Channels Strategy [JoseMetal]============

ENGLISH

============

- Description:

This strategy is based on Bollinger Bands / Keltner Channel price "rebounds" (the idea of price bouncing from one band to another).

The strategy has several customizable options, which allows you to refine the strategy for your asset and timeframe.

You can customize settings for ALL indicators, Bollinger Bands (period and standard deviation), Keltner Channel (period and ATR multiplier) and ATR (period).

- AVAILABLE INDICATORS:

You can pick Bollinger Bands or Keltner Channels for the strategy, the chosen indicator will be plotted as well.

- CUSTOM CONDITIONS TO ENTER A POSITION:

1. Price breaks the band (low below lower band for LONG or high above higher band for SHORT).

2. Same as 1 but THEN (next candle) price closes INSIDE the bands.

3. Price breaks the band AND CLOSES OUT of the band (lower band for LONG and higher band for SHORT).

4. Same as 3 but THEN (next candle) price closes INSIDE the bands.

- STOP LOSS OPTIONS:

1. Previous wick (low of previous candle if LONG and high or previous candle if SHORT).

2. Extended band, you can customize settings for a second indicator with larger values to use it as STOP LOSS, for example, Bollinger Bands with 2 standard deviations to open positions and 3 for STOP LOSS.

3. ATR: you can pick average true ratio from a source (like closing price) with a multiplier to calculate STOP LOSS.

- TAKE PROFIT OPTIONS:

1. Opposite band (top band for LONGs, bottom band for SHORTs).

2. Moving average: Bollinger Bands simple moving average or Keltner Channel exponential moving average .

3. ATR: you can pick average true ratio from a source (like closing price) with a multiplier to calculate TAKE PROFIT.

- OTHER OPTIONS:

You can pick to trade only LONGs, only SHORTs, both or none (just indicator).

You can enable DYNAMIC TAKE PROFIT, which updates TAKE PROFIT on each candle, for example, if you pick "opposite band" as TAKE PROFIT, it'll update the TAKE PROFIT based on that, on every single new candle.

- Visual:

Bands shown will depend on the chosen indicator and it's settings.

ATR is only printed if used as STOP LOSS and/or TAKE PROFIT.

- Recommendations:

Recommended on DAILY timeframe , it works better with Keltner Channels rather than Bollinger Bands .

- Customization:

As you can see, almost everything is customizable, for colors and plotting styles check the "Style" tab.

Enjoy!

============

ESPAÑOL

============

- Descripción:

Esta estrategia se basa en los "rebotes" de precios en las Bandas de Bollinger / Canal de Keltner (la idea de que el precio rebote de una banda a otra).

La estrategia tiene varias opciones personalizables, lo que le permite refinar la estrategia para su activo y temporalidad favoritas.

Puedes personalizar la configuración de TODOS los indicadores, Bandas de Bollinger (periodo y desviación estándar), Canal de Keltner (periodo y multiplicador ATR) y ATR (periodo).

- INDICADORES DISPONIBLES:

Puedes elegir las Bandas de Bollinger o los Canales de Keltner para la estrategia, el indicador elegido será mostrado en pantalla.

- CONDICIONES PERSONALIZADAS PARA ENTRAR EN UNA POSICIÓN:

1. El precio rompe la banda (mínimo por debajo de la banda inferior para LONG o máximo por encima de la banda superior para SHORT).

2. Lo mismo que en el punto 1 pero ADEMÁS (en la siguiente vela) el precio cierra DENTRO de las bandas.

3. El precio rompe la banda Y CIERRA FUERA de la banda (banda inferior para LONG y banda superior para SHORT).

4. Igual que el 3 pero ADEMÁS (siguiente vela) el precio cierra DENTRO de las bandas.

- OPCIONES DE STOP LOSS:

1. Mecha anterior (mínimo de la vela anterior si es LONGy máximo de la vela anterior si es SHORT).

2. Banda extendida, puedes personalizar la configuración de un segundo indicador con valores más extensos para utilizarlo como STOP LOSS, por ejemplo, Bandas de Bollinger con 2 desviaciones estándar para abrir posiciones y 3 para STOP LOSS.

3. ATR: puedes elegir el average true ratio de una fuente (como el precio de cierre) con un multiplicador para calcular el STOP LOSS.

- OPCIONES DE TAKE PROFIT:

1. Banda opuesta (banda superior para LONGs, banda inferior para SHORTs).

2. Media móvil: media móvil simple de las Bandas de Bollinger o media móvil exponencial del Canal de Keltner .

3. ATR: se puede escoger el average true ratio de una fuente (como el precio de cierre) con un multiplicador para calcular el TAKE PROFIT.

- OTRAS OPCIONES:

Puedes elegir operar sólo con LONGs, sólo con SHORTs, ambos o ninguno (sólo el indicador).

Puedes activar el TAKE PROFIT DINÁMICO, que actualiza el TAKE PROFIT en cada vela, por ejemplo, si eliges "banda opuesta" como TAKE PROFIT, actualizará el TAKE PROFIT basado en eso, en cada nueva vela.

- Visual:

Las bandas mostradas dependerán del indicador elegido y de su configuración.

El ATR sólo se muestra si se utiliza como STOP LOSS y/o TAKE PROFIT.

- Recomendaciones:

Recomendada para temporalidad de DIARIO, funciona mejor con los Canales de Keltner que con las Bandas de Bollinger .

- Personalización:

Como puedes ver, casi todo es personalizable, para los colores y estilos de dibujo comprueba la pestaña "Estilo".

¡Que lo disfrutes!

Bands and Channels

SPX Fair Value Bands V2An updated version of the SPX Fair Value Bands script from dharmatech and based on the net liquidity concept by MaxJAnderson .

Now with full customization of parameters through the settings (Dialog Box) and allowing the options to the use of

1) Standard Bands based on Offsets of the Fair Value

2) Bollinger Bands

3) Keltner Channels

to better capture buy/sell areas rather than relying on noisy unreliably (and unevenly) updated data from the Treasury/Fed.

==================================

Net Liquidity's importance in the new post-COVID QE to QT regime as described MaxJAnderson

----------------

" In past cycles, size of Fed's balance sheet changed a lot, while TGA and RRP changed relatively little. So size of balance sheet roughly equated Net Liquidity.

(The Treasury General Account) TGA and (Reverse Repo) RRP didn't matter. They were rounding errors by comparison.

But starting in 2020, relative changes in TGA and RRP have been THREE TIMES LARGER than the change in size of the Fed's balance sheet. As result, changes in TGA and RRP have taken over as the primary drivers Net Liquidity.

This is new, and changes the game significantly. Again - the size of the Fed's balance sheet doesn't matter.

What matters is the portion of it that's available to circulate in the economy (Net Liquidity).

And ever since 2020, the Treasury and Reverse Repo have become what controls that. Not the size of Fed's balance sheet.

----------------

The idea that follows is simple,short when $SPX reaches extreme levels of overvaluation, and close out when SPX returns to being undervalued. Here's the formulas I currently use to determine fair value:

Fair Value = (Fed Bal Sheet - TGA - RRP)/1.1 - 1625

And here's the trading rules I currently follow:

Short when diff of $SPX - Fair Value > 350

Close when diff of $SPX - Fair Value < 150

When one of these rules is triggered upon market close on a given day, trades are entered at open of the following day "

Keltner Channel Volatility FilterOVERVIEW

The Keltner Channel Volatility Filter indicator is a technical indicator that gauges the amount of volatility currently present in the market. The purpose of this indicator is to filter out with-trend signals during ranging/non-trending/consolidating conditions.

CONCEPTS

This indicator assists traders in capitalizing on the assumption that trends are more likely to start during periods of high volatility compared to periods of low volatility . This is because high volatility indicates that there are bigger players currently in the market, which is necessary to begin a sustained trending move.

So, to determine whether the current volatility in the market is low, the KCVF will grey out all bars whose average price is within the Keltner Channels.

If the average price breaks out of the Keltner Channels , it is reasonable to assume we are in a high-volatility period. Thus, this is the ideal time to enter a trending trade due to the assumption that trends are more likely to start during these high-volatility periods.

HOW DO I READ THIS INDICATOR

When the candles are greyed out, don't take any trend trades since the current volatility is less than the usual volatility experienced in the market.

When the candles aren't greyed out, take all valid with-trend trades since the current volatility is greater than the usual volatility experienced in the market.

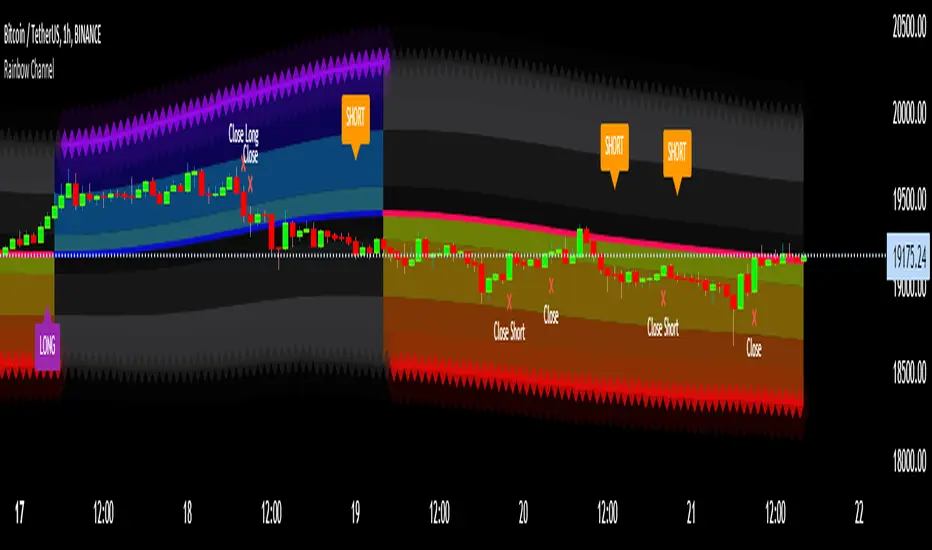

Rainbow ChannelI have designed this indicator with the idea of staying focused on the price during the corresponding trend, for this I have built a rainbow channel

The upper part of the channel is painted in colors during the uptrend, at this time the lower part turns gray to focus only on the longs signals

The lower part of the channel is painted in colors during the downtrend, at this time the upper part turns gray to focus only on the shorts signals

The signals are followed by a mark that indicates when to close that trade.

The indicator works with all timeframes, I use it on the 1 hour chart and I do the trades in 1 minute.

CREDITS:

- @DonovanWall for his study "Gaussian Channel " included in this script

- @Alex Orekhov (everget) for his study "HalfTrend" included in this script

HL-AverageThis script extracts the highest price "ta.highest" and lowest price "ta.lowest" over a period of time, obtains the average value "array.avg" and plots it on a chart. At the same time, it also plots high and low prices, so you can use the volatility over a period of time and its center point as a reference for trading. The pine code is as simple as possible, so there is no difficulty. You can also change the period. We sincerely hope that this script will help you in your trading.

Asymmetric Dispersion High Lowdear fellows,

this indicator is an effort to determine the range where the prices are likely to fall within in the current candle.

how it is calculated

1. obtain

a. gain from the open to the high

b. loss from the open to the low

in the last 20 (by default) candles and

in the last 200 (10*20 by default) candles

2. perform

a. the geometric average (sma of the log returns) over these gains and losses

b. their respective standard deviation

3. plot from the open of each candle

a. the average + 2 standard deviations (2 by default) of the short window size

b. same for the long window size (which is overlapped)

what it shows

1. where the current candle is likely to move with 95% likelyhood

how it can be interpreted

1. a gauge for volatility in the short and long term

2. a visual inbalance between likelyhood to go up or down according to dispersion in relation to current prices or candle open.

3. a confirmation of crossings of, for instance, support and resistances once the cloud is completely above or below.

in regard to bollinger bands (which are and excellent well proven indicator)

1. it segregates upward moves from the downward ones.

2. it is hardly crossed by prices

3. it is centered on the current candle open, instead of the moving average.

we welcome feedback and critic.

best regards and success wishes.

[Sniper] SSL Hybrid + QQE MOD + Waddah Attar StrategyHi. I’m DuDu95.

**********************************************************************************

This is the script for the series called "Sniper".

*** What is "Sniper" Series? ***

"Sniper" series is the project that I’m going to start.

In "Sniper" Series, I’m going to "snipe and shoot" the youtuber’s strategy: to find out whether the youtuber’s video about strategy is "true or false".

Specifically, I’m going to do the things below.

1. Implement "Youtuber’s strategy" into pinescript code.

2. Then I will "backtest" and prove whether "the strategy really works" in the specific ticker (e.g. BTCUSDT) for the specific timeframe (e.g. 5m).

3. Based on the backtest result, I will rate and judge whether the youtube video is "true" or "false", and then rate the validity, reliability, robustness, of the strategy. (like a lie detector)

*** What is the purpose of this series? ***

1. To notify whether the strategy really works for the people who watched the youtube video.

2. To find and build my own scalping / day trading strategy that really works.

**********************************************************************************

*** Strategy Description ***

This strategy is from "SSL QQE MOD 5MIN SCALPING STRATEGY" by youtuber "Daily Investments".

"Daily Investments" claimed that this strategy will make you some money from 100 trades in any ticker in 5 minute timeframe.

### Entry Logic

1. Long Entry Logic

- close > SSL Hybrid Baseline.

- QQE MOD should turn into blue color.

- Waddah Attar Explosion indicator must be green.

2. Short Entry Logic

- close < SSL Hybrid Baseline

- QQE MOD should turn into red color.

- Waddah Attar Explosion indicator must be red.

### Exit Logic

1. Long Exit Logic

- When QQE MOD turn into red color.

2. Short Entry Logic

- When QQE MOD turn into blue color.

### StopLoss

1. Can Choose Stop Loss Type: Percent, ATR, Previous Low / High.

2. Can Chosse inputs of each Stop Loss Type.

### Take Profit

1. Can set Risk Reward Ratio for Take Profit.

- To simplify backtest, I erased all other options except RR Ratio.

- You can add Take Profit Logic by adding options in the code.

2. Can set Take Profit Quantity.

### Risk Manangement

1. Can choose whether to use Risk Manangement Logic.

- This controls the Quantity of the Entry.

- e.g. If you want to take 3% risk per trade and stop loss price is 6% below the long entry price,

then 50% of your equity will be used for trade.

2. Can choose How much risk you would take per trade.

### Plot

1. Added Labels to check the data of entry / exit positions.

2. Changed and Added color different from the original one. (green: #02732A, red: #D92332, yellow: #F2E313)

3. SSL Hybrid Baseline is by default drawn on the chart.

4. If you check EMA filter, EMA would be drawn on the chart.

5. Should add QQE MOD and Waddah Attar Explosion indicator manually if you want to see QQE MOD.

**********************************************************************************

*** Rating: True or False?

### Rating:

→ 1.5 / 5 (0 = Trash, 1 = Bad, 2 = Not Good, 3 = Good, 4 = Great, 5 = Excellent)

### True or False?

→ False

→ Doesn't Work on 5 minute timeframe. Also, it doesn't work on crypto.

### Better Option?

→ Use this for Day trading or Swing Trading, not for Scalping. (Bigger Timeframe)

→ Although the result was bad at 5 minute timeframe, it was profitable in 1h, 2h, 4h, 8h, 1d timeframe.

→ BTC, ETH was ok.

→ The result was better when I use EMA filter (only on longer timeframe).

### Robust?

→ So So. Although result was bad in short timeframe (e.g. 30m 15m 5m), backtest result was "consistently" profitable on longer timeframe.

→ Also, MDD was not that bad under risk management option on.

**********************************************************************************

*** Conclusion?

→ Don't use this on short timeframe.

→ Better use on longer timeframe with filter, stoploss and risk management.

Three Linear Regression ChannelsPlot three linear regression channels using alexgrover 's Computing The Linear Regression Using The WMA And SMA indicator for the linear regression calculations.

Settings

Length : Number of inputs to be used

Source : Source input of the indicator

Midline Colour : The colour of the midline

Channel One, Two, and Three Multiplicative Factor : Multiplication factor for the RMSE, determine the distance between the upper and lower level

Channel One, Two, and Three Colour : The channel's lines colour

Usage

For usage details, please refer to alexgrover 's Computing The Linear Regression Using The WMA And SMA indicator.

Nadaraya-Watson non repainting [LPWN]// ENGLISH

The problem of the wonderfuls Nadaraya-Watson indicators is that they repainting, @jdehorty made an aproximation of the Nadaraya-Watson Estimator using raational Quadratic Kernel so i used this indicator as inspiration i just added the Upper and lower band using ATR with this we get an aproximation of Nadaraya-Watson Envelope without repainting

Settings:

Bandwidth. This is the number of bars that the indicator will use as a lookback window.

Relative Weighting Parameter. The alpha parameter for the Rational Quadratic Kernel function. This is a hyperparameter that controls the smoothness of the curve. A lower value of alpha will result in a smoother, more stretched-out curve, while a lower value will result in a more wiggly curve with a tighter fit to the data. As this parameter approaches 0, the longer time frames will exert more influence on the estimation, and as it approaches infinity, the curve will become identical to the one produced by the Gaussian Kernel.

Color Smoothing. Toggles the mechanism for coloring the estimation plot between rate of change and cross over modes.

ATR Period. Period to calculate the ATR (upper and lower bands)

Multiplier. Separation of the bands

// SPANISH

El problema de los maravillosos indicadores de Nadaraya-Watson es que repintan, @jdehorty hizo una aproximación delNadaraya-Watson Estimator usando un Kernel cuadrático racional, así que usé este indicador como inspiración y solo agregamos la banda superior e inferior usando ATR con esto obtenemos una aproximación de Nadaraya-Watson Envelope sin volver a pintar

Configuración:

Banda ancha. Este es el número de barras que el indicador utilizará como ventana retrospectiva.

Parámetro de ponderación relativa. El parámetro alfa para la función Rational Quadratic Kernel. Este es un hiperparámetro que controla la suavidad de la curva. Un valor más bajo de alfa dará como resultado una curva más suave y estirada, mientras que un valor más bajo dará como resultado una curva más ondulada con un ajuste más ajustado a los datos. A medida que este parámetro se acerque a 0, los marcos de tiempo más largos ejercerán más influencia en la estimación y, a medida que se acerque al infinito, la curva será idéntica a la que produce el Gaussian Kernel.

Suavizado de color. Alterna el mecanismo para colorear el gráfico de estimación entre la tasa de cambio y los modos cruzados.

Período ATR. Periodo para calcular el ATR (bandas superior e inferior)

Multiplicador. Separación de las bandas

Trend #4 - ATR+EMA channelOverview:

This strategy use ATR to take-profit, Red-EMA to stop-loss, Blue-EMA channel to judgment breakout.

This strategy use commission setting is 0.05%, slippage setting is 2 ticks, you can set the appropriate value size in the properties page.

What it does:

This strategy detects when a trend is emerging and buy or sell.

How it does it:

When the price breaks through the blue EMA channel, the trend is judged to be strong in the short term, strategy generates a buy or sell order.

After buying or selling,, if the price moves in the expected direction, uses ATR to determine the appropriate spread to take profit, otherwise use red EMA for stop loss.

How to use it:

Start Date and Stop Date - This parameter adjusts the time range used by the strategy.

Stoploss - This parameter adjusts the stop loss amount after each order is placed.

Blue EMA length - This parameter adjusts the length of the channel.

Blue EMA multy - This parameter adjusts the width of the top and bottom of the channel.

ATR Period - This parameter adjusts the number of candles used by the ATR.

ATR mult - This parameter adjusts the upper and lower widths of the ATR. Lowering this parameter can improve the win rate, but not necessarily the profitability.

Red EMA length - This parameter adjusts the number of candles used by the red EMA .

Long - This switch is used to turn Long position on or off.

Short - This switch is used to turn short position on or off.

Expected SPX Movement by timeframeTHIS INDICATOR ONLY WORKS FOR SP:SPX CHART

This code will help you to measure the expected movement of SP:SPX in a previously selected timeframe based on the current value of VIX index

E.g. if the current value of VIX is 30 we calculate first the expected move of the next 12 months.

If you selected the Daily timeframe it will calculate the expected move of SPX in the next Day by dividing the current VIX Value by the squared root of 252

(The 252 value corresponds to the approximate amount of trading sessions of the year)

If you selected the Weekly timeframe it will calculate the expected move of SPX in the next Week by dividing the current VIX Value by the squared root of 52

(The 52 value corresponds to the amount of weeks of the year)

If you selected the Monthly timeframe it will calculate the expected move of SPX in the next Week by dividing the current VIX Value by the squared root of 12

(The 12 value corresponds to the amount of months of the year)

For lower timeframes you have to calculate the amount of ticks in each trading session of the year in order to get that specific range

Once you have that calculation it it'll provide the range expressed as percentage of the expected move for the following period.

This script will plot that information in a range of 2 lines which represents the expected move of the SPX for the next period

The red flag indicator tells if that period closed between the 2 previous values marked by the range

Attrition Scalper v2.0Green/Red Arrowed Buy/Sell signals are just simple buy sell signals based on SuperTrend, VWAP, Bollinger, Linear Regression

Purple Arrowed Buy/Sell Signals happen when the price/candle cross over or under the yellow outer lines (4.236 fib lines) It's extremely rare and hard for price to stay above these lines therefore we can usually and comfortably buy/sell it, a key information here though when price pumps or dumps super fast and hard to the point of crossing these borders, the trend might also be extremely strong and continous so even if the price temporarily goes back inside the borders as the lines expand over time price can continue riding or crossing these lines back again and continue the uptrend/downtrend, therefore crossing these outer borders doesn't necessarilly and always mean a reversal is due.

When analyzing the instrument you're trading the important factors for support/resistance areas are usually the outer lines like i said previously it's super hard for price to be outside these and will almost always get back inside quickly. The Middle thicker green/red line which is Variable Index Dynamic Average should also be a nice pivot line for major support and resistance . All the other lines are also important dynamic support/resistance lines.

Their Importance Order

1- Outer Yellow Line (4.236 Fibs)

2- Thicker Middle Green/Red Line (VIDYA)

3- Thinner Upper/Lower Green/Red Line (VIDYA +3, VIDYA -3)

4- The Rest Of The Lines (Fib Lines)

You can use this indicator in any market condition in any market to determine key support/resistance levels, use it for mean reversion through price expanding to outside of the most outer line therefore being overbought/oversold basically using the purple buy/sell signals or only follow the normal buy/sell signals or use it in confluence with each other. You can also use this indicator in confluence with your own manual technical analysis or other indicators/strategies you are already using and are comfortable with.

A good part is the support/resistance lines from timeframe to timeframe pictures the whole situation quite well, you can use lower timeframe to find your entry/exit positions and higher timeframe to find your key support/resistance points, they all should be somewhat in confluence from timeframe to timeframe anyways. My recommendation would be to look at 1HR, 4HR and 1D charts for swing trading and 5-15 Min for quick scalping/day trading

You should still probably at least take a look to higher timeframes so that you don't get burned when you realize there is a huge resistance line at price XXXXX on the 4 hour chart but you're expecting it to go above it on the 5 minute chart, it can go above it temporarily but we analyze everything on a closing basis so it most likely won't close above it. Again don't take a position or FOMO when price breaks a support/resistance line, we're looking for a CLOSE above/below them and a retest to see if S/R flip happened would even be better.

Sometimes the most outer line won't be the 4.236 (Yellow) lines as when it gets quite volatile the Thinner Upper/Lower Green/Red Lines (VIDYA +3, VIDYA-3) might cross them to be the most outer line, in this case i have observed that the trend is extremely strong this time price almost always doesn't go above or below the VIDYA line but can stay outside of the Yellow 4.236 Fib line for an extended amount of time (price will still get back inside the channel relatively quickly, just not as fast as the normal condition)

With Proper Risk Management and Discipline this indicator can be of great use to you as it's surprisingly successful especially at mean reversion and pointing out the support/resistance lines, they are so much more successful than your average MA/EMA lines.

Multi-Optimized Linear Regression ChannelA take on alexgrover 's Optimized Linear Regression Channel script which allows users to apply multiple linear regression channel with unique multiplicative factors.

Multiplicative Factors

Adjust the amount of channels and multiplicative factors of existing or additional channels using the "Mults" input.

An input of "1" creates a single linear regression channel with the multiplicative factor of one.

An input of "4" creates a single linear regression channel with the multiplicative factor of four.

An input of "1,4" creates two linear regression channels with multiplicative factors of one and four.

An input of "1,2,3" creates three linear regression channels with multiplicative factors of one, two, and three.

SQueezeVergenceThis is my SQueezeVergence indicator. It fires Buy and Sell signals based on squeeze momentum and trend. **It also creates Bull and Bear signals based on MACD divergence which should only be used as areas of support and resistance being as these signals repaint based on a 5 candle look back of pivots.** All settings are editable for better use. The default settings are what I use on the 1 Minute chart of ES to scalp. This is a simple indicator to help me get alerts on when I need to scalp. The divergence signals work well for areas of significance. I like to watch for breaks of these levels along with support and resistance. I hope this helps.

DB Change Forecast ProDB Change Forecast Pro

What does the indicator do?

The DB Change Forecast Pro is a unique indicator that uses price change on HLC3 to detect buy and sell periods along with plotting a linear regression price channel with oversold and undersold zones. It also has a linear regression change forecast mode to optionally project market direction.

Change is calculated by taking a two-bar change of HLC3 and dividing that by the price or, optionally, a fixed divisor.

A fast-moving change cloud is then calculated and displayed as the "regular version" plot (shown in light gray). When the cloud bottom is above low, a buy zone is detected. When the cloud top is below the high, a sell zone is detected.

The linear regression price channel is calculated similarly but using a much slower change rate. The linear regression price channel shows reasonable high, low and HLC3 ranges. At the bar's opening, the channel will be more compact and come fairly accurate about 1/4 into the bar timeframe.

The change forecasted price is projected on the right side of the current bar to indicate the current timeframe direction. Please note this forecasting feature is shown in orange when it's early in the timeframe and gray when the timeframe is more likely to produce an accurate direction forecast for the upcoming bar.

You can use these projected dashed lines to see possible market movements for the Current bar and possible market direction for the next bar. Kindly note these projects change; they should be used to understand possible extreme highs/lows for the current bar or market direction.

The indicator includes an optional change forecast projection feature hidden by default. It will project the market forecast channel with an offset of 1. The forecast is defaulted to an offset of 1 to show market direction. However, you can modify to zero the offset to show the current bar forecast and forecast history.

How should this indicator be used?

First, very important,

1. Settings > Set Symbol to Desired

2. Settings > Set High Timeframe to "Chart"

3. Settings > Ensure "Use price as divisor" is checked.

It's recommended to use this indicator in higher timeframes. Buy and sell signals are displayed in real-time. However, waiting until 1/4 to 1/2 into the current bar is recommended before taking action, and change can happen.

The buy/sell signals (zones) provide recommendations on playing a long vs. a short. When in a buy sone, only play longs. When in a sell zone, only play shorts.

Then use the linear regression price channel oversold and undersold zones to optionally open and close positions within the buy/sell zones.

For example, consider opening a long in a buy zone when the linear regression price channel shows undersold. Then consider closing the long when the price moves into the linear regression oversold or higher. Then repeat as long as it's in the buy zone. Then vice versa for sell zones and shorting.

At basic design, buy in the buy zone, sell or short in the sell zone. If you are up for higher trading frequencies, use the linear regression price channel as described in the example above.

Please note, as, with all indicators, you may need to adjust to fit the indicator to your symbol and desired timeframe.

This is only an example of use. Please use this indicator as your own risk and after doing your due diligence.

Does the indicator include any alerts?

Yes,

"DB CFHLC3: Signal BUY" - Is triggered when a buy signal is fired.

"DB CFHLC3: Signal SELL" - Is triggered when a sell signal is fired.

"DB CFHLC3: Zone BUY" - Is triggered when a buy zone is detected.

"DB CFHLC3: Zeon SELL" - Is triggered when a sell zone is detected.

"DB CFHLC3: Oversold SELL" - Is triggered when the price exceeds the oversold level.

"DB CFHLC3: Undersold BUY" - Is triggered when the price goes below the undersold level.

Any other tips?

Once you have configured the indicator for your symbol and chart timeframe. Meaning the plots are displayed over the price. Check out larger timeframes such as W, 2W, 3W, 4W, M, and 4M. It works wonderfully for showing market lows and highs for long-term investing too!

Another, tip is to combine it with your favorite indicator, such as TTM Squeeze or MACD for confirmation purposes. You may be surprised how fast the indicator shows market direction changes on higher timeframes.

You can just as easily use a high timeframe such as D, 2D, or 3D for day trading due to how the linear price channel works.

Why am I not selling this indicator?

I would like to bless the TradingView community, and I enjoy publishing custom indicators.

If you enjoy this indicator, please consider leaving a thumbs up or a comment for others to know about your experience or recommendations.

Enjoy!

HMA w/ SSE-Dynamic EWMA Volatility Bands [Loxx]This indicator is for educational purposes to lay the groundwork for future closed/open source indicators. Some of thee future indicators will employ parameter estimation methods described below, others will require complex solvers such as the Nelder-Mead algorithm on log likelihood estimations to derive optimal parameter values for omega, gamma, alpha, and beta for GARCH(1,1) MLE and other volatility metrics. For our purposes here, we estimate the rolling lambda (λ) value used to calculate EWMA by minimizing of the sum of the squared errors minus the long-run variance--a rolling window of the one year mean of squared log-returns. In practice, practitioners will use a λ equal to a standardized value put out by institutions such as JP Morgan. Even simpler than this, others use a ratio of (per - 1) / (per + 1) to derive λ where per is the lookback period for EWMA. Due to computation limits in Pine, we'll likely not see a true GARCH(1,1) MLE on Pine for quite some time, but future closed source indicators will contain some very interesting industry hacks to get close by employing modifications to EWMA. Enjoy!

Exponentially weighted volatility and its relationship to GARCH(1,1)

Exponentially weighted volatility--also called exponentially weighted moving average volatility (EWMA)--puts more weight on more recent observations. EWMA is calculated as follows:

σ*2 = λσ(n - 1)^2 + (1 − λ)u(n - 1)^2

The estimate, σn, of the volatility for day n (made at the end of day n − 1) is calculated from σn −1 (the estimate that was made at the end of day n − 2 of the volatility for day n − 1) and u^n−1 (the most recent daily percentage change).

The EWMA approach has the attractive feature that the data storage requirements are modest. At any given time, we need to remember only the current estimate of the variance rate and the most recent observation on the value of the market variable. When we get a new observation on the value of the market variable, we calculate a new daily percentage change to update our estimate of the variance rate. The old estimate of the variance rate and the old value of the market variable can then be discarded.

The EWMA approach is designed to track changes in the volatility. Suppose there is a big move in the market variable on day n − 1 so that u2n−1 is large. This causes our estimate of the current volatility to move upward. The value of λ governs how responsive the estimate of the daily volatility is to the most recent daily percentage change. A low value of λ leads to a great deal of weight being given to the u(n−1)^2 when σn is calculated. In this case, the estimates produced for the volatility on successive days are themselves highly volatile. A high value of λ (i.e., a value close to 1.0) produces estimates of the daily volatility that respond relatively slowly to new information provided by the daily percentage change.

The RiskMetrics database, which was originally created by JPMorgan and made publicly available in 1994, used the EWMA model with λ = 0.94 for updating daily volatility estimates. The company found that, across a range of different market variables, this value of λ gives forecasts of the variance rate that come closest to the realized variance rate. In 2006, RiskMetrics switched to using a long memory model. This is a model where the weights assigned to the u(n -i)^2 as i increases decline less fast than in EWMA.

GARCH(1,1) Model

The EWMA model is a particular case of GARCH(1,1) where γ = 0, α = 1 − λ, and β = λ. The “(1,1)” in GARCH(1,1) indicates that σ^2 is based on the most recent observation of u^2 and the most recent estimate of the variance rate. The more general GARCH(p, q) model calculates σ^2 from the most recent p observations on u2 and the most recent q estimates of the variance rate.7 GARCH(1,1) is by far the most popular of the GARCH models. Setting ω = γVL, the GARCH(1,1) model can also be written:

σ(n)^2 = ω + αu(n-1)^2 + βσ(n-1)^2

What this indicator does

Calculate log returns log(close/close(1))

Calculates Lambda (λ) dynamically by minimizing the sum of squared errors. I've restricted this to the daily timeframe so as to not bloat the code with additional logic required to derive an annualized EWMA historical volatility metric.

After the Lambda is derived, EWMA is calculated one last time and the result is the daily volatility

This daily volatility is multiplied by the source and the multiplier +/- the HMA to create the volatility bands

Finally, daily volatility is multiplied by the square-root of days per year to derive annualized volatility. Years are trading days for the asset, for most everything but crypto, its 252, for crypto is 365.

Converging Pullbacks and PeaksMulti Timeframe Converging Lines Indicator. Using the highest/lowest Values at 2 different lengths. Convergence created by taking the highest/lowest value and subtracting/adding the # of barssince the highest/lowest bar was set multiplied by the price multiplied by the float. Curves are created from averaging out the emas of the center lines of the extremeties.

Helps show trendlines automatically most of the time but can be tweaked by changing the floats or Fast/Slow lengths to you liking.

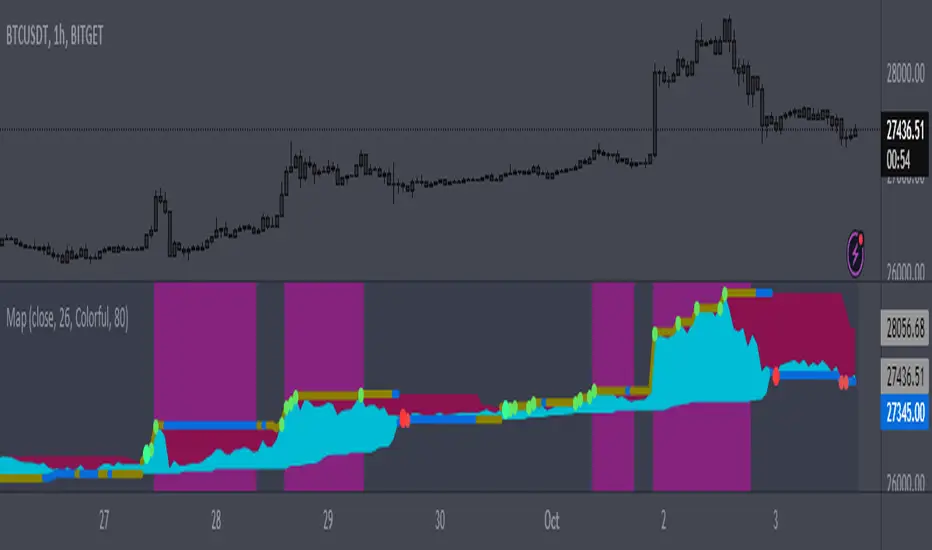

MapMap - an indicator that shows the highest and lowest points on the price movement road.

The calculation is based on the type of price data specified in the "Source" parameter and the length of the time interval specified in the "Length" parameter.

The indicator helps to visually find a local trend and rebound points.

Thanks for your attention!

Thursday Close BandsThis script is useful for Indian Markets where weekly expiry is on Thursday.

As per last 10 years historical stats Nifty stays with in 3% range from Thursday close 80% times.

Adaptive Rebound Line Bands (ARL Bands)These bands consist of 4 ARLs (See: Adaptive Rebound Line ('ARL'/AR Line)) that help accurately spot price rebounds.

It is excellent for 15 minute scalping and price-action trading.

See notes in the picture above for more details.

Note: "Top Deviation" is the deviation of the top 'ARL', "High Deviation" is for the high 'ARL', etc.

RTH & ETH VWAPs [vnhilton]Plots 2 different VWAPs for regular & extended trading sessions, with option for a plot fill between the 2 (using pinescript's new vertical gradient feature).

[DuDu95] SSL 4C MACD Laugerre RSI StrategyHello Guys! Nice to meet you all!

Before I start, my nickname has changed to 'DuDu95'!!

This is the Strategy introduced by youtube channel.

I made this based on the open source indicator by kevinmck100, vkno422, KivancOzbilgic. Thank you All!

### Entry Logic

1. Long Entry Logic

- close > SSL Hybrid baseline upper k (keltner channel)

- macd signal > 0 and current MACD value > previous MACD value

- Laguerre RSI < overbought Line.

2. short Entry Logic

- close < SSL Hybrid baseline lower k (keltner channel)

- macd signal < 0 and current MACD value < previous MACD value

- Laguerre RSI > overbought Line.

### Exit Logic

1. Long Exit Logic

- close < SSL Hybrid baseline lower k (keltner channel)

- macd signal < 0

2. short Entry Logic

- close > SSL Hybrid baseline upper k (keltner channel)

- macd signal > 0

### StopLoss

1. Can Choose Stop Loss Type: Percent, ATR, Previous Low / High.

2. Can Chosse inputs of each Stop Loss Type.

### Take Profit

1. Can set Risk Reward Ratio for Take Profit.

- To simplify backtest, I erased all other options except RR Ratio.

- You can add Take Profit Logic by adding options in the code.

2. Can set Take Profit Quantity.

### Risk Manangement

1. Can choose whether to use Risk Manangement Logic.

- This controls the Quantity of the Entry.

- e.g. If you want to take 3% risk per trade and stop loss price is 6% below the long entry price,

then 50% of your equity will be used for trade.

2. Can choose How much risk you would take per trade.

### Plot

1. Added Labels to check the data of entry / exit positions.

2. Changed and Added color different from the original one. (green: #02732A, red: #D92332, yellow: #F2E313)

[Floride] 4 Layers of Bollinger Shadow

This is the indicator I named 4LBS. That means four layers of bollinger shadow.

This is an indicator that I made to see how far past prices could affect the future prices.

And I found some very interesting and beautiful things about it, and I wanted to share them with you, so I publish this indicator.

*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-

Hello, nice to meet you all. my name as a trader is Floride.

First of all, I am not good at English, so there may be many grammatically incorrect sentences below.

I ask for your understanding in advance. Thanks for your understanding.

*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-*-

What is it?

bollinger Bands usually has one moving average line. And there's two bands that uses same period value of standard deviation as the former MA. And this indicator, by the way, has a 4 shadow bands

that uses twice,three,four,five time the value of the MA's period.

Appearance -

This indicator has four layers, and there are also other layers between them.

You can turn on or off all the shadow layers.

Uses of Indicator and Examples

examples of actual use

1. market strongness diagnosis

-It seems all layers of shadow has some degree resist/support forces.

This indicator has the 4th layer - "L4". (indicated by red lines).

I saw emergence of volatility quite frequently when this last layer breaks through.

When price breaks through this area or line, shade appear on the L4 layer in red. and red cross appear on the that point. This is I called Marlin signal.

If you saw red color shadow in this indicator, then the market may have quite high volatility.

(of course, there's not 100%. Please be careful about this.)

But I've also checked in quite several markets. when this volatility emerges, then also that market seems to started to building quite directional power afterwards.

I mean, after the marlin signal, market tends to have bigger volatility, and tends to go one direction.

again, it's not 100%. but probability is quite high.

But maybe depending on the type of market you need some adjustment.

Recommended values are M2-1.618, M3-2.618

Or M2-1, M3-2. default value is M2-1.618, M3-2.618

and also, if prices breakthrough the channels, or layers, It tends to break through the at once, in first bar. In other words, if price don't break through the first or second candle, it's very likely that the price won't break through channel for the time being.

2. market weakness diagnosis

Usually, without external momentum, the price converges to the average value and does not deviate from the band. And if price fails to break through the most inner first layer-"L1 - the green channel", In that case, the market is usually assumed to be weak, or has low volatility.

- you can set alarms on tuna, marlin signal. and you don't have to watch chart all the time.

3. Signals

I put two signals in this indicator.

One has the name "Tuna," and the second has the name "Marlin."

As you can already tell from the name's feeling, tuna is a weaker signal and marlin is a stronger signal.

Actual example of a signal

1. Tuna signal

- When the tuna signal appears, you can guess that the current market is generally not weak. or has quite good directional force. or medium volatility.

Below is important.

- If a tuna signal appears, there is a possibility that a marlin will appear later.

- In my opinion, it might be wise not to have a position without a tuna signal.

- Almost all of the marlin signal appeared shortly after the tuna signal appeared.

2. Marlin signal

- When marlin signal appears, with a high probability, volatility can increase large.

- In the backtesting of the stock, in some cases, the market moved quite frequently in the direction of the marlin signal.

- The emergence of marlin can be seen as a pretty strong indication of the emergences of direction.