traders Rarely Use Swaps

Swaps require:

Large contracts

Institutional relationships

Legal agreements

Creditworthiness

Sophisticated pricing models

However, retail traders indirectly benefit through:

Mutual funds

ETFs

Banks

Derivative products

These institutions use swaps behind the scenes to improve performance.

Conclusion

Swap trading is one of the financial world’s most powerful, secretive, and flexible tools. Institutions use swaps to hedge risk, create leverage, optimize taxes, reduce financing costs, and structure sophisticated trading strategies across interest rates, currencies, commodities, and credit.

Even though retail traders rarely trade swaps directly, understanding them gives you insights into how the world’s largest financial players operate. If you understand swap dynamics, you gain a deeper understanding of global money flows, risk management, and institutional market behavior.

International Market Insights1. What Are International Markets?

International markets refer to financial markets operating across countries—where global investors trade stocks, currencies, bonds, commodities, and derivatives. These markets include:

a) Global Stock Markets

Major exchanges such as:

NYSE & Nasdaq (USA)

London Stock Exchange (UK)

Tokyo Stock Exchange (Japan)

Shanghai & Hong Kong Stock Exchange (China)

Euronext (Europe)

India's NSE & BSE (Emerging Markets)

International stock markets reflect global corporate earnings, economic health, and geopolitical stability.

b) Forex (Foreign Exchange Market)

The largest financial market globally, trading:

Major pairs (EUR/USD, USD/JPY)

Cross pairs (EUR/JPY)

Emerging market currencies (INR, BRL)

Forex movements show real-time global economic sentiment.

c) Commodity Markets

Global commodities such as:

Crude oil

Gold & silver

Natural gas

Base metals (Copper, Zinc)

Agricultural products (Soybean, Wheat)

d) Bond Markets

Sovereign and corporate bonds traded internationally reflect interest rates, inflation expectations, and risk appetite.

2. Why International Markets Matter

International markets provide insights into global:

Liquidity flow

Economic trends

Risk appetite

Corporate performance

Currency stability

Commodity cycles

For a trader or investor, global markets act like a “leading indicator.” For example:

If the U.S. markets fall sharply, Asian markets often open lower.

If crude oil prices rise, inflation risk increases globally.

If the USD strengthens, emerging markets often see capital outflows.

Understanding international markets allows better decision-making in:

Equity investing

Forex trading

Commodity trading

Options & derivatives

Business planning and imports/exports

3. Major Drivers of International Markets

A. Economic Indicators

Global markets move on key macroeconomic data such as:

GDP growth

Interest rates

Inflation (CPI, WPI)

Unemployment rate

Manufacturing PMI

Retail sales

Trade balance

For example:

Higher U.S. inflation → Higher chances of Federal Reserve rate hike → Strengthening USD → Weakening global equities.

B. Central Bank Policies

Central banks such as the Federal Reserve (Fed), European Central Bank (ECB), Bank of Japan (BOJ), and Reserve Bank of India (RBI) influence global liquidity.

Higher interest rates restrict liquidity → markets fall.

Lower interest rates create liquidity → markets rally.

C. Geopolitical Events

Events such as:

wars,

sanctions,

elections,

trade disputes,

diplomatic tensions,

immediately affect international markets.

Example:

Russia–Ukraine war → Crude oil and natural gas prices surged globally.

U.S.–China trade war → Impact on global supply chains and tech stocks.

D. Currency Movement

Currency fluctuations affect:

Import/export costs,

Foreign investment,

Commodity prices.

If USD rises:

Commodities like gold and crude become expensive.

Emerging market currencies weaken.

E. Corporate Earnings

Global companies like Apple, Tesla, Amazon, Samsung, and Toyota influence global investor sentiment.

Positive earnings → global market rally

Negative earnings → global correction

4. Key Global Market Trends to Track

1. US Market Trends

The U.S. market influences almost every other market. Key indices include:

Dow Jones

S&P 500

Nasdaq 100

Why important?

US technology and financial institutions dominate global markets.

The USD is the world’s reserve currency.

2. European Market Outlook

Important indices:

FTSE 100 (UK)

DAX (Germany)

CAC 40 (France)

Europe’s data impacts:

Auto sector

Banking

Energy markets

3. Asian Markets

Key markets:

Nikkei (Japan)

Hang Seng (Hong Kong)

Shanghai Composite (China)

Nifty & Sensex (India)

Asia is crucial for:

Manufacturing

Global supply chains

Technology components

Emerging market growth

4. Crude Oil Trends

Crude oil affects:

Inflation

Transportation

Trade deficit

Currency movement

Countries like India are heavily impacted by crude prices.

5. Gold Trends

Gold is a “safe-haven asset.” During fear or recession:

Gold prices rise

Stock markets fall

6. Bond Yields

US Bond yield (10-year) is a critical global indicator.

Rising yields → risk-off sentiment.

Falling yields → risk-on sentiment.

5. How International Markets Impact India

India is one of the world’s fastest-growing emerging markets. Global cues directly influence Indian equities, forex, and commodities.

a) US Market Impact

If the US markets fall:

FIIs withdraw from India

Nifty & Sensex fall

INR weakens

b) Dollar Index (DXY)

Rising DXY → pressure on emerging markets

Falling DXY → relief rally in equities and commodities

c) Crude Oil Movement

Higher crude = higher inflation = possible RBI rate hike

d) Global Risk Appetite

If global funds shift to safe assets such as bonds or gold, emerging markets see outflows.

6. Tools Used to Analyze International Markets

1. Economic Calendar

Tracks global economic events impacting market volatility.

2. Market Correlation Analysis

Example:

Nifty is highly correlated with S&P 500.

Gold is inversely correlated with USD.

3. Volume Profile & Market Structure

You can analyze:

Price action

Value areas

Global liquidity zones

(Useful for your interest in volume profile and structure-based trading.)

4. Global Indices Screeners

Tools to monitor:

Pre-market data

Futures

International indices

Currency heatmaps

Commodity charts

5. Central Bank Commentary

Federal Reserve statements often drive global markets for weeks.

7. Key Risks in International Markets

A. Geopolitical Risk

War, terrorism, sanctions.

B. Economic Policy Risk

Changes in:

Taxes

Trade tariffs

Government spending

C. Currency Risk

Sudden currency crashes affect global trade.

D. Interest Rate Risk

Rapid rate hikes cause:

Stock market crash

Bond market volatility

Capital flight from emerging markets

E. Commodity Price Shock

Crude oil spikes can trigger global recession fears.

F. Systemic Risk

Banking crisis, global debt crisis, or recession.

8. Future Trends Shaping International Markets

1. AI & Technology Dominance

AI, cloud computing, EVs, semiconductors will drive global market cycles.

2. De-dollarization Debate

Countries exploring alternative settlement systems could impact USD strength.

3. Supply Chain Realignment

Shift from China to India, Vietnam, Mexico.

4. Green Energy Revolution

Solar, hydrogen, EV batteries creating new global winners.

5. Digital Currencies

CBDCs (Central Bank Digital Currencies) will reshape global payments & forex markets.

Conclusion