APPLE BULLISH ON THE DAILYAPPLE has broken above the bullish channel formed a bull flag, and has now broken out. We can expect a rise above 200 and possibly as high as 210 provided that the tech sector remains bullish.

Search in ideas for "APPLE"

APPLE New Max HighIf apple beat with decision the 120 level, could touch the $134 level and even make a new high.

Apple is at a resistance levelShort

Apple is at a resistance level

The price usually drops after product launch

limit 82

stop 108

Apple Stock:The 3 Steps Rocket Booster Strategy [Learn More]Apple stock looks like its trending upwards.

Today I was thinking about how to trade

the markets with less risk and if that's even possible.

-

Do you think you can trade the markets without risk?

What is your risk management strategy?

-

As traders we are all different that's why

its not easy to teach risk management, and profit-taking

because its a personality thing

-

The rocket booster strategy is technical analysis.

It has the following steps according to

this NASDAQ:AAPL stock chart:

-The price has to be above the 50 EMA

-The price has to be above the 200 EMA

-The 50 EMA should cross above the 200 EMA

-

That is the rocket booster strategy

To learn more rocket boost this content.

Disclaimer: Trading is risky, please

learn risk management

and profit-taking strategies.

Apple “disproved ” Newton’s law of Gravity? 1/August/22.Apple. AAPL. The world's biggest companies by market cap. Is he breaking “ Newton’s law of Gravity = stop falling down? Probably not.. Maybe another -35%..@ around 103.80? (F=ma)

Apple... look for a breakout with volumeApple is in a resistance level, tested multiple times. Look for a breakout with volume.

Target price: 142

Expected Returns: 12%

APPLE 270 - 300 - 320 TP BY 2025 Apple's potential to reach a stock price of $320 by 2025 is significantly bolstered by its strategic shift towards artificial intelligence (AI). Here are key reasons why this could happen:

AI-Driven iPhone Upgrades: Apple is poised to enter what analysts describe as a "multi-year AI-driven iPhone upgrade cycle." This cycle is expected to drive significant hardware sales as consumers upgrade to newer models equipped with advanced AI capabilities. The introduction of Apple Intelligence, a suite of AI features, is anticipated to make the iPhone more compelling, encouraging upgrades even from users with relatively new devices.📷📷📷

Expansion in Services Revenue: With AI, Apple aims not just at hardware but also at enhancing its services ecosystem. Features like Apple Intelligence are expected to spawn new AI-driven apps and services, creating new revenue streams. This could lead to a multi-billion-dollar increase in services revenue, which traditionally accounts for a substantial portion of Apple's income.📷

Market Sentiment and Analyst Predictions: Recent analyst upgrades reflect a strong bullish sentiment on Apple's stock due to its AI strategy. For instance, Wedbush has raised the price target to $325, suggesting Wall Street might be underestimating Apple's growth potential in the

AI space. This optimism could drive investor confidence and stock value upwards.📷📷📷

Innovation and Market Positioning: Apple's focus on on-device AI, privacy, and security differentiates it from competitors. By integrating AI into its core products like Siri, Photos, and even the new iPhone SE expected in 2025, Apple can maintain or even increase its market share in both developed and emerging markets. This is particularly relevant as AI becomes more integral to everyday device usage.📷📷

Regulatory Adaptation: Despite facing regulatory challenges, Apple's ability to adapt and navigate these issues while continuing to innovate in AI could further solidify its market position. Compliance with new laws while maintaining innovation could be seen as a testament to Apple's strategic foresight, potentially boosting investor confidence.

Apple AAPL - Brace Yourselves for $200. Seriously.Apple is something of a reverse canary in the coalmine when it comes to the Nasdaq, specifically because it's its highest weighted company at almost 14%. All these weeks everyone has been bearish, but yet, Apple is not in anything resembling a bear market.

Instead, everything about Apple from the monthly chart to the daily chart indicates that the January all time high of $182.93 is not very likely at all to be the all time high.

And this is under the circumstance wherein Apple extensively relies on what is effectively slave labor supplied by the notorious Chinese Communist Party, a problem really exacerbated by the regime employing that Zero-COVID stuff.

This is important because the situation with Apple's Foxconn factories and other Chinese factories and the new restrictions on chip makers means there is fundamental problems with this company going forward.

There's fundamental problems and yet it's set up to rally to a new all time high. Apple is more or less in "The Big Short."

Look up "China Quarantine Camps" or "COVID QR Code" on social media. The Chinese are literally being placed by the millions into huge concentration camps and every aspect of their daily life, from their ability to use public transit, their ability to go to work, their ability to purchase goods, their ability to use money, is entirely under the CCP's social credit system, lynch pinned around the colour of their QR code health pass.

And to think this is a system that the Western globalist establishment would like to install for all of us all over the world via central bank digital currencies... all I can say to readers is I hope you are intelligent enough to reject the Communist Party's things and its Marxist-Leninist "Theory of Evolution" and atheism stuff. If you want those things, you'll have to go with those things and experience what those things truly entail.

Personally, I'm calling a bear market rally, with Nasdaq going to 14,000. I suppose it'll be rather humiliating for me if this turns out to be incorrect and we keep dumping. However, fortune favours the bold, and at the same time, this is how bear markets work and there's a logic to the way they operate.

Nasdaq NQ - Unpopular Opinion #2,118: 14,000 is Coming

I also believe that stocks like Amazon and Meta are due for a fat rally

AMZN Amazon - Realistic Expectations In Both Doom and Gloom

Facebook/Meta - Too Much Bear, Not Enough Bull

Before you discount my supposition as hogwash, consider that McDonald's and Lockheed Martin just made all time highs just last month. And this is supposed to be a bear market where everything is going down.

So what's the rationale for saying Apple is going to set a new all time high?

Let's examine the monthly:

1. Apple set the low of the year in June, like everything else, but when it came time for September and October's scary index dumps, Apple remained very strong. October was actually a winning month overall.

2. Although this appears to have sharply reversed in November, it's worth noting we're a total of 4 trading days into the month. The November high as printed is not likely to remain the high.

3. In terms of range equilibrium for this market cycle, which I measure from anything's Coronavirus Disease 2019 pseudo-pandemic hysteria low to its all time high, Apple has not wanted to trade back to equilibrium. This all on its own tells me that the MMs are still heavy on the sell.

Looking at a weekly chart:

Inside the 2022 trading range we can see that Apple is currently trading at a deep discount. The magnification of the fractal shows us that not only is the prior statement true, but that the area below the October of 2021 pivot that led to the ATH has been worked extensively for the last several months.

On the daily, we can see with more clarity that the post-earnings pump was actually a major trade away from this genuine demand zone and back towards range equilibrium. It has since retraced, which is bullish.

If you understand how sell models work, you'll understand why this is "bullish" and not "bearish," and you'll understand why Apple continues to trade like it does and why it doesn't want to make a new low despite how excited everyone always is about the prospect of it crashing so they can buy cheap.

(Hint: When Apple is under $115, don't touch it. It's going to wind up like Facebook.)

But if you understand how sell models work, you'll also know why a new all time high on Apple is bearish, and not bullish.

What I would like to say to everyone is that bear markets rally and rally hard. They do this for a reason and the fundamental reason is that they're not bullish.

It sounds contradictory, right? "Why would something rally so hard if it's not bullish? How can that be?"

You are confused because when you see price go up, you think buying and when you see price go down, you think selling. Yet, if the banks and the funds traded like that, they would blow their account like you do and we would have ourselves a Lehman Brothers moment every 3 to 6 months and society would collapse.

When you see huge rallies like what's ahead you need to govern yourself strictly, and this means:

1. Don't get delusional and think you're in a new paradigm of everything going uppy. No, SPX is not going to 6,000 before Jan. 1 like David J. Hunter has been calling.

2. Check your greed before your greed checks your hide

3. Don't short or buy puts too early. Instead, buy them too late. A bullish Apple is as scary as a bullish Bitcoin.

4. The more complaining you see on social media and your signal groups about the Federal Reserve and "this ponzi," the higher things are going to go. The top is in when the charlatans and grifters start talking about getting long.

5. Buy the dip, but keep your risk low.

6. Make sure you take profits because this is no time to buy and hold.

Because what lies ahead after you see this go on for a bit and VIX hit numbers like 17 and 18, is this, which I called in August,

VIX - 9x8 = 72

The limit down that lies ahead is going to be vicious. Afterwards, North Americans will finally know what a real bear market feels like. It's not fun.

Apple | Fundamental Analysis | MUST READ | LONG Apple stock, like most other tech companies, has made investors experience a full range of emotions this year. While the company's stock price was volatile in the first few months of 2022, a significant downward trend began after the company reported Q2 results in late April.

The stock has not recovered since then. According to S&P Global Market Intelligence, Apple stock is down 17 percent for the year. That's mostly because investors are concerned that Apple won't be able to avoid the effects of supply chain shortages and a potential economic slowdown.

Investors went into pessimistic mode in late April after Apple released its Q2 financial results. Apple beat analysts' consensus estimates on both the top and bottom line, but investors focused on the company's management comments.

During the results announcement, CEO Tim Cook said Apple was "not immune" to supply chain problems caused by COVID-19, chip shortages, and the war in Ukraine.

Apple Chief Financial Officer Luca Maestri was more specific about the supply chain problems and said they could hurt Apple's third-quarter sales by as much as $8 billion.

"Supply chain constraints caused by COVID-related disruptions and industry-wide silicon shortages are impacting our ability to meet customer demand for our products. We expect these constraints to be between $4 billion and $8 billion, significantly higher than the March quarter," Maestri said.

Clearly, investors didn't want to hear that Apple's sales could suffer to such an extent and sent the company's stock on a downward track.

Apple investors will want to keep a close eye on the Q3 results, which will be released July 28. The results should shed light on how severe Apple's supply chain problems have become and whether the company has felt the downturn in consumer demand.

With inflation still at its highest level in nearly 40 years and the U.S. Federal Reserve focused on raising the federal funds rate to get it back on track, it is likely that Apple investors could experience some more short-term volatility as the market reacts to a potential economic slowdown.

But long-term investors should also consider that while temporary supply constraints may affect the company, Apple still has the potential to be a great investment. For one thing, the company still generates a massive amount of cash -- $28 billion in operating cash flow in the last quarter -- that will help it weather a potential economic slowdown better than other companies.

And while Apple stock isn't that cheap right now -- it's worth 23 times the company's projected earnings -- the recent stock sell-off gives investors the opportunity to buy shares of this extremely profitable company at a relative discount.

Finally, Apple continues to increase shareholder value through buybacks and invest in new products. In the last quarter, the company added $90 billion to its stock buyback program and could enter a new product segment within the next year.

With Apple stock down this year and the company still in a very strong financial position, investors may want to consider buying some stock right now.

Apple | Fundamental Analysis | Bat Pattern Formation|LONG SETUPApple will release its fiscal 2022 Q1 results today after the market closes, and investors are hopeful that the company will show good results to stop the stock's decline.

Apple stock is down in 2022 because of a hawkish stance by the Federal Reserve, which could lead to four interest rate hikes in 2022 to keep inflation under control.

Apple CEO Tim Cook noted during an earnings conference call in October that the company lost about $6 billion in revenue in the fourth quarter of fiscal 2021 because of "industry silicon shortages and COVID-related manufacturing disruptions." Cook added that "the impact of supply constraints will be greater in the December quarter."

Because of supply chain issues, Apple declined to release its first-quarter earnings guidance, so it remains to be seen how the company's results will compare to Wall Street expectations. Analysts expect Apple's fiscal first-quarter revenue to grow just 6% year over year to $118.4 billion. Last year in the same quarter, the company grew revenue 21% to $111.4 billion, and in fiscal 2021, its full-year revenue rose 33% to $365.8 billion.

Higher rates encourage investors to move their money from high-risk companies to relatively safer investments, such as bonds. In addition, higher interest rates increase borrowing costs, which can have a negative impact on the bottom line, something investors don't want to see in high-value stocks.

When you add in the fact that Apple suffered from supply chain problems during the holiday season, the odds seem to be stacked against the iPhone maker when it releases its results. Does this mean that investors should start selling Apple stock before the earnings report is released? Or should they take advantage of the drop and buy more? Let's find out.

The company's earnings are only expected to increase 12% year-over-year this quarter. By comparison, in the fiscal year 2021, Apple's adjusted earnings rose 71% to $5.61 per share.

The bigger concern is that Apple's growth rate could slow significantly this fiscal year. Analysts expect fiscal 2022 revenue to grow just 4.5% to $382.3 billion, and earnings are expected to rise just 2.3% to $5.74 per share. A potential increase in interest rates could add to the gloom and prevent Apple from repeating its outstanding performance in the stock market over the past three years.

So, there are quite a few reasons why investors might want to sell Apple stock before the earnings report comes out. However, experienced investors should focus on the big picture, as the company may offer a surprise in both the short and long term.

It would be a bad idea to write Apple off, given the way it dominates the 5G smartphone market. According to Strategy Analytics, Apple has been the leading provider of 5G smartphones since it launched its first 5G-enabled device in the fourth quarter of 2020. More specifically, Apple controlled 26% of the 5G smartphone market in the third quarter of 2021, and it's unlikely to relinquish that position anytime soon.

That's because Apple has a huge user base in the upgrade window waiting to get their hands on a 5G-enabled iPhone. Wedbush Securities analyst Daniel Ives estimates that about 230 million iPhone users have not upgraded their phones in the past three and a half years, which means that Apple's sales could start rising once the supply chain issues are resolved.

The good news is that Wall Street is seeing improvements in Apple's supply chain. Wells Fargo analysts raised their price target on Apple stock to $205, indicating a 26% upside from Friday's close. Analyst Aaron Rakers says the combination of an improving supply chain and strong demand for Apple's products could help it maintain its growth momentum.

CFRA Research also has a similar view, saying that supply constraints are likely to ease in the first half of the year, and Apple could gain share in markets such as China. Not surprisingly, analysts believe the tech giant could beat expectations. Katy Huberty of Morgan Stanley estimates that Apple sold 83 million iPhones last quarter, beating expectations of 80 million units.

In addition, Huberty predicts that Apple will sell 55 million iPhones this quarter, beating market expectations. Thus, Apple may beat expectations when it releases its earnings report, and that will help the stock regain its strength. More importantly, tech stocks can maintain their momentum into the future, as they are on several appetizing catalysts.

Overall, a strong report and optimistic outlook can lift stocks and make them more expensive. That's why investors might consider buying Apple stock ahead of the quarterly report, as it's currently trading at 29 times earnings guidance, a small discount from the 31.6 times earnings at which it traded last year.

Apple | Fundamental AnalysisApple has just become the first company whose market capitalization has reached $3 trillion. The company's stock lately reached new highs on the back of robust iPhone 13 sales, but there is more in store.

Experts predict the tech titan to release two new products in the next several years, even a foldable phone. Apple is still in growth mode, with annual free cash flow approaching $100 billion a year. Next, we'll tell you why it's worth buying stock to start 2022.

First, the iPhone 13 is a real success.

Apple has been successful in dealing with supply chain disruptions. The company's fourth fiscal quarter (ended Sept. 25) saw a 29% year-over-year increase in revenue, even though CEO Tim Cook called last quarter's supply chain problems "more significant than expected." Investors can take credit for the growing demand for all Apple products, as sales of Macs, iPhones, iPads, wearables, home products, and accessories hit record highs last quarter, and that momentum likely continued after the holidays.

Last month, a Morgan Stanley analyst noted that iPhone shipments in China were up 46% over November of last year. What's more, over the holidays, order fulfillment times for the iPhone 13 shrank to two days from nearly three weeks after launch.

Analysts now expect the company's first quarter of fiscal 2022 to see a 6% year-over-year increase in revenue and adjusted earnings per share of $1.88, up from $1.68 a year earlier.

Second, the company's new products should not be overlooked.

Investors are undervaluing the power of the current 5G upgrade cycle. During Verizon's Q3 earnings report, CEO Hans Westberg said consumers are embracing 5G much faster than 4G. Right now, 25 percent of the consumer phone base is using 5G-enabled devices, up from 10 percent in the first year after the 4G launch.

And if the 5G update slows down in a few years, Apple could announce a foldable smartphone in 2023, according to reports. That wouldn't be surprising, since Samsung already has Galaxy Z Fold3 and Flip3 foldable phones, and Apple is usually late in terms of hardware innovation. But when Apple finally does come along, it always executes the new technology better than the competition.

Samsung's Galaxy Z foldable phones, for example, have been criticized for their weak battery life and creases where the screen folds. Apple's foldable device likely won't have such shortcomings, given its longer development time, and that could make it the most popular foldable phone on the market.

The company is also expected to announce a long-discussed virtual reality/ augmented reality headset this year. The Apple headset won't be available until 2023, but the product could drive sales at the same level as Apple's other wearable devices, which currently account for about 10% of total sales (along with the Home and Accessories categories).

Well, and of course, the important point is the increasing free cash flow, share repurchases, and dividends.

The company's stock is not cheap, but with a price to free cash flow ratio of 31, it's hard to argue that Apple is overvalued.

The company's annual free cash flow is approaching $100 billion, and management is giving it all back to shareholders. Apple spent $84.9 billion on stock buybacks and $14.5 billion on dividends last year, bringing its dividend yield to 0.51%. When you believe that Apple's free cash flow continues to grow, up 55% over the past three years, the stock can grow without any expansion in valuation multiples.

Moreover, share repurchases work as expected, reducing the number of shares outstanding and therefore providing more free cash flow per share. Apple's free cash flow per share has grown 77% over the past three years.

Further 5G upgrades, demand for new products, and continued growth in the high-value services segment should result in even more free cash flow over the next few years, driving the company's stock up.

Of course, an economic downturn or major market correction could cause Apple's stock price to drop before it grows. But these are short-term risks that we all accept as investors. If you buy Apple stock today intending to hold it for the long term, you will be in a strong position to get an attractive return on your investment that will parallel the underlying growth of that business.

Apple Tweaks App Store AlgorithmApple Tweaks App Store Algorithm

In a recent turn of events after coming under fire for antitrust concerns, Apple revised its App Store’s search algorithm.

On Monday, a widely-popular news publication reported that the iPhone-maker is trying to limit its own apps dominating top spots. Apple Inc. did not comment on the report.

The news publication also added that Apple tweaked its App Store algorithm in July. It also conducted an analysis of search results in over six years, showing ‘Apple’s own apps mostly ranking first. Since 2016, the tech giant’s self-published apps dominated at least 700 search terms in the store.

Additionally, the newspaper reported that its analysis encompassed rankings of over 1,800 specific apps across 13 keywords since 2013. Another well-known financial news publication supports the credibility of the examination, showing similar findings regarding the subject.

Following the tweaks in July, Apple’s own apps started appearing less at the top ranks of the search results.

According to the smartphone manufacturer, its apps appeared at the uppermost listings as the former algorithm’s design functions this way. When a user searches for a keyword, the App Store lists multiple apps from the developer, much like personalized ads.

For instance, every time a user searches for a specific game, other applications from the same developer might show up. In a similar fashion, common search terms like “music” or “books” would put up Apple Music or Apple Books.

Despite showing related apps from other developers, this forces competitors further below the search ranks.

Apple’s App Store practices have come under scrutiny over antitrust concerns in Europe recently. The U.S. Department of Justice is now also considering an Apple probe, albeit being uncertain on specific angles to examine.

200 Million of New Apple Products to Drive Sales In

In light of all the issues the company is facing, Apple products persist in dominating a large market portion.

In addition, according to analysts, the tech giant could sell around 200 million of its latest iPhone products. Many existing users are now exchanging their older models for the new iteration of the iPhone. Demand is also growing over in China in spite of the long-drawn-out tariff war.

On Tuesday, Apple is widely expected to launch three brand new models of its most popular product.

Tech analysts believe that Apple will launch a new set of iPhone 11s this year, which include a 5.8-inch iPhone 11 Pro, 6.5-inch 11 Pro Max and a budget-friendly 6.1-inch 11R.

In over 12 months, 180 million of these Apple products could sell due to the anticipated upgrade cycle. Around 60 million to 70 million are consumers from China, according to tech financial experts.

Currently, 900 million iPhones are active worldwide. Estimates show that 200 million of these are iPhone 6 and earlier models, whose users have now set for an upgrade.

Chinese demand over Apple products has spiked this year, mainly uplifted by Chinese online retailers selling iPhones at discounted prices.

Apple is facing charges of 15% since September 1 as imposed by the U.S. government. The levies target Apple products made in China, such as smartwatches and wireless headphones. An additional tariff on the iPhone should also take effect on December 15.

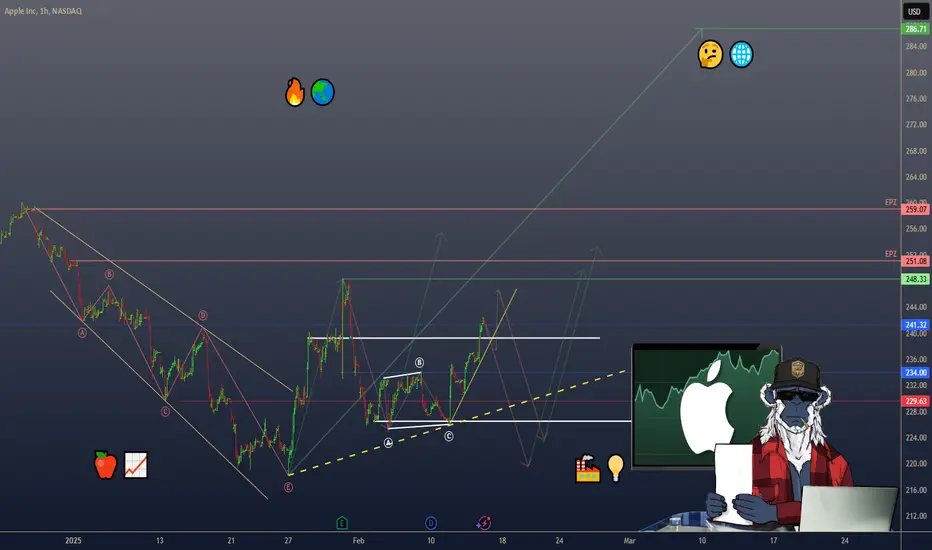

APPLE ($AAPL) – Q1 FY25 EARNINGS & WHAT’S NEXT APPLE ( NASDAQ:AAPL ) – Q1 FY25 EARNINGS & WHAT’S NEXT

(1/8)

Revenue: $124.3B (+4% YoY) – A new all-time record! Services soared +14% to $26.3B, offsetting a slight dip in iPhone sales. Let’s see how Apple’s holding up. 🍎📈

(2/8) – EARNINGS BEAT

• EPS: $2.40 (beat by $0.06)

• Gross margin: 46.9%, topping estimates 🔥

• Despite China sales dropping 11% to $18.51B, Apple still racked up big gains elsewhere 🌏

(3/8) – SECTOR SNAPSHOT

• Market cap $3.5T+, P/E ~30

• Some call it pricey vs. tech peers, but brand strength + services + potential AI expansions = possible undervaluation 🤔

• Compares favorably to Microsoft, Samsung, etc., given stable product + services synergy 🌐

(4/8) – RISKS TO WATCH

• Geopolitical: China manufacturing & sales reliance → Trade tensions? Tariffs? 🏭

• Innovation Pace: Competitors could leapfrog Apple in AI or other emerging tech 💡

• Regulatory: Antitrust cases (App Store) could pinch profitability ⚖️

• Economy: Premium pricing in downturn—brand loyalty helps, but can’t ignore recession effects 💸

(5/8) – SWOT HIGHLIGHTS

Strengths:

Legendary brand loyalty & huge install base

Growing services revenue (+14%!)

Massive cash reserves for R&D & buybacks

Weaknesses:

Heavy dependence on iPhone sales

China manufacturing concentration

Opportunities:

AI, AR/VR expansions (Vision Pro, maybe more)

Emerging markets → untapped smartphone penetration 🌍

Services sector continuing to expand ⚡

Threats:

Fierce competition (especially in China) 🦖

Trade tensions & supply chain hiccups 🌐

Shifts in consumer tech tastes or new disruptors

(6/8) – CHINA SALES DENT

• China down 11%—that’s a chunk given its importance

• Local giants (Xiaomi, Huawei) are snapping at Apple’s heels 🦾

• Will Vision Pro + AI upgrades woo Chinese consumers back? 🤔

(7/8) – Is Apple undervalued at a $3.5T market cap & P/E of 30?

1️⃣ Bullish—Brand power + AI = unstoppable 🍀

2️⃣ Neutral—Solid, but watch those China risks 🔍

3️⃣ Bearish—Too expensive, competition’s rising 🐻

Vote below! 🗳️👇

Apple partners with OpenAI to enhance iPhone AI capabilitiesApple Inc. has reportedly reached an agreement with OpenAI’s Sam Altman, marking a significant step for Apple in the artificial intelligence domain. This partnership will be officially announced at Apple’s upcoming developer conference next week. The collaboration involves integrating ChatGPT into the iPhone operating system, aiming to enhance the functionality of Apple services significantly.

This strategic alliance not only aims to boost the development trajectory of both Apple and OpenAI but also adds a symbolic touch as Sam Altman returns to the conference where he once participated as a developer 16 years ago, now appearing in a vastly different role.

Examining the investment potential, let’s review the technical analysis of Apple Inc. (NASDAQ: AAPL):

On the Daily (D1) timeframe, Apple’s stock has surpassed the resistance level at 192.70 USD, establishing support at 186.65 USD. The stock has been in an uptrend since the end of April 2024. If this trend reverses, a potential downside target could be 175.00 USD.

If the current uptrend maintains its momentum, a short-term investment with a target of 205.00 USD upon a rebound from the resistance level could be an opportunity. For a medium-term investment, the stock price could potentially rise to 220.00 USD if the upward trend continues.

—

Ideas and other content presented on this page should not be considered as guidance for trading or an investment advice. RoboMarkets bears no responsibility for trading results based on trading opinions described in these analytical reviews.

The material presented and the information contained herein is for information purposes only and in no way should be considered as the provision of investment advice for the purposes of Investment Firms Law L. 87(I)/2017 of the Republic of Cyprus or any other form of personal advice or recommendation, which relates to certain types of transactions with certain types of financial instruments.

Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69.88% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Apple Back to 182 Consolidation AreaApple Inc.

Explore

A Bearish Perspective on Apple Stock

Apple Inc., the tech giant known for its innovative products and services, has been a darling of Wall Street for many years. However, some analysts are turning bearish on the company’s stock. Here’s a closer look at why.

Underperformance in 2023

Despite gaining an impressive 49% in 2023, Apple’s stock was the worst-performing FAANG constituent of the year1. The company reported negative revenue growth in all four quarters of 2023, the first time since 2001 that the company’s revenues fell YoY for four straight quarters1.

Downgrades in 2024

The start of 2024 hasn’t been positive for Apple either, with three brokerages downgrading the stock within the first two weeks of the year1. Redburn, Piper Sandler, and Barclays have all downgraded the stock1. While Redburn and Piper Sandler now rate the stock as a “Hold” or equivalent, Barclays downgraded the stock to a “Sell” equivalent with a Street-low target price of $1601.

Concerns Over iPhone Sales

Some brokerages are turning bearish on Apple amid fears of an extended slowdown in iPhone sales1. Analysts are especially worried about the outlook for iPhone sales in China, which is the company’s third-biggest market behind the U.S. and Europe, and accounted for around 19% of its fiscal year 2023 revenues1. Apple is facing tough competition from domestic Chinese smartphone companies like Huawei and Xiaomi1.

APPLE - Great But Rebound could be Over NowAPPLE is what dreams are made off. Probably one of the Top-3 stocks that everyone and anyone would make sense to invest in.

But is the timing right?

We think not, as price is below 2 major resistances at 148$-154$

We feel Bitcoin is a better bargain today just above the 30,000$ mark.

APPLE News :

iPhone 14 leaks are beginning to snowball as their release edges closer, and now we have our best look yet at what the full range will look like.

Longtime Apple leaker Sonny Dickson is behind the latest scoop, releasing a hands-on video with dummy models of the iPhone 14, iPhone 14 Max, iPhone 14 Pro and iPhone 14 Pro Max. And it highlights the biggest external changes coming to the range. www.forbes.com

Apple's 2022 Event Plans : New Products and Software Coming in 2022: www.macrumors.com

APPLE is GREAT and it has been rebounding but sorry guys: we listen ONLY to our charts and our chart says NOT now, not today.

One Love,

the FXPROFESSOR

Apple Could Make Additional Gains Ahead Before Launch EventApple shares could post additional gains ahead of September 14 Launch event where the company usually present its new products.

This time Apple is expected to present Iphone 13, AirPods 3, brand new Apple Watch Series 7 with a widescreen. The company may also talk about its efforts to launch new MacBook. Analysts expect Company’s revenues to top $120 billion for the next year.

If we look at the long-term trend for Apple shares, it was smooth in November 2008 – May 2016. But since then it has accelerated to an exponential growth since January 2019. Since than shares soared by more than 340%, while company’s revenue increased by 400%.

Nevertheless, Apple shares are still seen attractive in the short-term despite climbing to the new all-time highs. And to understand this we have to look at the Apple shares monthly chart where it is clear that they have terminated correction in June and resumed climbing.

If we consider the depth of this correction from $145.09 to $116.21 next target upside levels may be recorded at $159.53 and $162.93. Long-term targets are at $174 and $185 respectively. The strong support level for the moment is at $150-151.5, highs of July, with a trend line from June 3 crossing these values. It prices would scale back to this support buy position may be considered as a perspective idea.

Moreover, Apple shares may perform better than the market ahead of the Launch Event, as it was on Tuesday when they gained 1.56% vs decline of Dow Jones index by 0.76% and S&P 500 by 0.34%.

Apple ready to flyApple has consolidated for last 4 weeks. Apple weekly resistance is around 121 which bears were unable to break with rsi divergence , i feel apple is ready to fly. (trading idea here is for education and entertainment purpose. Do trading at your own risk).

Why apple should go up

1- good fundamental

2- market got bullish

3- my experience has been apple follows weird pattern, usually it does not follow market direction

4- sitting on 4 week of support

5- apple car will be arriving in next few years

6- apple sitting on large amount of cash

APPLE IS TOPPING OUT - SHORT ITApple at 207 is fully valued according to a DCF valuation, no room to move higher into overvalued territory. Apple's iPhone sales are in decline from their latest form 10Q and the services business is growing slowly. I think the trade war with China has affected Apple's earnings and growth, also competition from Samsung and other cheaper phones. The iPhone is now a mature product, it has everything people want and sales of lower models are popular as people don't want to spend $1000+ for a phone. Apple's shares may fall to the lower channel line before consolidating there. The RSI, ROC and MACD are all topping out indicating weakness. Apple will announce its next quarterly earnings on Monday. If they disappoint, expect a fall in share price.

Also, I think the earnings growth rate projections are too high. 10% pa growth in earnings is too high for a company that is so large with a mature product (iPhone) and so many competitors. Keep in mind a Samsung Galaxy A30 smartphone costs only $300, much lower than an Apple's iPhone and has better battery life and the same functionality. Apple's products are overvalued and together with its share price will fall.

APPLE (AAPL)Apple's innovation shown in iPhone 14 is not likely enough to entice consumers to stretch their budgets in the current macroeconomic environment

40% of Warren Buffett portfolio still belongs to Apple?! for most people and traders I think its a slow asset class and like Tim Apple! sorry Cook ,Warren like to play safe too

Apple price showed a good reaction to 135 support and now heading to 149, for Scalpers breaking 150 resistance can be a good long opportunity and for investors AAPL still can back to 125$ levels so

there is no reason to fomo

Apple sees drop in revenue and net incomeApple delivered its financial results for the second quarter of fiscal year 2024. According to the report, the company generated revenue worth $90.753 billion, down 4.3% YoY, and net income of $23.636 billion, representing a decrease of 2.16% YoY. Operating income amounted to $27.9 billion for the same period, falling 1.5% YoY. In addition to that, Apple announced the largest share buyback program in the company’s history, amounting to $110 billion.

Net revenue = $90.7 billion (-4.3% YoY) vs. $94.8 billion in FY2Q23

Net income = $23.6 billion (-2.16% YoY) vs. $24.1 billion in FY2Q23

Operating income = $27.9 billion (-1.5% YoY) vs. $28.3 billion in FY2Q23

Earnings per share = $1.53 (0% YoY) vs. $1.53 in FY2Q23

Illustration 1.01

The illustration above shows Apple's price action in the aftermarket, with shares soaring more than 7%.

Additional information

Operating costs rose 5.2% YoY to $14.3 billion.

iPhone sales fell 10.4% YoY.

Mac sales increased nearly 4% YoY.

iPad sales went down 16.6% YoY.

Sales in the wearable, home, and accessories category dropped 9.6% YoY.

Revenue from services grew by 14.1%

The company’s liabilities declined by about 9.4% YoY.

Apple increased its dividend to $0.25 per share.

Forward guidance

Apple did not provide any forward guidance. However, its CEO, Tim Cook, said the company plans to announce in regard to artificial intelligence. On top of that, he expressed optimism about the company’s operations in China.

Please feel free to express your ideas and thoughts in the comment section.

DISCLAIMER: This analysis is not intended to encourage any buying or selling of any particular securities. Furthermore, it should not be a basis for taking any trade action by an individual investor or any other entity. Therefore, your own due diligence is highly advised before entering a trade.

Apple's Earnings: Should You Take Some Profits Off The Table?Apple's Earnings: Should You Take Some Profits Off The Table? Apple stock has been on a roll lately, up 50% heading into earnings. However, given that earning date is just around the corner on August 3, and historically, Apple stock tends to sell off in the months of August and September, it's time to consider the wisest course of action. Many investors are pondering whether to take some profits off the table, especially considering that the company's revenue, net income, and net profit margin have all been declining in recent quarters. As we rationalize why or why not to sell Apple's shares, let's review everything you need to know about Apple's earnings and stock performance.