DMI + HMA - No Risk ManagementDMI (Directional Movement Index) and HMA (Hull Moving Average)

The DMI and HMA make a great combination, The DMI will gauge the market direction, while the HMA will add confirmation to the trend strength.

What is the DMI?

The DMI is an indicator that was developed by J. Welles Wilder in 1978. The Indicator was designed to identify in which direction the price is moving. This is done by comparing previous highs and lows and drawing 2 lines.

1. A Positive movement line

2. A Negative movement line

A third line can be added, which would be known as the ADX line or Average Directional Index. This can also be used to gauge the strength in which direction the market is moving.

When the Positive movement line (DI+) is above the Negative movement line (DI-) there is more upward pressure. Ofcourse visa versa, when the DI- is above the DI+ that would indicate more downwards pressure.

Want to know more about HMA? Check out one of our other published scripts

What is this strategy doing?

We are first waiting for the DMI to cross in our favoured direction, after that, we wait for the HMA to signal the entry. Without both conditions being true, no trade will be made.

Long Entries

1. DI+ crosses above DI-

2. HMA line 1 is above HMA line 2

Short Entries

1. DI- Crosses above DI+

2. HMA line 1 is below HMA lilne 2

Its as simple as that.

Conclusion

While this strategy does have its downsides, that can be reduced by adding some risk manegment into the script. In general the trade profitability is above average, And the max drawdown is at a minimum.

The settings have been optimised to suite BTCUSDT PERP markets. Though with small adjustments it can be used on many assets!

Algotrading

Ichimoku Cloud Strategy Long Only [Bitduke]Slightly modificated and optimized for Pine Script 4.0, Ichimoku Cloud Strategy which, suddenly, good suitable for the several crypto assets.

Details:

Enter position when conversion line crosses base line up, and close it when the opposite happens.

Additional condition for open / close the trade is lagging span, it should be higher than cloud to open position and below - to close it.

Backtesting:

Backtested on SOLUSDT ( FTX, Binance )

+150% for 2021 year, 8% dd

+191% for all time, 32% dd

Disadvantages:

- Small number of trades

- Need to vary parameters for different coins (not very robust)

Should be tested carefully for other coins / stock market. Different parameters could be needed or even algo modifications.

Strategy doesn't repaint.

Stochastic TrendDear community,

I've made another simple trading bot for you to use. This bot is based on the Stochastic Oscillator. It only produces long trades currently.

I changed the oscillation period to a much longer one, which in turn creates opportunities to trade long term trends.

The bot goes long when the Entry lines is crossed from below and it will close its long position once the Exit line has been crossed from above.

Strategy NNFX Tester Strategy NNFX, Baseline, QQEs Fast C1, Slow C2, ATR, Volume and Exit

This is a Strategy Tester designed to work with Study (Alerts) of the same.

At time of creation based on Revision 8 of the Study.

DO NOT USE the Currency/Money Management section under settings. use the position sizing under "Inputs" - "Money Management" - "Risk per trade" which is defaulted to 2%

This has adjustable Baselines, Exits, ATR calculations, C1 and C2 are currently QQE & QQE Histo with adjustable settings but I'll include more choice of C1 & C2 as time goes on.

Find settings that work for you, then move them over to the Study version for best results.

Forward plans are to add much more options to both Alert/Strategy.

If anyone wants to collaborate or anything hit me up.

Keltner Channel [LINKUSDT] 1HThis is a long-only strategy tested on LINK/USDT, 1 hour bar, from Feb 2019. The entry is determined by the breakout of upper Keltnel Channel and when the +DI is higher than 32. Instead of a fixed stop-loss from the original script , I change the exit to the middle band of the Keltnel Channel. 1st profit target will close 20% of the position. 2nd profit target will close 30% of the position. While the remaining 50% position will be closed when the price closes below the middle band of the Keltnel Channel, to take advantage of big trend. All parameters are adjustable. I added another option to enable or disable the ribbon trend filter.

My thoughts: For the same period, LINK appreciated 3000%. So I guess most in and out strategies couldn’t beat a buy and hold strategy during this period. But this doesn’t mean that this strategy is not feasible as each strategy is designed to only take advantage of a certain pattern or behavior of the market. Also, short term strategies allow you to use leverage and hence enable you to use you capital efficiently. Commission is set to 0.1%, taking account of the slippage.

Suggestion: Please perform walk forward analysis before you use real money for trading. Parameters need to be adjusted from time to time depends on your analysis. Can try using ATR for profit targets as over a longer term, the volatility might drop hence a high fixed % profit targets might not be realistic.

Any suggestions are welcome!

BTC and ETH Long strategy - version 1I will start with a small introduction about myself. I'm now trading cryto currencies manually for almost 2 years. I decided to start after watching a documentary on the TV showing people who made big money during the Bitcoin pump which happened at the end of 2017.

The next day, I asked myself "Why should I not give it a try and learn how to trade".

This was in February 2018 and the price of Bitcoin was around 11500USD.

I didn't know how to trade. In fact, I didn't know the trading industry at all.

So, my first step into trading was to open an account with a broken. Then I directly bought 200$ worst of BTC . At that time, I saw the graph and thought "This can only go back in the upward direction!" :)

I didn't know anything about Stop loss, Take profit and Risk management.

Today, almost 2 years after, I think that I know how to trade and can also confirm that I still hold this bag of 200$ of bitcoin from 2018 :)

I did spend the 2 last years to learn technical analysis , risk management and leverage trading.

Today (14/05/2020), I know what I'm doing and I'm happy to see that the 2 last years have been positive in terms of gains. Of course, I did not make crazy money with my saving but at least I made more than if I would have kept it in my bank account.

Even if I like trading, I have a full time job which requires my full energy and lots of focus, so, the biggest problem I had is that I didn't have enough time to look at the charts.

Also, I realized that sometimes, neither technical analysis , nor fundamentals worked with crypto currency (at least for short time trading). So, as I have a developer background I decided to try to have a look at algo trading.

The goal for me was neither to make complex algos nor to beat the market but just to automate my trading with simple bot catching the big waves.

I then started to take a look at TV pine script and played with it.

I did my first LONG script in February 2020 to Long the BTC Market. It has some limitations but works well enough for me for the time being. Even if the real trades will bring me half of what the back testing shows, this will still be a lot more than what I was used to win during the last 2 years with my manual trading.

So, here we are! Below you will find some details about my first LONG script. I'm happy to share it with you.

Feel free to play with it, give your comments and bring improvements to it.

But please note that it only works fine with the candle size and crypto pair that I have mentioned below. If you use other settings this algo might loose money!

- Crypto pairs : XBTUSD and ETHXBT

- Candle size: 2 Hours

- Indicator used: Volatility , MACD (12, 26, 7), SMA (100), SMA (200), EMA (20)

- Default StopLoss: -1.5%

- Entry in position if: Volatility < 2%

AND MACD moving up

AND AME (20) moving up

AND SMA (100) moving up

AND SMA (200) moving up

AND EMA (20) > SAM (100)

AND SMA (100) > SMA (200)

- Exit the postion if: Stoploss is reached

OR EMA (20) crossUnder SMA (100)

Here is a summary of the results for this script:

XBTUSD : 01/01/2019 --> 14/05/2020 = +107%

ETHXBT : 01/01/2019 --> 14/05/2020 = +39%

ETHUSD : 01/01/2019 --> 14/05/2020 = +112%

It is far away from being perfect. There are still plenty of things which can be done to improve it but I just wanted to share it :) .

Enjoy playing with it....

Coinbase_3-MIN_HFT-StrategyThis conceptual strategy trades against the short-term trend. The first position can be either long or short.

In the short-term, prices fluctuate up and down on wide spread exchanges.

And if the price moves to one side, the price tends to return to its original position momentarily.

This strategy set stop order. Stop price is calculated with upper and lower shadows.

Combo Backtest 123 Reversal & CMOaDisparity Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The related CMOaDisparity Index article is copyrighted material from Stocks & Commodities Dec 2009

My strategy modification.

WARNING:

- For purpose educate only

- This script to change bars colors.

N Bars Down Backtest Evaluates for n number of consecutive lower closes. Returns a value

of 1 when the condition is true or 0 when false.

WARNING:

- For purpose educate only

- This script to change bars colors.

N Bars Up Backtest Evaluates for n number of consecutive higher closes. Returns a value

of 1 when the condition is true or 0 when false.

WARNING:

- For purpose educate only

- This script to change bars colors.

HatiKO EnvelopesPublished source code is subject to the terms of the GNU Affero General Public License v3.0

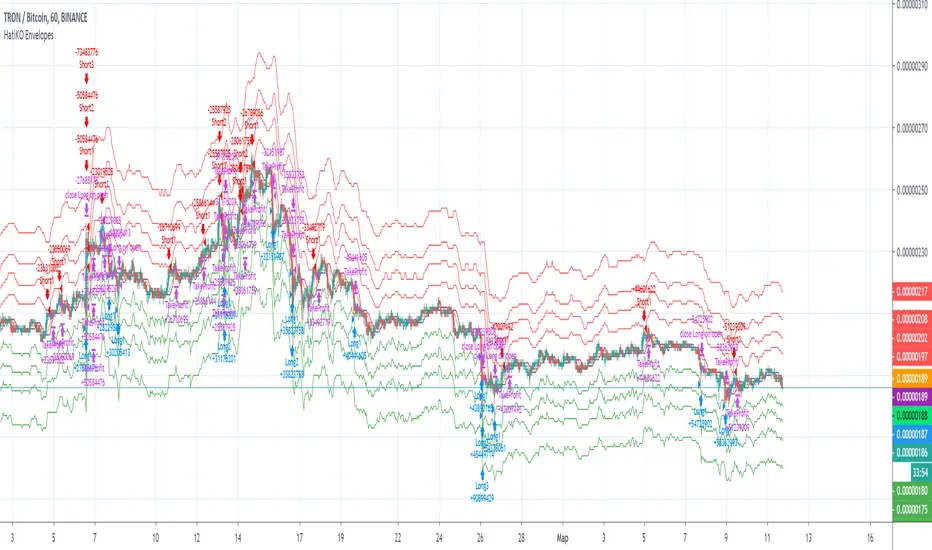

This script describes and provides backtesting functionality to internal strategy of algorithmic crypto trading software "HatiKO bot".

Suitable for backtesting any Cryptocurrency Pair on any Exchange/Platform, any Timeframe.

Core Mechanics of this strategy are based on theory of price always returning to Moving Average + Envelopes indicator (Moving_average_envelope from Wiki)

Developement of this script and trading software is inspired by:

"Essential Technical Analysis: Tools and Techniques to Spot Market Trends" by Leigh Stevens (published on 12th of April 2002)

"Moving Average Envelopes" by ChartSchool, StockCharts platform (published on 13th of April 2015 or earlier)

"Коля Колеснік" from Crypto Times channel ("Метод сетка", published on 19th of August 2018)

"3 ways to use Moving Average Envelopes" by Rich Fitton, published on Trader's Nest (published on 28st of November 2018 or earlier)

noro's "Robot WhiteBox ShiftMA" strategy v1 script, published on TradingView platform (published on 29th of August 2018)

"Moving Average Envelopes: A Popular Trading Tool" Investopedia article (published 25th of June 2019)

and KROOL1980's blogpost on Argolabs ("Гридерство или Сетка как источник прибыли на форекс", published on 27th of February 2015)

Core Features:

1) Up to 4 Envelopes in each direction (Long/Short)

2) Use any of 6 different basis MAs, optionally use different MAs for Opening and Closure

3) Use different Timeframes for MA calculation, without any repainting and lookahead bias.

4) Fixed order size, not Martingale strategy

5) Close open position earlier by using Deviation parameter

6) PineScript v4 code

Options description:

Lot - % from your initial balance to use for order size calculation

Timeframe Short - Timeframe to use for Short Opening MA calculation, can be chosen from dropdown list, default is Current Graph Timeframe

MA Type Short - Type of MA to use for Short Opening MA calculation, can be chosen from dropdown list, default is SMA

Data Short - Source of Price for Short Opening MA calculation, can be chosen from dropdown list, default is OHLC4

MA Length Short - Period used for Short Opening MA calculation, should be >=1, default is 3

MA offset Short - Offset for MA value used for Short Envelopes calculation, should be >= 0, default is 0

Timeframe Long - Timeframe to use for Long Opening MA calculation, can be chosen from dropdown list, default is Current Graph Timeframe

MA Type Long - Type of MA to use for Long Opening MA calculation, can be chosen from dropdown list, default is SMA

Data Long - Source of Price for Long Opening MA calculation, can be chosen from dropdown list, default is OHLC4

MA Length Long - Period used for Long Opening MA calculation, should be >=1, default is 3

MA offset Long - Offset for MA value used for Long Envelopes calculation, should be >= 0, default is 0

Mode close MA Short - Enable different MA for Short position Closure, default is "false". If false, Closure MA = Opening MA

Timeframe Short Close - Timeframe to use for Short Position Closure MA calculation, can be chosen from dropdown list, default is Current Graph Timeframe

MA Type Close Short - Type of MA to use for Short Position Closure MA calculation, can be chosen from dropdown list, default is SMA

Data Short Close - Source of Price for Short Closure MA calculation, can be chosen from dropdown list, default is OHLC4

MA Length Short Close - Period used for Short Opening MA calculation, should be >=1, default is 3

Short Deviation - % to move from MA value, used to close position above or beyond MA, can be negative, default is 0

MA offset Short Close - Offset for MA value used for Short Position Closure calculation, should be >= 0, default is 0

Mode close MA Long - Enable different MA for Long position Closure, default is "false". If false, Closure MA = Opening MA

Timeframe Long Close - Timeframe to use for Long Position Closure MA calculation, can be chosen from dropdown list, default is Current Graph Timeframe

MA Type Close Long - Type of MA to use for Long Position Closure MA calculation, can be chosen from dropdown list, default is SMA

Data Long Close - Source of Price for Long Closure MA calculation, can be chosen from dropdown list, default is OHLC4

MA Length Long Close - Period used for Long Opening MA calculation, should be >=1, default is 3

Long Deviation - % to move from MA value, used to close position above or beyond MA, can be negative, default is 0

MA offset Long Close - Offset for MA value used for Long Position Closure calculation, should be >= 0, default is 0

Short Shift 1..4 - % from MA value to put Envelopes at, for Shorts numbers should be positive, the higher is number, the higher should be Shift position, example: "Shift 1 = 1, shift 2 = 2, etc."

Long Shift 1..4 - % from MA value to put Envelopes at, for Longs numbers should be negative, the lower is number, the lower should be Shift position, example: "Shift 1 = -1, shift 2 = -2, etc."

From Year 20XX - Backtesting Starting Year number, only 20xx supported as script is cryptocurrency-oriented.

To Year 20XX - Backtesting Final Year number, only 20xx supported as script is cryptocurrency-oriented.

From Month - Years starting Month, optional tweaking, changing not recommended

To Month - Years ending Month, optional tweaking, changing not recommended

From day - Months starting day, optional tweaking, changing not recommended

To day - Months ending day, optional tweaking, changing not recommended

Graph notes:

Green lines - Long Envelopes.

Red lines - Short Envelopes.

Orange line - MA for closing of Short positions.

Lime line - MA for closing of Long positions.

**************************************************************************************************************************************************************************************************************

Опубликованный исходный код регулируется Условиями Стандартной Общественной Лицензии GNU Affero v3.0

Этот скрипт описывает и предоставляет функции бектеста для внутренней стратегии алгоритмического программного обеспечения "HatiKO bot".

Подходит для тестирования любой криптовалютной пары на любой бирже/платформе, на любом таймфрейме.

Кор-механика этой стратегии основана на теории всегда возвращающейся к значению МА цены с использованием индикатора Envelopes (Moving_average_envelope from Wiki)

Разработка этого скрипта и программного обеспечения для торговли вдохновлена следующими источниками:

Книга "Essential Technical Analysis: Tools and Techniques to Spot Market Trends" Ли Стивенса (опубликовано 12 апреля 2002 года)

«Moving Average Envelopes» от ChartSchool, платформа StockCharts (опубликовано 13 апреля 2015 года или раньше)

«Коля Колеснік» с канала Crypto Times («Метод сетка», опубликовано 19 августа 2018 года)

«3 ways to use Moving Average Envelopes» Рича Фиттона, опубликованные в «Trader's Nest» (опубликовано 28 ноября 2018 года или раньше)

Скрипт стратегии noro "Robot WhiteBox ShiftMA" v1, опубликованный на платформе TradingView(опубликовано 29 августа 2018 года)

«Moving Average Envelopes: A Popular Trading Tool», статья Investopedia (опубликовано 25 июня 2019 года)

Блог KROOL1980 из Argolabs («Гридерство или Сетка как источник прибыли на форекс», опубликовано 27 февраля 2015 года)

Основные особенности:

1) До 4-х Ордеров в каждом из направлении (Лонг / Шорт)

2) Выбор из 6-ти разных базовых МА, опционально используйте разные МА для открытия и закрытия.

3) Используйте разные таймфреймы для расчета MA, без перерисовки и "эффекта стеклянного шара".

4) Фиксированный размер ордера, а не стратегия Мартингейла

5) Возможность закрытия открытой позиции заблаговременно, используя параметр Deviation

6) Код реализован на PineScript v4

Описание параметров:

Lot - % от вашего первоначального баланса, используется при расчете размера Ордера

Timeframe Short - таймфрейм, используемый для расчета МА Открытия Шорт позиций, может быть выбран из списка, по умолчанию - таймфрейм текущего графика

MA Type Short - тип MA, используемый для расчета МА Открытия Шорт позиций, может быть выбран из списка, по умолчанию SMA

Data Short - источник цены для расчета МА Открытия Шорт позиций, может быть выбран из списка, по умолчанию OHLC4

MA Length Short - период, используемый для расчета МА Открытия Шорт позиций, должен быть >= 1, по умолчанию 3

MA Offset Short - смещение значения MA, используемого для расчета Шорт Ордеров, должно быть >= 0, по умолчанию 0

Timeframe Long - таймфрейм, используемый для расчета МА Открытия Лонг позиций, может быть выбран из списка, по умолчанию - таймфрейм текущего графика

MA Type Long - тип MA, используемый для расчета МА Открытия Лонг позиций, может быть выбран из списка, по умолчанию SMA

Data Long - источник цены для расчета МА Открытия Лонг позиций, может быть выбран из списка, по умолчанию OHLC4

MA Length Long - период, используемый для расчета МА Открытия Лонг позиций, должен быть >= 1, по умолчанию 3

MA Offset Long - смещение значения MA, используемого для расчета Лонг Ордеров, должно быть >= 0, по умолчанию 0

Mode close MA Short - Включает отдельное MA для закрытия Шорт позиции, по умолчанию «false». Если false, MA Закрытия = MA Открытия

Timeframe Short Close - таймфрейм, используемый для расчета МА Закрытия Шорт позиций, может быть выбран из списка, по умолчанию - таймфрейм текущего графика

MA Type Close Short - тип MA, используемый при расчете МА Закрытия Шорт позиции. Mожно выбрать из списка, по умолчанию SMA

Data Short Close - источник цены для расчета МА Закрытия Шорт позиций, может быть выбран из списка, по умолчанию OHLC4

MA Length Short Close - период, используемый для расчета МА Закрытия Шорт позиции, должен быть >= 1, по умолчанию 3

Short Deviation - % отклонения от значения MA, используется для закрытия позиции выше или ниже рассчитанного значения MA, может быть отрицательным, по умолчанию 0

MA Offset Short Close - смещение значения MA, используемого для расчета закрытия Шорт позиции, должно быть >= 0, по умолчанию 0

Mode close MA Long - Включает разные MA для закрытия Лонг позиции, по умолчанию «false». Если false, MA Закрытия = MA Открытия

Timeframe Long Close - таймфрейм, используемый для расчета МА Закрытия Лонг позиций, может быть выбран из списка, по умолчанию - таймфрейм текущего графика

MA Type Close Long - тип MA, используемый при расчете МА Закрытия Лонг позиции. Mожно выбрать из списка, по умолчанию SMA

Data Long Close - источник цены для расчета МА Закрытия Лонг позиций, может быть выбран из списка, по умолчанию OHLC4

MA Length Long Close - период, используемый для расчета МА Закрытия Лонг позиции, должен быть >= 1, по умолчанию 3

Long Deviation -% для перехода от значения MA, используется для закрытия позиции выше или ниже рассчитанного значения MA, может быть отрицательным, по умолчанию 0

MA Offset Long Close - смещение значения MA, используемого для расчета закрытия Лонг позиции, должно быть >= 0, по умолчанию 0

Short Shift 1..4 - % от значения MA для размещения Ордеров, для Шорт Ордеров должен быть положительным, чем выше номер, тем выше должна располагаться позиция Shift, например: «Shift 1 = 1, Shift 2 = 2 и т.д. "

Long Shift 1..4 - % от значения MA для размещения Ордеров, для Лонг Ордеров должно быть отрицательным, чем ниже число, тем ниже должна располагаться позиция Shift, например: «Shift 1 = -1, Shift 2 = -2, и т.д."

From Year 20XX - Год начала тестирования, из-за ориентированности на криптовалюты поддерживаются только значения формата 20хх.

To Year 20XX - Год окончания тестирования, из-за ориентированности на криптовалюты поддерживаются только значения формата 20хх.

From Month - Начальный месяц, опционально, менять не рекомендуется

To Month - Конечный месяц, опционально, менять не рекомендуется

From day - Начальный день месяца, опционально, менять не рекомендуется

To day - Конечный день месяца, опционально, менять не рекомендуется

Пояснения к графику:

Зеленые линии - Лонг Ордера.

Красные линии - Шорт Ордера.

Оранжевая линия - MA Закрытия Шорт позиций.

Лаймовая линия - MA Закрытия Лонг позиций.

Adaptive Price Zone Backtest The adaptive price zone (APZ) is a volatility-based technical indicator that helps investors

identify possible market turning points, which can be especially useful in a sideways-moving

market. It was created by technical analyst Lee Leibfarth in the article “Identify the

Turning Point: Trading With An Adaptive Price Zone,” which appeared in the September 2006 issue

of the journal Technical Analysis of Stocks and Commodities.

This indicator attempts to signal significant price movements by using a set of bands based on

short-term, double-smoothed exponential moving averages that lag only slightly behind price changes.

It can help short-term investors and day traders profit in volatile markets by signaling price

reversal points, which can indicate potentially lucrative times to buy or sell. The APZ can be

implemented as part of an automated trading system and can be applied to the charts of all tradeable assets.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & D_ELI (Ehlers Leading Indicator) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This Indicator plots a single

Daily DSP (Detrended Synthetic Price) and a Daily ELI (Ehlers Leading

Indicator) using intraday data.

Detrended Synthetic Price is a function that is in phase with the dominant

cycle of real price data. This one is computed by subtracting a 3 pole Butterworth

filter from a 2 Pole Butterworth filter. Ehlers Leading Indicator gives an advanced

indication of a cyclic turning point. It is computed by subtracting the simple

moving average of the detrended synthetic price from the detrended synthetic price.

Buy and Sell signals arise when the ELI indicator crosses over or under the detrended

synthetic price.

See "MESA and Trading Market Cycles" by John Ehlers pages 64 - 70.

WARNING:

- For purpose educate only

- This script to change bars colors.

Simple Price Momentum - How To Create A Simple Trading StrategyThis script was built using a logical approach to trading systems. All the details can be found in a step by step guide below. I hope you enjoy it. I am really glad to be part of this community. Thank you all. I hope you not only succeed on your trading career but also enjoy it.

docs.google.com

Combo Backtest 123 Reversal & Comparative Relative Strength This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Comparative Relative Strength Strategy for ES

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & EMA & Volume WeightingThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The related article is copyrighted material from Stocks & Commodities 2009 Oct

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & DMI & Moving Average This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The related article is copyrighted material from Stocks & Commodities Aug 2009

WARNING:

- For purpose educate only

- This script to change bars colors.

Kase Dev Stops Backtest The Kase Dev Stops system finds the optimal statistical balance between letting profits run,

while cutting losses. Kase DevStop seeks an ideal stop level by accounting for volatility (risk),

the variance in volatility (the change in volatility from bar to bar), and volatility skew

(the propensity for volatility to occasionally spike incorrectly).

Kase Dev Stops are set at points at which there is an increasing probability of reversal against

the trend being statistically significant based on the log normal shape of the range curve.

Setting stops will help you take as much risk as necessary to stay in a good position, but not more.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & CMOfilt This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots a CMO which ignores price changes which are less

than a threshold value. CMO was developed by Tushar Chande. A scientist,

an inventor, and a respected trading system developer, Mr. Chande developed

the CMO to capture what he calls "pure momentum". For more definitive

information on the CMO and other indicators we recommend the book The New

Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change, etc.

It is most closely related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to the

CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & CMOav This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots average of three different length CMO's. This indicator

was developed by Tushar Chande. A scientist, an inventor, and a respected

trading system developer, Mr. Chande developed the CMO to capture what he

calls "pure momentum". For more definitive information on the CMO and other

indicators we recommend the book The New Technical Trader by Tushar Chande

and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change, etc.

It is most closely related to Welles Wilder?s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to

the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & CMOabsThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots the absolute value of CMO. CMO was developed by Tushar

Chande. A scientist, an inventor, and a respected trading system developer,

Mr. Chande developed the CMO to capture what he calls "pure momentum". For

more definitive information on the CMO and other indicators we recommend the

book The New Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented indicators

such as Relative Strength Index, Stochastic, Rate-of-Change, etc. It is most closely

related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to

the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

DAKELAX-XRPUSDT Bollinger Band Strategy for TradebotlerDAKELAX-XRPUSDT is a Tradebotler strategy designed to run on XRPUSDT for binance, it's a simple reverse to mean strategy and when backtested on may-aug 2019 on H1 timeframe it performs pretty well in backtest as well as running live.

In order to get started install the Tradebotler extension and connect the strategy with Binance or other crypto exchanges of your choice such as Kraken, Bitstamp, Bitmex, Bittrex, Polyneux etc, etc.

Combo Backtest 123 Reversal & CMO & WMA This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots Chande Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.