$DOGE looking good hereDogecoin, considering the strong hype around meme coins, Elon Musk’s support, and its strong uptrend on the weekly timeframe, could be a good buy opportunity.

It's currently sitting on the 55 EMA and also at the 61% Fibonacci level, providing strong support.

I’ll wait for its reaction to see how the weekly candlestick closes.

Elonmusk

Under 3-Minute Deep Dive Into Tesla (TSLA) – Big Move ComingTesla just pulled back to $320 on the weekly chart, and this is where things get interesting. If buyers step in, we could see a strong push to $370, and if that breaks, $397 and even $417 are in play.

But here’s the flip side—if Tesla loses $320, things could unravel fast, and $250 might not be far off.

I’m watching this level closely because the next move could be huge.

Kris/Mindbloome Exchange

Trade Smarter Live Better

DOGE - Time to buy again!The price has formed a Triangle on the 4h time frame, and if it breaks out, it can drive the price up to around $0.30.

Give me some energy !!

✨We spend hours finding potential opportunities and writing useful ideas, we would be happy if you support us.

Best regards CobraVanguard.💚

_ _ _ _ __ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

✅Thank you, and for more ideas, hit ❤️Like❤️ and 🌟Follow🌟!

⚠️Things can change...

The markets are always changing and even with all these signals, the market changes tend to be strong and fast!!

TSLA in Free Fall: How Low Will It Go ?Tesla is in free fall – and so far, there’s no sign of a turnaround. The 38.2% retracement zone has been hit, but let’s be honest: there’s no real bounce yet. Here’s why I expect the stock to drop further towards $360 – and how I’m positioning my entries.

Since mid-December, NASDAQ:TSLA has been in a clear downtrend on lower time frames, with no serious buying momentum yet. My first entry is already set as a limit order just below current support. If sellers keep the pressure on, a second entry below the untouched VWAP could make sense – with a tight stop in case TSLA takes another dive.

I’m staying on top of this and ready to adjust, but one thing’s for sure: The moment TSLA shows it’s done bleeding, it's going to send higher!

Tesla Stock Rattled as Insiders Dump Shares. What’s Going On?EV maker’s sales in Europe have made a sharp U-turn this year with some regions selling half the volumes from a year ago. Is Musk’s political ambition causing car buyers to look elsewhere for electric wheels?

Tesla stock TSLA is off to a bumpy start of the year with 10% shaved off its market valuation since the first trading bell of 2025. It’s all likely tied to Elon Musk’s shifting focus from his electric-car giant and into US politics (and, some would say, beyond that and into European affairs).

To make matters worse, key insiders and directors dumped tons of shares this month, cashing out cold hard dollars. Elon Musk’s brother, Kimbal Musk, who’s a Tesla board member, together with two other key figures, Robyn Denholm and chief financial officer Vaibhav Taneja, sold roughly 200,000 shares.

Kimbal Musk offloaded 75,000 shares worth $27.6 million on February 6. Before that, on February 3, Denholm sold 112,390 shares worth more than $43 million. On the same day, Taneja parted ways with 7,000 shares worth $2.8 million.

The share sale is happening at a time when it’s getting increasingly difficult for Tesla to keep its brand equity out of Elon Musk’s public image. In January, Musk was making headline after headline on the politics pages of big media outlets.

His efforts to reshape the White House administration spilled over into interfering with UK politics (where he attacked UK Prime Minister Keir Starmer over his alleged involvement with “mass rapes in exchange for votes” ).

The Tesla CEO also hosted a discussion on X with Germany’s far-right candidate Alice Weidel. It happened about a month before Germany’s federal election on February 23. The live event pulled in roughly 100,000 streamers and sparked a debate over whether it was right to give a free platform to a far-right political party of a foreign country. There’s also Musk’s gesture likened to a Nazi salute he pulled off at Trump’s inauguration — that one really turned heads globally.

Enough politics, let’s dive into the numbers.

Tesla sales were shockingly bad in January. All around Europe, car buyers opted for cheaper Chinese alternatives in a sea of looming competition in the auto industry .

In the UK, sales dipped about 8% from last year’s January. Chinese EV maker BYD BYD saw a massive jump by 550% to 1,614 cars sold. In Germany, sales of Tesla vehicles dropped 60%, while BYD sales rose 69%. France logged a 63% decline in sales of Tesla while Spain saw the steepest drop of 75%. Norway registered a 38% drop in Tesla sales while Tesla’s market in Sweden shrunk 44%. In China, where Tesla commands a towering presence, sales were down 11.5% in the first month of 2025.

Moving outside Europe and across the Atlantic — California marked a decline in Tesla sales to the tune of 11.6%. It was the only carmaker with tumbling sales in the state.

"All of the decrease in the state market last year was attributable to Tesla, which had an 11.6 percent decline," the California New Car Dealers Association said. "Registrations for all other brands increased 1.4 percent."

By the looks of it, Tesla isn’t in a good place fundamentally and shares are down 28% from their record high in December. It’s also coming from a pretty battering fourth quarter where profits plunged 71% while sales barely made it above the flatline with a 2% growth year over year.

Do you believe Tesla’s fortunes are tied to Elon Musk’s ventures into politics? And if you had to choose, are you long or short Tesla? Share your thoughts below!

VINE/USDT IS THIS THE LONG WAITING BREAK TO $0,50 Whales enterPreviously, we tracked Vine's journey from a lower price point to its peak target of over $0.30. Now, Vine is presenting a new opportunity, with a strong potential to aim for $0.50 in the near future.

If this is the bottom as it looks, then there is a high chance this coin could explode to $0,50 in the coming time. The increased volume will go faster after $0,15

We will closely monitor Vine's progress step by step as it continues its upward trajectory.

If there is a launch coming at X, this could be 1 volume shot target. (Elon should know more than we know.

As always, remember to manage your risk effectively, as this update is for informational purposes only and does not constitute trading advice.

TSLA Main Trend 02 2025Logarithm. Time frame 1 month (no need for less). Chart until 2031

🟢At the moment we are running a big triangle that broke through upwards .

🔄 There is a rollback now , to retest the breakout zone. All according to technical analysis, due to the super success of the company and the liquidity of its shares. As for me, the retest should be successful, and then the trend will continue.

🔴But, they can do, like in the last cycle (I specifically highlighted this and showed %), a reset (for some grandiose news) and only then a reversal. If this happens, remember, this is a "temporary phenomenon". Do not play locally in shorts, the main trend is bullish, and it will clearly dominate in the long term.

Fundamental analysis. Competition with BYD.

That's why I'll write a lot of text about how this will greatly affect the price of TSLA shares in the future (real supply/demand) due to trade wars for sales markets.

1️⃣ The only competitor in the world is only the Chinese BYD . Which will become an order of magnitude stronger for TSLA in monetary terms and the popularity of more technologically advanced and affordable cars. Its main advantage, why it can give a cheaper price for a higher quality product, is complete control over the production of the most expensive unit of an electric car - batteries. From the extraction of raw materials for production to the assembly of the battery, without intermediaries. But, it is worth noting that the future super giant BYD will be denied access (as is currently partially the case) to countries where politics is subject to US influence.

This is the so-called "gray zone" where a "trade war" will develop for the sale of products. The one who pays more will win, or their government (USA or China) will use greater leverage. For example, as now, in Brazil. The construction of the BYD plant is closed due to "inhumane working conditions" (and this is in a company with 500 billion in capital) in an important region (Latin America), where "the enemy does not sleep" and plans to begin construction of TSLA-Brazil in 2026. You probably understand what the matter is...

The main “trade battle” will naturally take place for the European market . The European electric car industry will not be competitive with TSLA and BYD (two main flagship companies in the transition of internal combustion engines to electric transport on earth).

It is worth noting that TSLA is now very popular in China. There is a large plant (Shanghai). 40,000 pre-orders for the new Model Y. The Chinese government does not interfere with this. But if unfair play continues in other markets, it is unlikely that TSLA will not be thrown out of China. Competition must be fair. Duties on cars are similar. So far, this is conditionally observed, but there are negative signs from the United States.

2️⃣ The reality of the launch of a new hydrogen engine from Toyota. There are rumors that it is being developed jointly with BMW. This is a completely new level of hydrogen engines. Instead of refueling with hydrogen, distilled water will be poured into the tank. The engine converts it into hydrogen. Serial production will allegedly begin in 2028, when the first hydrogen BMW models will roll off the assembly line.

In some sources, also together with Mercedes-Benz, and even Porsche. Perhaps this is just a news teaser for a potential future buyer, to save the catastrophic decline in sales last year and this year, due to the virtual loss (due to the inability to compete) of the world's largest sales market — China.

It is probably logical to assume that the release of this hydrogen engine to the masses will negatively affect TSLA shares. Provided that TSLA does not follow this fuel trend. My opinion is that they are unlikely to give mass production to something like this. It is like the mass production of electric cars in the 1990s and 2000s, in the era of the reign and monopoly of the hegemonies of oil capital, and as a consequence of internal combustion engines.

3️⃣ Massive power outages around the world. The next point is probably more of a “conspiracy theory”, but I can't help but mention the extremely unlikely scenario of impact on stock prices (a sharp drop).

It is worth noting that the shares of any company that is associated with electricity are extremely “afraid” of a massive power outage and its rise in price, especially accompanied by extremely negative news. If, at least for a week, with a significant transition to electric vehicles (for example, 20-30%) in a large city there are power outages, then this can have an extremely negative impact on the shares of companies associated with the production of electric vehicles and components for them, which is logical. To scare and save and, as a result, "get your way".

4️⃣ Also, a gradual but rapid rise in the price of electricity , as a result of some events or policies, will discourage people from using electric vehicles (they will buy and drive less). This could also have a negative impact on the earnings of these companies like TSLA and BYD, and as a result on their speculative assets.

PS . Of all the points, probably the most important is 1 (real competition and trade war). Then 2, after 2028. Before that, I think TSLA and other companies related to electric cars will pump up a lot.

TESLA is overvalued and here is why - waiting for 270Tesla is overvalued, especially when compared to traditional metrics like P/E ratio. We have P/E 190 atm. If we compare Tesla to other EV companies, Tesla’s valuation might appear inflated. For example, companies like Rivian, Lucid, and NIO have been hyped similarly, but most haven’t shown the same level of growth and revenue.

Investors are betting on Tesla’s dominance in electric vehicles, energy, and other sectors, which drives the high valuation. Tesla's stock is also closely tied to Elon Musk’s reputation, decisions, and Twitter presence.

Tesla has become more profitable in recent years, but many argue that it’s still a growth company where profits aren't the main focus. The question is whether the current market cap is justified based on actual cash flow and profitability - of course NO.

Tesla was created as a startup and truly revolutionized the auto industry, but its stock is now worth several hundred times more than it is as a technology-driven car manufacturer. Future expectations have always driven the stock market, and this phenomenon will continue to accompany us. However, I believe that in terms of future expectations, Tesla, as an automaker, has long since exhausted its potential, and its competitors have long been replicating Tesla's "miracle," but in much more efficient ways.

A vivid example of this is the recent story of ChatGPT and DeepSeek. I am confident that sooner or later, Tesla will also become a "victim" of this.

On the other hand, Elon Musk’s reputation, political involvement, and trade wars—all of these are potential bombs placed under Tesla.

Tesla - Another +100% After This Breakout!Tesla ( NASDAQ:TSLA ) can still double from here:

Click chart above to see the detailed analysis👆🏻

With Elon Musk actually becoming the richest person on this planet, Tesla is simultaneously attempting another all time high breakout. All the recent bullish momentum could further fuel this rally, leading to new all time highs and another 2x in Tesla's market cap.

Levels to watch: $450, $900

Keep your long term vision,

Philip (BasicTrading)

Do you think I'm joking ???As you can see, the price is forming two bullish patterns on the 4h timeframe, If my view is correct, DOGE will rise to $0.53 .

And if this pattern is correct and breaks, higher targets are possible.

Give me some energy !!

✨We spend hours finding potential opportunities and writing useful ideas, we would be happy if you support us.

Best regards CobraVanguard.💚

_ _ _ _ __ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

✅Thank you, and for more ideas, hit ❤️Like❤️ and 🌟Follow🌟!

⚠️Things can change...

The markets are always changing and even with all these signals, the market changes tend to be strong and fast!!

XRP Parabolic !?As in recent posts, we’ve seen XRP climb from .042 towards $1,$2 and now consolidating a bullish structure in the $2.80-$3.25 range.

With the recent inauguration, new laws being passed including the introductory crypto bill. An XRP ETF has been filed just in the past 48 hours. I expect the SEC battle to be done soon as well as the XRP ETF being made available and accepted. From there i will speculate but like I said before. The trump admin and xrp will lead to an open world source for crypto reserves to be built worldwide. Which will increase the price beyond the point of market cap.

This is just a prediction, NFA. Good luck!

Short term Possible double correction in progress, looking for more upside as long as current lows hold

TSLA Tesla Options Ahead of EarningsIf you haven`t bought TSLA before the previous earnings:

Now analyzing the options chain and the chart patterns of TSLA Tesla prior to the earnings report this week,

I would consider purchasing the 400usd strike price Calls with

an expiration date of 2025-1-31,

for a premium of approximately $16.35.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Vine/USDT PRICE PREDICTION 2025 $3.50 2025Vine/USDT PRICE PREDICTION 2025

Means for long-term follow, and where the possibility is for this coin 2025

The best way to enter volume is in steps.

Depending on the 2025 protection for this coin, we expect this is a good chance this coin can gain over $3.50

It can take time, and the price can even breakdown more before it can increase

This update will stay a prediction, do always your study and manage the risk.

Expect nothing from the market, but more see the possibilities.

DOGECOIN - Time to buy again!As you can see, the price is forming two bullish patterns on the 4h timeframe, If my view is correct, DOGECOIN will rise to $0.50 .

And if this pattern is correct and breaks, higher targets are possible.

Give me some energy !!

✨We spend hours finding potential opportunities and writing useful ideas, we would be happy if you support us.

Best regards CobraVanguard.💚

_ _ _ _ __ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

✅Thank you, and for more ideas, hit ❤️Like❤️ and 🌟Follow🌟!

⚠️Things can change...

The markets are always changing and even with all these signals, the market changes tend to be strong and fast!!

DOGE : Break .46 to $1.4 or Plunge to .23?Hey trading family

DOGE could soar to $1.4 if it goes over .46 cents. If it drops below .30, it might fall to .23 cents.

If you found this analysis valuable, boost it with a like, share: I appreciate the love or send me a DM if you need help.

Kris/Mindbloome Exchange

Trade What You See

TRUMPUSDT Trade Log As Trump steps up to take the oath,

Markets buzz with fervent growth.

TRUMPUSDT's on the rise,

A digital bet beneath the skies.

Inauguration's pomp and cheer,

Crypto traders far and near.

With hopeful eyes, they watch and see,

What today's trade will come to be.

ELONUSDT Trade LogBought some ELON, took the leap,

A moonshot dream, in charts so deep.

To the stars, it’s set to fly,

Hold tight, let the profits rise high.

Through the dips, I’ll stand my ground,

With each new wave, more gains are found.

In the space where rockets zoom,

ELON’s the ticket, to break the gloom.

Kekius Maximus: Fibonacci Levels and Key Support ZonesThis coin became famous after Elon Musk changed his Twitter account name!

But what is going on exactly:

Key Resistance Zone:

The resistance around $0.21–$0.22 has been tested previously and remains a significant barrier for upward movement. If the price manages to break this zone, we could see a continuation toward higher Fibonacci extensions.

Fibonacci Levels:

The retracement levels marked in the chart highlight the price's potential correction zones. The 0.618 retracement level ($0.061) aligns closely with the lower support zone, making it a critical area to watch for buyers to step in.

Support Zone:

The $0.045–$0.061 zone is a major area of interest for potential accumulation. This area aligns with the Fibonacci golden pocket, often viewed as a prime area for price reversals in bullish setups.

Potential Scenarios:

If the price revisits the lower support zone and buyers defend it, we could see a bounce back toward the key resistance at $0.21.

Alternatively, if the price consolidates above the 0.382 level ($0.094) and breaks through the resistance without retesting the lower levels, it may indicate strong bullish momentum.

_____________________________________

Conclusion:

Traders should monitor the support zone around $0.045–$0.061 closely for potential long positions. Breaking the $0.21–$0.22 resistance could open doors for a significant rally. Caution is advised if the price falls below $0.045, as it might signal further downside momentum.

Doge's Journey to the MOON? $1.42 and Beyond Morning Trading Family

Hold onto your leashes, traders! If our 30 cents at supports holds firm, we're in for an epic ride:

First Stop: 50 cents - A nice little hop.

Next Leap: 61 cents - The momentum builds.

Gearing Up: 83 cents - We're picking up speed.

Moonshot: $1.42 - Aim for the stars!

Keep your eyes on the charts, and let's see where this meme coin takes us next!

If you found this useful: boost, share, like, and comment. I appreciate all the support! If you're struggling as a trader, I get it - I've been there myself. Jump in, send me a DM or head to my profile; I'm more than happy to help.

Kris/Mindbloome Exchange

Trade What You See

Tesla Update: Navigating the Road to $440Morning Trading Family

Tesla's journey is heating up as we aim for the $440 target. But buckle up, because we've got some resistance zones to watch:

First Stop: $427 - This could be where the ride gets a bit turbulent. Expect some market reactions here.

Next Challenge: $435.35 - Another potential bump in the road. Will we see a correction, or will Tesla's momentum carry us straight through?

The depth of any correction at these levels is still up in the air, but keep your eyes peeled. If the market punches through these resistances, $440 might just be in our sights sooner than expected!

If you found this useful: boost, share, like, and comment. I appreciate all the support! If you're struggling as a trader, I get it - I've been there myself. Jump in, send me a DM or head to my profile; I'm more than happy to help.

Kris/Mindbloome Exchange

Trade What You See

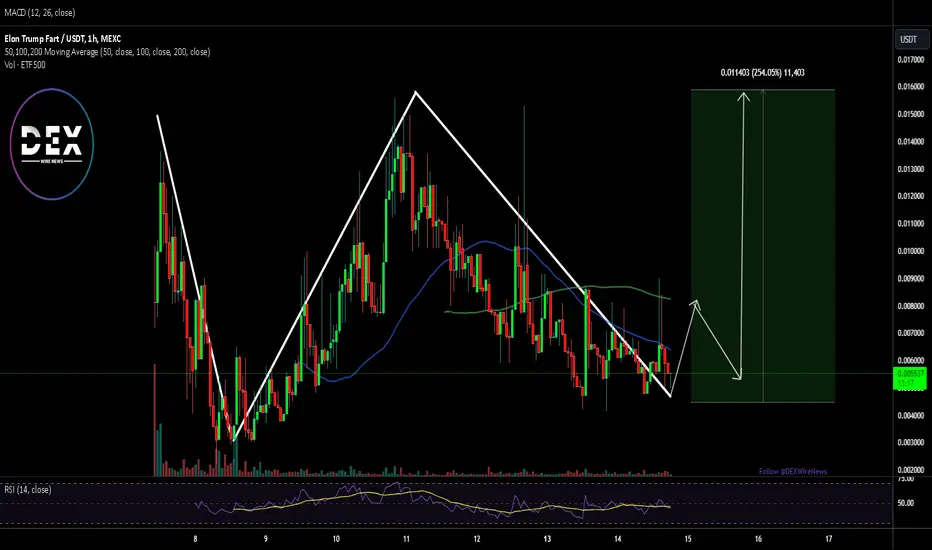

ETF500 Coin Set for a 250% Surge Amidst Neck & Shoulder PatternThe Elon Trump Fart (ETF500) token has been making waves in the meme coin market, driven by its unique blend of political satire and community-driven momentum. This token, inspired by the Fartcoin deployer narrative, has been through significant market fluctuations but is now showing signs of a potential bullish reversal.

Meme Coin Narrative:

ETF500 stands out by merging two influential figures, Elon Musk and Donald Trump, into a politically charged meme token. This strategy taps into a broad audience that finds humor and engagement in the politifi narrative.

From its inception, ETF500 has been a community-driven project. The CTO has been pivotal in shaping the token’s direction, fostering transparency and inclusivity.

Market Metrics

- Current Price: 61.09% below its all-time high of $0.01462 (recorded on January 10, 2025).

- All-Time Low: $0.002335 (recorded on January 8, 2025), with the current price up by 143.57%.

- Market Cap: $5,684,503, ranking #2246 on CoinGecko.

Where to Buy ETF500

ETF500 tokens can be traded on decentralized exchanges like MEXC, Raydium and Meteora. The most active trading pair, ETF500/SOL, indicates strong liquidity and accessibility for traders.

Technical Analysis

As of this writing, ETF500USDT is down 19%, trading within a falling wedge pattern. This bearish setup often precedes a bullish breakout, signaling potential opportunities for traders.

Neck and Shoulder Pattern:

A developing neck and shoulder pattern hints at a bullish reversal. However, the preceding shoulder formation is incomplete, placing ETF500 in a strategic buy zone for early investors. Similarly, the Relative Strength Index (RSI) indicates oversold conditions, suggesting that ETF500 has the potential to break new highs as buying momentum builds.

- Key Levels:

Resistance: The token faces resistance near the $0.0095 level, which aligns with the neckline of the pattern.

Support: Strong support is observed at $0.0052, providing a safety net for traders.

Potential for Growth

The combination of community engagement, unique narrative appeal, and favorable technical patterns positions ETF500 for significant growth. If the bullish reversal materializes, the token could see a surge of up to 250%, capturing the attention of meme coin enthusiasts and seasoned traders alike.

Conclusion

Elon Trump Fart (ETF500) represents the fusion of humor, community, and market strategy in the crypto space. While its price trajectory has been volatile, the current technical and fundamental indicators point to a promising future. As always, investors should conduct their own research and consider the inherent risks before diving in.

Bullish/Bearish Sentiment We saw #BTC last hit it's double top 209 days after making an ATH 64k in April and topping out in Nov.

VeChain also took around 200 days to revisit higher lows.

[BULLS}

Elliot Wave Theory:

It appears that we are in the next 2-3 wave

Regardless of the narrative, the trend is showing bearish in the short term. I have HODL positions but short until we hit our buy zones keeping a close eye on what #BTC and #ETH do.

CRYPTOCAP:ETH is in a channel and appears to be falling out.

If we dig deeper watch 3k as a psychological area of support, CRYPTOCAP:BTC will be around 95k. For NYSE:VET we see $0.04 being a key level of support in our first buy zone, secondary we are looking for around $0.033.

Once these levels hold I will flip my sentiment and continue to long into this year with our bullish commander and chief stepping into office.

#Donaldtrump

If November repeats itself with this day we could be hopeful for another 300% but remain reserved with our PT's on the way up because.

"You never go broke taking a profit."

HNY #vechain fam.

Don't over-leverage, set your SL before bed.

@VEREKTION