Open Vertical Lines [TradeWithRon]This indicator allows traders to draw vertical lines manually or automatically based on the current or specified higher timeframes. It is a versatile tool designed to help users identify and mark significant changes in the market, such as new candle formations, based on a selected or auto-adjusted timeframe.

Open Source

Features:

Timeframe Customization: Users can either manually specify a desired timeframe (e.g., 1-hour, 1-day, etc.) or enable the "Auto" feature, which automatically adjusts the timeframe based on the current chart's timeframe for better alignment with different trading strategies.

Customizable Line Style: The vertical line can be drawn in three different styles: Solid, Dashed, or Dotted, giving users the flexibility to choose their preferred appearance for better chart readability.

Line Color: Users can select the color of the vertical line with transparency options to match their chart's visual preferences.

Auto Timeframe Adjustments: The "Auto Align" option dynamically adjusts the timeframe used for vertical lines depending on the chart's current timeframe. For example, if you’re using a lower timeframe (e.g., 5 minutes), the indicator will automatically switch to a higher timeframe (e.g., 1 hour or daily) to mark vertical lines, ensuring the lines correspond to higher timeframe price action.

Vertical Line Placement:

A vertical line is placed each time a new candle appears on the chart, marking key moments for the user to analyze market movements. This can be helpful for marking the start of new trading sessions or significant events in the market.

How to Use:

1. Apply the indicator to your chart.

2. Configure the preferred timeframe settings (either fixed or auto-align).

3. Customize the line style and color according to your visual preference.

4. The indicator will automatically place vertical lines on the chart when a new candle is formed, based on your selected timeframe.

Cycleanalysis

[GYTS-CE] Market Regime Detector🧊 Market Regime Detector (Community Edition)

🌸 Part of GoemonYae Trading System (GYTS) 🌸

🌸 --------- INTRODUCTION --------- 🌸

💮 What is the Market Regime Detector?

The Market Regime Detector is an advanced, consensus-based indicator that identifies the current market state to increase the probability of profitable trades. By distinguishing between trending (bullish or bearish) and cyclic (range-bound) market conditions, this detector helps you select appropriate tactics for different environments. Instead of forcing a single strategy across all market conditions, our detector allows you to adapt your approach based on real-time market behaviour.

💮 The Importance of Market Regimes

Markets constantly shift between different behavioural states or "regimes":

• Bullish trending markets - characterised by sustained upward price movement

• Bearish trending markets - characterised by sustained downward price movement

• Cyclic markets - characterised by range-bound, oscillating behaviour

Each regime requires fundamentally different trading approaches. Trend-following strategies excel in trending markets but fail in cyclic ones, while mean-reversion strategies shine in cyclic markets but underperform in trending conditions. Detecting these regimes is essential for successful trading, which is why we've developed the Market Regime Detector to accurately identify market states using complementary detection methods.

🌸 --------- KEY FEATURES --------- 🌸

💮 Consensus-Based Detection

Rather than relying on a single method, our detector employs two complementary detection methodologies that analyse different aspects of market behaviour:

• Dominant Cycle Average (DCA) - analyzes price movement relative to its lookback period, a proxy for the dominant cycle

• Volatility Channel - examines price behaviour within adaptive volatility bands

These diverse perspectives are synthesised into a robust consensus that minimises false signals while maintaining responsiveness to genuine regime changes.

💮 Dominant Cycle Framework

The Market Regime Detector uses the concept of dominant cycles to establish a reference framework. You can input the dominant cycle period that best represents the natural rhythm of your market, providing a stable foundation for regime detection across different timeframes.

💮 Intuitive Parameter System

We've distilled complex technical parameters into intuitive controls that traders can easily understand:

• Adaptability - how quickly the detector responds to changing market conditions

• Sensitivity - how readily the detector identifies transitions between regimes

• Consensus requirement - how much agreement is needed among detection methods

This approach makes the detector accessible to traders of all experience levels while preserving the power of the underlying algorithms.

💮 Visual Market Feedback

The detector provides clear visual feedback about the current market regime through:

• Colour-coded chart backgrounds (purple shades for bullish, pink for bearish, yellow for cyclic)

• Colour-coded price bars

• Strength indicators showing the degree of consensus

• Customizable colour schemes to match your preferences or trading system

💮 Integration in the GYTS suite

The Market Regime Detector is compatible with the GYTS Suite , i.e. it passes the regime into the 🎼 Order Orchestrator where you can set how to trade the trending and cyclic regime.

🌸 --------- CONFIGURATION SETTINGS --------- 🌸

💮 Adaptability

Controls how quickly the Market Regime detector adapts to changing market conditions. You can see it as a low-frequency, long-term change parameter:

Very Low: Very slow adaptation, most stable but may miss regime changes

Low: Slower adaptation, more stability but less responsiveness

Normal: Balanced between stability and responsiveness

High: Faster adaptation, more responsive but less stable

Very High: Very fast adaptation, highly responsive but may generate false signals

This setting affects lookback periods and filter parameters across all detection methods.

💮 Sensitivity

Controls how sensitive the detector is to market regime transitions. This acts as a high-frequency, short-term change parameter:

Very Low: Requires substantial evidence to identify a regime change

Low: Less sensitive, reduces false signals but may miss some transitions

Normal: Balanced sensitivity suitable for most markets

High: More sensitive, detects subtle regime changes but may have more noise

Very High: Very sensitive, detects minor fluctuations but may produce frequent changes

This setting affects thresholds for regime detection across all methods.

💮 Dominant Cycle Period

This parameter allows you to specify the market's natural rhythm in bars. This represents a complete market cycle (up and down movement). Finding the right value for your specific market and timeframe might require some experimentation, but it's a crucial parameter that helps the detector accurately identify regime changes. Most of the times the cycle is between 20 and 40 bars.

💮 Consensus Mode

Determines how the signals from both detection methods are combined to produce the final market regime:

• Any Method (OR) : Signals bullish/bearish if either method detects that regime. If methods conflict (one bullish, one bearish), the stronger signal wins. More sensitive, catches more regime changes but may produce more false signals.

• All Methods (AND) : Signals only when both methods agree on the regime. More conservative, reduces false signals but might miss some legitimate regime changes.

• Weighted Decision : Balances both methods with equal weighting. Provides a middle ground between sensitivity and stability.

Each mode also calculates a continuous regime strength value that's used for colour intensity in the 'unconstrained' display mode.

💮 Display Mode

Choose how to display the market regime colours:

• Unconstrained regime: Shows the regime strength as a continuous gradient. This provides more nuanced visualisation where the intensity of the colour indicates the strength of the trend.

• Consensus only: Shows only the final consensus regime with fixed colours based on the detected regime type.

The background and bar colours will change to indicate the current market regime:

• Purple shades: Bullish trending market (darker purple indicates stronger bullish trend)

• Pink shades: Bearish trending market (darker pink indicates stronger bearish trend)

• Yellow: Cyclic (range-bound) market

💮 Custom Colour Options

The Market Regime Detector allows you to customize the colour scheme to match your personal preferences or to coordinate with other indicators:

• Use custom colours: Toggle to enable your own colour choices instead of the default scheme

• Transparency: Adjust the transparency level of all regime colours

• Bullish colours: Define custom colours for strong, medium, weak, and very weak bullish trends

• Bearish colours: Define custom colours for strong, medium, weak, and very weak bearish trends

• Cyclic colour: Define a custom colour for cyclic (range-bound) market conditions

🌸 --------- DETECTION METHODS --------- 🌸

💮 Dominant Cycle Average (DCA)

The Dominant Cycle Average method forms a key part of our detection system:

1. Theoretical Foundation :

The DCA method builds on cycle analysis and the observation that in trending markets, price consistently remains on one side of a moving average calculated using the dominant cycle period. In contrast, during cyclic markets, price oscillates around this average.

2. Calculation Process :

• We calculate a Simple Moving Average (SMA) using the specified lookback period - a proxy for the dominant cycle period

• We then analyse the proportion of time that price spends above or below this SMA over a lookback window. The theory is that the price should cross the SMA each half cycle, assuming that the dominant cycle period is correct and price follows a sinusoid.

• This lookback window is adaptive, scaling with the dominant cycle period (controlled by the Adaptability setting)

• The different values are standardised and normalised to possess more resolving power and to be more robust to noise.

3. Regime Classification :

• When the normalised proportion exceeds a positive threshold (determined by Sensitivity setting), the market is classified as bullish trending

• When it falls below a negative threshold, the market is classified as bearish trending

• When the proportion remains between these thresholds, the market is classified as cyclic

💮 Volatility Channel

The Volatility Channel method complements the DCA method by focusing on price movement relative to adaptive volatility bands:

1. Theoretical Foundation :

This method is based on the observation that trending markets tend to sustain movement outside of normal volatility ranges, while cyclic markets tend to remain contained within these ranges. By creating adaptive bands that adjust to current market volatility, we can detect when price behaviour indicates a trending or cyclic regime.

2. Calculation Process :

• We first calculate a smooth base channel center using a low pass filter, creating a noise-reduced centreline for price

• True Range (TR) is used to measure market volatility, which is then smoothed and scaled by the deviation factor (controlled by Sensitivity)

• Upper and lower bands are created by adding and subtracting this scaled volatility from the centreline

• Price is smoothed using an adaptive A2RMA filter, which has a very flat and stable behaviour, to reduce noise while preserving trend characteristics

• The position of this smoothed price relative to the bands is continuously monitored

3. Regime Classification :

• When smoothed price moves above the upper band, the market is classified as bullish trending

• When smoothed price moves below the lower band, the market is classified as bearish trending

• When price remains between the bands, the market is classified as cyclic

• The magnitude of price's excursion beyond the bands is used to determine trend strength

4. Adaptive Behaviour :

• The smoothing periods and deviation calculations automatically adjust based on the Adaptability setting

• The measured volatility is calculated over a period proportional to the dominant cycle, ensuring the detector works across different timeframes

• Both the center line and the bands adapt dynamically to changing market conditions, making the detector responsive yet stable

This method provides a unique perspective that complements the DCA approach, with the consensus mechanism synthesising insights from both methods.

🌸 --------- USAGE GUIDE --------- 🌸

💮 Starting with Default Settings

The default settings (Normal for Adaptability and Sensitivity, Weighted Decision for Consensus Mode) provide a balanced starting point suitable for most markets and timeframes. Begin by observing how these settings identify regimes in your preferred instruments.

💮 Finding the Optimal Dominant Cycle

The dominant cycle period is a critical parameter. Here are some approaches to finding an appropriate value:

• Start with typical values, usually something around 25 works well

• Visually identify the average distance between significant peaks and troughs

• Experiment with different values and observe which provides the most stable regime identification

• Consider using cycle-finding indicators to help identify the natural rhythm of your market

💮 Adjusting Parameters

• If you notice too many regime changes → Decrease Sensitivity or increase Consensus requirement

• If regime changes seem delayed → Increase Adaptability

• If a trending regime is not detected, the market is automatically assigned to be in a cyclic state

• If you want to see more nuanced regime transitions → Try the "unconstrained" display mode (note that this will not affect the output to other indicators)

💮 Trading Applications

Regime-Specific Strategies:

• Bullish Trending Regime - Use trend-following strategies, trail stops wider, focus on breakouts, consider holding positions longer, and emphasize buying dips

• Bearish Trending Regime - Consider shorts, tighter stops, focus on breakdown points, sell rallies, implement downside protection, and reduce position sizes

• Cyclic Regime - Apply mean-reversion strategies, trade range boundaries, apply oscillators, target definable support/resistance levels, and use profit-taking at extremes

Strategy Switching:

Create a set of rules for each market regime and switch between them based on the detector's signal. This approach can significantly improve performance compared to applying a single strategy across all market conditions.

GYTS Suite Integration:

• In the GYTS 🎼 Order Orchestrator, select the '🔗 STREAM-int 🧊 Market Regime' as the market regime source

• Note that the consensus output (i.e. not the "unconstrained" display) will be used in this stream

• Create different strategies for trending (bullish/bearish) and cyclic regimes. The GYTS 🎼 Order Orchestrator is specifically made for this.

• The output stream is actually very simple, and can possibly be used in indicators and strategies as well. It outputs 1 for bullish, -1 for bearish and 0 for cyclic regime.

🌸 --------- FINAL NOTES --------- 🌸

💮 Development Philosophy

The Market Regime Detector has been developed with several key principles in mind:

1. Robustness - The detection methods have been rigorously tested across diverse markets and timeframes to ensure reliable performance.

2. Adaptability - The detector automatically adjusts to changing market conditions, requiring minimal manual intervention.

3. Complementarity - Each detection method provides a unique perspective, with the collective consensus being more reliable than any individual method.

4. Intuitiveness - Complex technical parameters have been abstracted into easily understood controls.

💮 Ongoing Refinement

The Market Regime Detector is under continuous development. We regularly:

• Fine-tune parameters based on expanded market data

• Research and integrate new detection methodologies

• Optimise computational efficiency for real-time analysis

Your feedback and suggestions are very important in this ongoing refinement process!

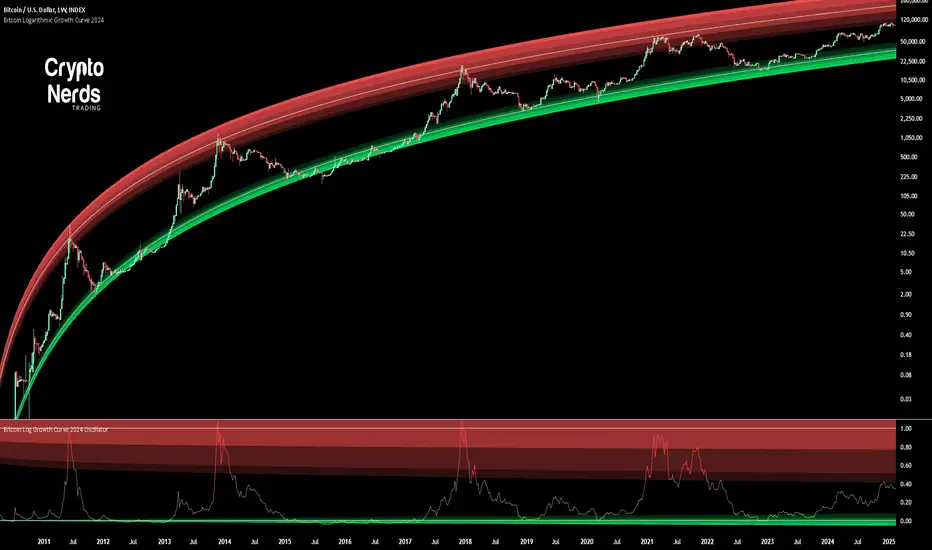

Bitcoin Log Growth Curve OscillatorThis script presents the oscillator version of the Bitcoin Logarithmic Growth Curve 2024 indicator, offering a new perspective on Bitcoin’s long-term price trajectory.

By transforming the original logarithmic growth curve into an oscillator, this version provides a normalized view of price movements within a fixed range, making it easier to identify overbought and oversold conditions.

For a comprehensive explanation of the mathematical derivation, underlying concepts, and overall development of the Bitcoin Logarithmic Growth Curve, we encourage you to explore our primary script, Bitcoin Logarithmic Growth Curve 2024, available here . This foundational script details the regression-based approach used to model Bitcoin’s long-term price evolution.

Normalization Process

The core principle behind this oscillator lies in the normalization of Bitcoin’s price relative to the upper and lower regression boundaries. By applying Min-Max Normalization, we effectively scale the price into a bounded range, facilitating clearer trend analysis. The normalization follows the formula:

normalized price = (upper regresionline − lower regressionline) / (price − lower regressionline)

This transformation ensures that price movements are always mapped within a fixed range, preventing distortions caused by Bitcoin’s exponential long-term growth. Furthermore, this normalization technique has been applied to each of the confidence interval lines, allowing for a structured and systematic approach to analyzing Bitcoin’s historical and projected price behavior.

By representing the logarithmic growth curve in oscillator form, this indicator helps traders and analysts more effectively gauge Bitcoin’s position within its long-term growth trajectory while identifying potential opportunities based on historical price tendencies.

4-Year Cycles [jpkxyz]Overview of the Script

I wanted to write a script that encompasses the wide-spread macro fund manager investment thesis: "Crypto is simply and expression of macro." A thesis pioneered by the likes of Raoul Pal (EXPAAM) , Andreesen Horowitz (A16Z) , Joe McCann (ASYMETRIC) , Bob Loukas and many more.

Cycle Theory Background:

The 2007-2008 financial crisis transformed central bank monetary policy by introducing:

- Quantitative Easing (QE): Creating money to buy assets and inject liquidity

- Coordinated global monetary interventions

Proactive 4-year economic cycles characterised by:

- Expansionary periods (low rates, money creation)

- Followed by contraction/normalisation

Central banks now deliberately manipulate liquidity, interest rates, and asset prices to control economic cycles, using monetary policy as a precision tool rather than a blunt instrument.

Cycle Characteristics (based on historical cycles):

- A cycle has 4 seasons (Spring, Summer, Fall, Winter)

- Each season with a cycle lasts 365 days

- The Cycle Low happens towards the beginning of the Spring Season of each new cycle

- This is followed by a run up throughout the Spring and Summer Season

- The Cycle High happens towards the end of the Fall Season

- The Winter season is characterised by price corrections until establishing a new floor in the Spring of the next cycle

Key Functionalities

1. Cycle Tracking

- Divides market history into 4-year cycles (Spring, Summer, Fall, Winter)

- Starts tracking cycles from 2011 (first cycle after the 2007 crisis cycle)

- Identifies and marks cycle boundaries

2. Visualization

- Colors background based on current cycle season

- Draws lines connecting:

- Cycle highs and lows

- Inter-cycle price movements

- Adds labels showing:

- Percentage gains/losses between cycles

- Number of days between significant points

3. Customization Options

- Allows users to customize:

- Colors for each season

- Line and label colors

- Label size

- Background opacity

Detailed Mechanism

Cycle Identification

- Uses a modulo calculation to determine the current season in the 4-year cycle

- Preset boundary years include 2015, 2019, 2023, 2027

- Automatically tracks and marks cycle transitions

Price Analysis

- Tracks highest and lowest prices within each cycle

- Calculates percentage changes:

- Intra-cycle (low to high)

- Inter-cycle (previous high to current high/low)

Visualization Techniques

- Background color changes based on current cycle season

- Dashed and solid lines connect significant price points

- Labels provide quantitative insights about price movements

Unique Aspects

1. Predictive Cycle Framework: Provides a structured way to view market movements beyond traditional technical analysis

2. Seasonal Color Coding: Intuitive visual representation of market cycle stages

3. Comprehensive Price Tracking: Captures both intra-cycle and inter-cycle price dynamics

4. Highly Customizable: Users can adjust visual parameters to suit their preferences

Potential Use Cases

- Technical analysis for long-term investors

- Identifying market cycle patterns

- Understanding historical price movement rhythms

- Educational tool for market cycle theory

Limitations/Considerations

- Based on a predefined 4-year cycle model (Liquidity Cycles)

- Historic Cycle Structures are not an indication for future performance

- May not perfectly represent all market behavior

- Requires visual interpretation

This script is particularly interesting for investors who believe in cyclical market theories and want a visual, data-driven representation of market stages.

Financial Astrology Ceres SpeedCeres speed influence is clear for BTCUSD and confirms other planets speed observations, volatility increase as speed is accelerating. The most dominant bull runs of BTC have occurred when Ceres was moving direct in speed and accelerating. In many cases the trend reversed or stalled where Ceres enter into deceleration period. The only exception was March 2019 where BTCUSD price increased while Ceres was moving retrograde but as we know, all the planets are acting simultaneously so careful exploration needs to be made with the other planets and asteroids speed phases during that same period to conclude why in that observation the volatility was strong.

Note: The Ceres speed indicator is based on an ephemeris array that covers years 2010 to 2030, prior or after this years the data is not available, this daily ephemeris are based on UTC time so in order to align properly with the price bars times you should set UTC as your chart timezone.

[TheMandalor] Invert or Mirror Chart SUPPORT RESSISTANTThis is a new idea to find supports and resistant’s for any charts.

What is the concept of this indicator:

1. It is used close and inverted it on chart

2. When the real chart and the inverted chart is crossing together several times, this point will be important on this concept that means the price will care about this point again and again.

3. When you draw a horizontal line as support and resistance check it with this indicator too, if your support and resistance is touched with inverted chart, it will be more important than normal support/ resistance.

4. This indicator has plot candle too, it means you can compare regular chart with the inverted one at same time if you need.

Here is the steps:

1. When you add the indicator to your chart it will add your ticker as inverted.

2. Change your chart type to line chart.

3. Fix your scale in both sides left and right (the indicator's side is on the left).

4. Now you must have two type of line charts, one is yours (The blue one) and one is plotted with this indicator (The purple one).

5. Draw a horizontal line where these two lines have more crossing at the middle of chart, this line will be a powerful line later.

6. Find other more crossed points and draw horizontal line for them too.

7. Now you can see these indicator's support and resistant’s, now you can remove the indicator and watch how the price will touch, reverse, or stay on your new type of support and resistant’s lines.

PS: I have added candle plotting too if you need it.

Bitcoin Logarithmic Growth Curve 2024The Bitcoin logarithmic growth curve is a concept used to analyze Bitcoin's price movements over time. The idea is based on the observation that Bitcoin's price tends to grow exponentially, particularly during bull markets. It attempts to give a long-term perspective on the Bitcoin price movements.

The curve includes an upper and lower band. These bands often represent zones where Bitcoin's price is overextended (upper band) or undervalued (lower band) relative to its historical growth trajectory. When the price touches or exceeds the upper band, it may indicate a speculative bubble, while prices near the lower band may suggest a buying opportunity.

Unlike most Bitcoin growth curve indicators, this one includes a logarithmic growth curve optimized using the latest 2024 price data, making it, in our view, superior to previous models. Additionally, it features statistical confidence intervals derived from linear regression, compatible across all timeframes, and extrapolates the data far into the future. Finally, this model allows users the flexibility to manually adjust the function parameters to suit their preferences.

The Bitcoin logarithmic growth curve has the following function:

y = 10^(a * log10(x) - b)

In the context of this formula, the y value represents the Bitcoin price, while the x value corresponds to the time, specifically indicated by the weekly bar number on the chart.

How is it made (You can skip this section if you’re not a fan of math):

To optimize the fit of this function and determine the optimal values of a and b, the previous weekly cycle peak values were analyzed. The corresponding x and y values were recorded as follows:

113, 18.55

240, 1004.42

451, 19128.27

655, 65502.47

The same process was applied to the bear market low values:

103, 2.48

267, 211.03

471, 3192.87

676, 16255.15

Next, these values were converted to their linear form by applying the base-10 logarithm. This transformation allows the function to be expressed in a linear state: y = a * x − b. This step is essential for enabling linear regression on these values.

For the cycle peak (x,y) values:

2.053, 1.268

2.380, 3.002

2.654, 4.282

2.816, 4.816

And for the bear market low (x,y) values:

2.013, 0.394

2.427, 2.324

2.673, 3.504

2.830, 4.211

Next, linear regression was performed on both these datasets. (Numerous tools are available online for linear regression calculations, making manual computations unnecessary).

Linear regression is a method used to find a straight line that best represents the relationship between two variables. It looks at how changes in one variable affect another and tries to predict values based on that relationship.

The goal is to minimize the differences between the actual data points and the points predicted by the line. Essentially, it aims to optimize for the highest R-Square value.

Below are the results:

It is important to note that both the slope (a-value) and the y-intercept (b-value) have associated standard errors. These standard errors can be used to calculate confidence intervals by multiplying them by the t-values (two degrees of freedom) from the linear regression.

These t-values can be found in a t-distribution table. For the top cycle confidence intervals, we used t10% (0.133), t25% (0.323), and t33% (0.414). For the bottom cycle confidence intervals, the t-values used were t10% (0.133), t25% (0.323), t33% (0.414), t50% (0.765), and t67% (1.063).

The final bull cycle function is:

y = 10^(4.058 ± 0.133 * log10(x) – 6.44 ± 0.324)

The final bear cycle function is:

y = 10^(4.684 ± 0.025 * log10(x) – -9.034 ± 0.063)

The main Criticisms of growth curve models:

The Bitcoin logarithmic growth curve model faces several general criticisms that we’d like to highlight briefly. The most significant, in our view, is its heavy reliance on past price data, which may not accurately forecast future trends. For instance, previous growth curve models from 2020 on TradingView were overly optimistic in predicting the last cycle’s peak.

This is why we aimed to present our process for deriving the final functions in a transparent, step-by-step scientific manner, including statistical confidence intervals. It's important to note that the bull cycle function is less reliable than the bear cycle function, as the top band is significantly wider than the bottom band.

Even so, we still believe that the Bitcoin logarithmic growth curve presented in this script is overly optimistic since it goes parly against the concept of diminishing returns which we discussed in this post:

This is why we also propose alternative parameter settings that align more closely with the theory of diminishing returns.

Our recommendations:

Drawing on the concept of diminishing returns, we propose alternative settings for this model that we believe provide a more realistic forecast aligned with this theory. The adjusted parameters apply only to the top band: a-value: 3.637 ± 0.2343 and b-parameter: -5.369 ± 0.6264. However, please note that these values are highly subjective, and you should be aware of the model's limitations.

Conservative bull cycle model:

y = 10^(3.637 ± 0.2343 * log10(x) - 5.369 ± 0.6264)

Atlantean Bitcoin Weekly Market Condition - Top/Bottom BTC Overview:

The "Atlantean Bitcoin Weekly Market Condition Detector - Top/Bottom BTC" is a specialized TradingView indicator designed to identify significant turning points in the Bitcoin market on a weekly basis. By analyzing long-term and short-term moving averages across two distinct resolutions, this indicator provides traders with valuable insights into potential market bottoms and tops, as well as the initiation of bull markets.

Key Features:

Market Bottom Detection: The script uses a combination of a simple moving average (SMA) and an exponential moving average (EMA) calculated over long and short periods to identify potential market bottoms. When these conditions are met, the script signals a "Market Bottom" label on the chart, indicating a possible buying opportunity.

Bull Market Start Indicator: When the short-term EMA crosses above the long-term SMA, it signals the beginning of a bull market. This is marked by a "Bull Market Start" label on the chart, helping traders to prepare for potential market upswings.

Market Top Detection: The script identifies potential market tops by analyzing the crossunder of long and short-term moving averages. A "Market Top" label is plotted, suggesting a potential selling point.

Customizable Moving Averages Display: Users can choose to display the moving averages used for detecting market tops and bottoms, providing additional insights into market conditions.

How It Works: The indicator operates by monitoring the interactions between the specified moving averages:

Market Bottom: Detected when the long-term SMA (adjusted by a factor of 0.745) crosses over the short-term EMA.

Bull Market Start: Detected when the short-term EMA crosses above the long-term SMA.

Market Top: Detected when the long-term SMA (adjusted by a factor of 2) crosses under the short-term SMA.

These conditions are highlighted on the chart, allowing traders to visualize significant market events and make informed decisions.

Intended Use: This indicator is best used on weekly Bitcoin charts. It’s designed to provide long-term market insights rather than short-term trading signals. Traders can use this tool to identify strategic entry and exit points during major market cycles. The optional display of moving averages can further enhance understanding of market dynamics.

Originality and Utility: Unlike many other indicators, this script not only highlights traditional market tops and bottoms but also identifies the aggressive start of bull markets, offering a comprehensive view of market conditions. The unique combination of adjusted moving averages makes this script a valuable tool for long-term Bitcoin traders.

Disclaimer: The signals provided by this indicator are based on historical data and mathematical calculations. They do not guarantee future market performance. Traders should use this tool as part of a broader trading strategy and consider other factors before making trading decisions. Not financial advice.

Happy Trading!

By Atlantean

Ehlers Band-Pass FilterHeyo,

This indicator is an original translation from Ehlers' book "Cycle Analytics for Traders Advanced".

First, I describe the indicator as usual and later you can find a very insightful quote of the book.

Key Features

Signal Line: Represents the output of the band-pass filter, highlighting the dominant cycle in the data.

Trigger Line: A leading indicator derived from the signal line, providing early signals for potential market reversals.

Dominant Cycle: Measures the dominant cycle period by counting the number of bars between zero crossings of the band-pass filter output.

Calculation:

The band-pass filter is implemented using a combination of high-pass and low-pass filters.

The filter's parameters, such as period and bandwidth, can be adjusted to tune the filter to specific market cycles.

The signal line is normalized using an Automatic Gain Control (AGC) to provide consistent amplitude regardless of price swings.

The trigger line is derived by applying a high-pass filter to the signal line, creating a leading

waveform.

Usage

The indicator is effective in identifying peaks and valleys in the market data.

It works best in cyclic market conditions and may produce false signals during trending periods.

The dominant cycle measurement helps traders understand the prevailing market cycle length, aiding in better decision-making.

Quoted from the Book

Band-Pass Filters

“A little of the data narrowly passed,” said Tom broadly.

Perhaps the least appreciated and most underutilized filter in technical analysis is the band-pass filter. The band-pass filter simultaneously diminishes the amplitude at low frequencies, qualifying it as a detrender, and diminishes the amplitude at high frequencies, qualifying it as a data smoother.

It passes only those frequency components from input to output in which the trader is interested. The filtering produced by a band-pass filter is superior because the rejection in the stop bands is related to its bandwidth. The degree of rejection of undesired frequency components is called selectivity. The band-stop filter is the dual of the band-pass filter. It rejects a band of frequency components as a notch at the output and passes all other frequency components virtually unattenuated. Since the bandwidth of the deep rejection in the notch is relatively narrow and since the spectrum of market cycles is relatively broad due to systemic noise, the band-stop filter has little application in trading.

Measuring the Cycle Period

The band-pass filter can be used as a relatively simple measurement of the dominant cycle.

A cycle is complete when the waveform crosses zero two times from the last zero crossing. Therefore, each successive zero crossing of the indicator marks a half cycle period. We can establish the dominant cycle period as twice the spacing between successive zero crossings.

When we measure the dominant cycle period this way, it is best to widen the pass band of the band-pass filter to avoid distorting the measurement simply due to the selectivity of the filter. Using an input bandwidth of 0.7 produces an octave-wide pass band. For example, if the center period of the filter is 20 and the relative bandwidth is 0.7, the bandwidth is 14. That means the pass band of the filter extends from 13-bar periods to 27-bar periods.

That is, roughly an octave exists because the longest period is twice the shortest period of the pass band. It is imperative that a high-pass filter is tuned one octave below the half-bandwidth edge of the band-pass filter to ensure a nominal zero mean of the filtered output. Without a zero mean, the zero crossings can have a substantial error.

Since the measurement of the dominant cycle can vary dramatically from zero crossing to zero

crossing, the code limits the change between measurements to be no more than 25 percent.

While measuring the changing dominant cycle period via zero crossings of the band-pass waveform is easy, it is not necessarily the most accurate method.

Best regards,

simwai

Good Luck with your trading! 🙌

Central Banks Balance Sheets ROI% ChangeIntroducing the "Central Banks Balance Sheets ROI% Change" indicator, a tool designed to offer traders and analysts an understanding of global liquidity dynamics.

This indicator tracks the Return on Investment (ROI) percentage changes across major central banks' balance sheets, providing insights into shifts in global economic liquidity not tied to cumulative figures but through ROI calculations, capturing the pulse of overall economic dynamics.

Key Enhancements:

ROI Period Customization: Users can now adjust the ROI calculation period, offering flexibility to analyze short-term fluctuations or longer-term trends in central bank activities, aligning with their strategic time horizons.

Chart Offset Feature: This new functionality allows traders to shift the chart view, aiding in the alignment of data visualization with other indicators or specific analysis needs, enhancing interpretive clarity.

Central Bank Selection: With options to include or exclude data from specific central banks among the world's top 15 economies (with the exception of Mexico and the consolidation of the EU's central bank data), traders can tailor the analysis to their regional focus or diversification strategies.

US M2 Option: Recognizing the significance of the M2 money supply as a liquidity metric, this indicator offers an alternative view focusing solely on the US M2, allowing for a concentrated analysis of the US liquidity environment.

Comprehensive Coverage: The tool covers a wide array of central banks, including the Federal Reserve, People's Bank of China, European Central Bank, and more, ensuring a broad and inclusive perspective on global liquidity.

Visualization Enhancements: A histogram plot vividly distinguishes between positive and negative ROI changes, offering an intuitive grasp of liquidity expansions or contractions at a glance.

This indicator is a strategic tool designed for traders who seek to understand the undercurrents of market liquidity and its implications on global markets.

Whether you're assessing the impact of central bank policies, gauging economic health, or identifying investment opportunities, the "Central Banks Balance Sheets ROI% Change" indicator offers a critical lens through which to view the complex interplay of global liquidity factors.

Market Time Cycle (Expo)█ Time Cycles Overview

Time cycles are a fascinating and powerful concept in the world of trading and investing. They are all about understanding and predicting the timing of market moves based on the premise that market events and price movements are not random, but instead occur in repeatable, cyclical patterns.

The Concept of Time Cycles: The foundation of time cycles lies in the belief that historical market patterns tend to repeat themselves over specific periods. These periods or cycles could be influenced by a myriad of factors like economic data releases, earnings reports, geopolitical events, or even natural human behavior. For example, some traders observe increased market activity around the start and end of a trading day, which is a form of intraday time cycle.

Understanding time cycles can provide traders with a roadmap, helping them anticipate potential trend shifts and make more informed decisions about when to buy or sell.

█ Indicator Overview

The Market Time Cycle (Expo) is designed to help traders track and analyze market cycles and generate signals for potential trading opportunities. It uses mathematical techniques to analyze market cycles and detect possible turning points. It does this by projecting the estimated cycle timeline and providing visual indications of cyclical phases through the use of color-coded lines and sine wave cycles.

Time cycles offer a compelling way to forecast market trends and time your trades better. By adding time cycles to your trading toolbox, you could potentially gain a new perspective on market movements and refine your trading strategy further. The indicator generates trading signals based on the sine wave's behavior. When the sine wave crosses certain thresholds, the indicator generates a signal suggesting a potential trading opportunity based on cycle behavior.

█ How to use

This indicator can be a valuable tool to help traders understand and predict market trends and time their trades more accurately. By visualizing the cyclic nature of markets, traders can better anticipate potential turning points and adjust their trading strategies accordingly. It helps traders to spot ideal entry and exit points based on the cyclical nature of financial markets.

█ Settings

You can customize the number of bars (NumbOfBars) that are taken into consideration for the cycle. Including a higher number of bars will provide more data, which can be helpful for analyzing long-term trends.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Adaptive Fisherized CMOIntroduction

Heyo, here is another no-repaint adaptive fisherized indicator.

I added Inverse Fisher Transform, Ehlers dominant cycle analysis and smoothing to the Chande Momentum Oscillator (CMO).

Usage

The CMO is a momentum oscillator which shows the usual movement of an asset.

I recommend to use it from a lower timeframe with a higher timeframe set.

Signals

(Signal mode will come soon.)

Zero Line

CMO crosses above zero line => enter long

CMO cross below zero line => ente short

Overbought/Oversold

CMO crosses above bottom band => enter long

CMO crosses under top band => enter short

MA (Maybe this signals will vary. Then, check update notes.)

CMO crosses above MA => enter long

CMO crosses below MA => enter short

Enjoy and share your experience with it!

More to read: CMO Explanationsp

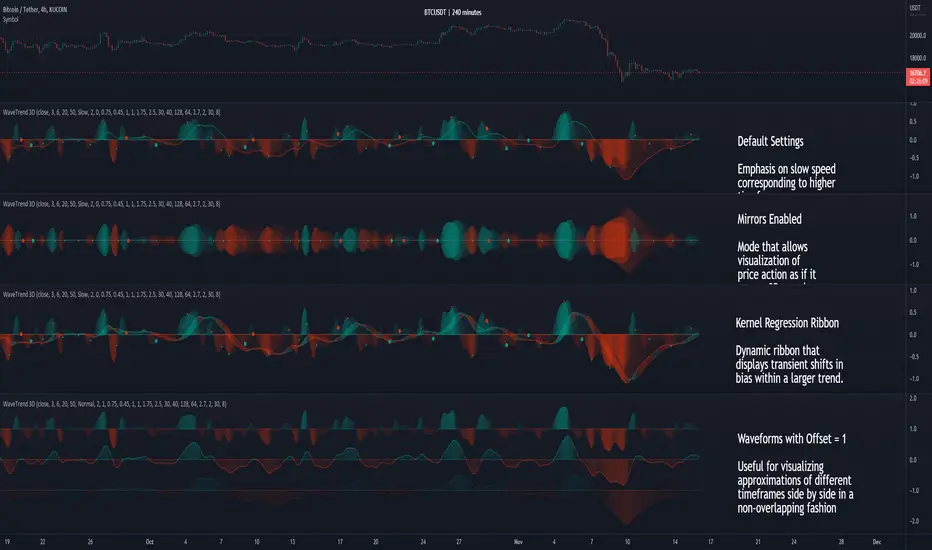

WaveTrend 3D█ OVERVIEW

WaveTrend 3D (WT3D) is a novel implementation of the famous WaveTrend (WT) indicator and has been completely redesigned from the ground up to address some of the inherent shortcomings associated with the traditional WT algorithm.

█ BACKGROUND

The WaveTrend (WT) indicator has become a widely popular tool for traders in recent years. WT was first ported to PineScript in 2014 by the user @LazyBear, and since then, it has ascended to become one of the Top 5 most popular scripts on TradingView.

The WT algorithm appears to have origins in a lesser-known proprietary algorithm called Trading Channel Index (TCI), created by AIQ Systems in 1986 as an integral part of their commercial software suite, TradingExpert Pro. The software’s reference manual states that “TCI identifies changes in price direction” and is “an adaptation of Donald R. Lambert’s Commodity Channel Index (CCI)”, which was introduced to the world six years earlier in 1980. Interestingly, a vestige of this early beginning can still be seen in the source code of LazyBear’s script, where the final EMA calculation is stored in an intermediate variable called “tci” in the code.

█ IMPLEMENTATION DETAILS

WaveTrend 3D is an alternative implementation of WaveTrend that directly addresses some of the known shortcomings of the indicator, including its unbounded extremes, susceptibility to whipsaw, and lack of insight into other timeframes.

In the canonical WT approach, an exponential moving average (EMA) for a given lookback window is used to assess the variability between price and two other EMAs relative to a second lookback window. Since the difference between the average price and its associated EMA is essentially unbounded, an arbitrary scaling factor of 0.015 is typically applied as a crude form of rescaling but still fails to capture 20-30% of values between the range of -100 to 100. Additionally, the trigger signal for the final EMA (i.e., TCI) crossover-based oscillator is a four-bar simple moving average (SMA), which further contributes to the net lag accumulated by the consecutive EMA calculations in the previous steps.

The core idea behind WT3D is to replace the EMA-based crossover system with modern Digital Signal Processing techniques. By assuming that price action adheres approximately to a Gaussian distribution, it is possible to sidestep the scaling nightmare associated with unbounded price differentials of the original WaveTrend method by focusing instead on the alteration of the underlying Probability Distribution Function (PDF) of the input series. Furthermore, using a signal processing filter such as a Butterworth Filter, we can eliminate the need for consecutive exponential moving averages along with the associated lag they bring.

Ideally, it is convenient to have the resulting probability distribution oscillate between the values of -1 and 1, with the zero line serving as a median. With this objective in mind, it is possible to borrow a common technique from the field of Machine Learning that uses a sigmoid-like activation function to transform our data set of interest. One such function is the hyperbolic tangent function (tanh), which is often used as an activation function in the hidden layers of neural networks due to its unique property of ensuring the values stay between -1 and 1. By taking the first-order derivative of our input series and normalizing it using the quadratic mean, the tanh function performs a high-quality redistribution of the input signal into the desired range of -1 to 1. Finally, using a dual-pole filter such as the Butterworth Filter popularized by John Ehlers, excessive market noise can be filtered out, leaving behind a crisp moving average with minimal lag.

Furthermore, WT3D expands upon the original functionality of WT by providing:

First-class support for multi-timeframe (MTF) analysis

Kernel-based regression for trend reversal confirmation

Various options for signal smoothing and transformation

A unique mode for visualizing an input series as a symmetrical, three-dimensional waveform useful for pattern identification and cycle-related analysis

█ SETTINGS

This is a summary of the settings used in the script listed in roughly the order in which they appear. By default, all default colors are from Google's TensorFlow framework and are considered to be colorblind safe.

Source: The input series. Usually, it is the close or average price, but it can be any series.

Use Mirror: Whether to display a mirror image of the source series; for visualizing the series as a 3D waveform similar to a soundwave.

Use EMA: Whether to use an exponential moving average of the input series.

EMA Length: The length of the exponential moving average.

Use COG: Whether to use the center of gravity of the input series.

COG Length: The length of the center of gravity.

Speed to Emphasize: The target speed to emphasize.

Width: The width of the emphasized line.

Display Kernel Moving Average: Whether to display the kernel moving average of the signal. Like PCA, an unsupervised Machine Learning technique whereby neighboring vectors are projected onto the Principal Component.

Display Kernel Signal: Whether to display the kernel estimator for the emphasized line. Like the Kernel MA, it can show underlying shifts in bias within a more significant trend by the colors reflected on the ribbon itself.

Show Oscillator Lines: Whether to show the oscillator lines.

Offset: The offset of the emphasized oscillator plots.

Fast Length: The length scale factor for the fast oscillator.

Fast Smoothing: The smoothing scale factor for the fast oscillator.

Normal Length: The length scale factor for the normal oscillator.

Normal Smoothing: The smoothing scale factor for the normal frequency.

Slow Length: The length scale factor for the slow oscillator.

Slow Smoothing: The smoothing scale factor for the slow frequency.

Divergence Threshold: The number of bars for the divergence to be considered significant.

Trigger Wave Percent Size: How big the current wave should be relative to the previous wave.

Background Area Transparency Factor: Transparency factor for the background area.

Foreground Area Transparency Factor: Transparency factor for the foreground area.

Background Line Transparency Factor: Transparency factor for the background line.

Foreground Line Transparency Factor: Transparency factor for the foreground line.

Custom Transparency: Transparency of the custom colors.

Total Gradient Steps: The maximum amount of steps supported for a gradient calculation is 256.

Fast Bullish Color: The color of the fast bullish line.

Normal Bullish Color: The color of the normal bullish line.

Slow Bullish Color: The color of the slow bullish line.

Fast Bearish Color: The color of the fast bearish line.

Normal Bearish Color: The color of the normal bearish line.

Slow Bearish Color: The color of the slow bearish line.

Bullish Divergence Signals: The color of the bullish divergence signals.

Bearish Divergence Signals: The color of the bearish divergence signals.

█ ACKNOWLEDGEMENTS

@LazyBear - For authoring the original WaveTrend port on TradingView

@PineCoders - For the beautiful color gradient framework used in this indicator

@veryfid - For the inspiration of using mirrored signals for cycle analysis and using multiple lookback windows as proxies for other timeframes

Tesla Coil MLThis is a re-implementation of @veryfid's wonderful Tesla Coil indicator to leverage basic Machine Learning Algorithms to help classify coil crossovers. The original Tesla Coil indicator requires extensive training and practice for the user to develop adequate intuition to interpret coil crossovers. The goal for this version is to help the user understand the underlying logic of the Tesla Coil indicator and provide a more intuitive way to interpret the indicator. The signals should be interpreted as suggestions rather than as a hard-coded set of rules.

NOTE: Please do NOT trade off the signals blindly. Always try to use your own intuition for understanding the coils and check for confluence with other indicators before initiating a trade.

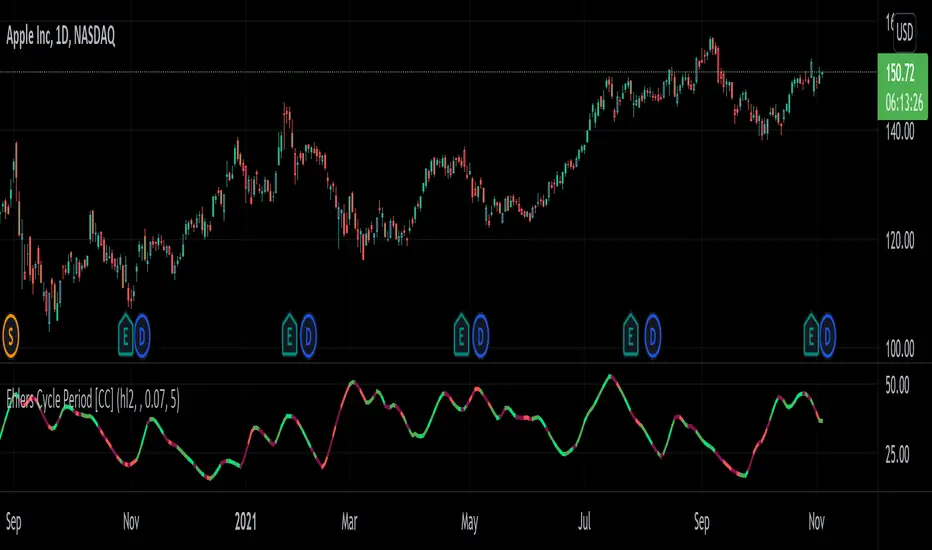

Ehlers Cycle Period [CC]The Cycle Period was created by John Ehlers and this is yet another version that shows how to calculate the current cycle period which is the approximate amount of days between a current peak or valley and the next peak or valley. I would not recommend this for trading since it is more for informational use only but I would try experimenting with this output to be used with another indicator as an input length. I have included strong buy and sell signals in addition to normal ones so strong signals are darker in color and normal signals are lighter in color.

Let me know if there are any other scripts you would like to see me publish!

Ehlers Mesa Spectrum Dominant Cycle [CC]The Mesa Spectrum Dominant Cycle was created by John Ehlers and this is the foundation for many indicators he created that would later follow. This is his updated version of his original Mesa algorithm and I do not recommend this indicator as a stand alone for trading. This is more of an informational indicator that will tell you the current dominant cycle period which is the approximate period between peaks and valleys in the underlying data. I have color coded buy signals just in case with both strong and normal signals. Darker colors are strong and lighter colors are normal. Buy when the line is green and sell when it is red.

Let me know if there are any other indicators you would like to see me publish!

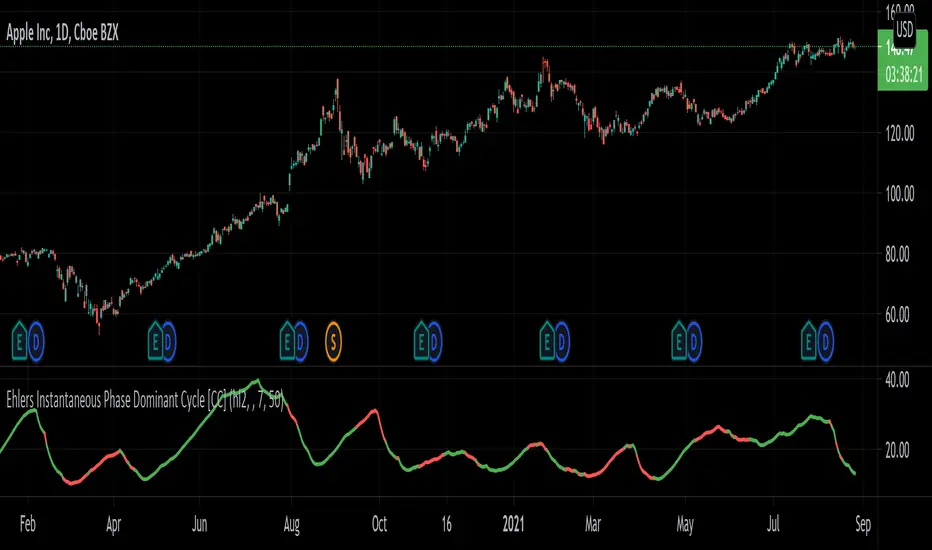

Ehlers Instantaneous Phase Dominant Cycle [CC]The Instantaneous Phase Dominant Cycle was created by John Ehlers (Stocks & Commodities V. 18:3 (16-27)) and this is one of many similar indicators that I will be publishing from Ehlers in the next few months that calculate the current dominant cycle period. The cycle period can be used in multiple ways but generally this means that if the stock is currently at a low then the current cycle period will tell you when the next lowest low will get hit or vice versa. This is also useful for using this cycle period as an input for other indicators to provide a very good adaptive length. Let me know how you wind up using these indicators in your daily trading. I have included the same buy and sell signals from my recent Hilbert Transform and so buy when the line turns green and sell when it turns red.

Let me know if there are any other indicators you would like to see me publish!

Financial Astrology Juno LongitudeJuno is the 4th largest object in terms of mass in the asteroid belt between Mars and Jupiter, this asteroid is not widely used by financial astrologers but as was demonstrated in our research with Ceres and Vesta, the objects in the asteroid belt seems to be very important for the trend forecast. The zodiacal energy of this objects cannot be ignored for an accurate analysis. Based in BTCUSD historical price data we calculated the daily trend (buy/sell) during the periods where Juno was transiting across different zodiac signs and we found some significant patterns:

INDEX:BTCUSD

Bullish zodiac signs

From 387 days located in Scorpio, price increased 62% of the days.

From 316 days located in Capricorn, price increased 64% of the days.

From 300 days located in Sagittarius, price increased 56% of the days.

From 435 days located in Libra, price increased 55% of the days.

Bearish zodiac signs

From 200 days located in Taurus, price decreased 56% of the days.

From 152 days located in Virgo, price decreased 58% of the days.

Note: The Juno longitude indicator is based on an ephemeris array that covers years 2010 to 2030, prior or after this years the data is not available, this daily ephemeris are based on UTC time so in order to align properly with the price bars times you should set UTC as your chart timezone.

Fast Fourier Transform (FFT) FilterDear friends!

I'm happy to present an implementation of the Fast Fourier Transform (FFT) algorithm. The script uses the FFT procedure to decompose the input time series into its cyclical constituents, in other words, its frequency components , and convert it back to the time domain with modified frequency content, that is, to filter it.

Input Description and Usage

Source and Length :

Indicates where the data comes from and the size of the lookback window used to build the dataset.

Standardize Input Dataset :

If enabled, the dataset is preprocessed by subtracting its mean and normalizing the result by the standard deviation, which is sometimes useful when analyzing seasonalities. This procedure is not recommended when using the FFT filter for smoothing (see below), as it will not preserve the average of the dataset.

Show Frequency-Domain Power Spectrum :

When enabled, the results of Fourier analysis (for the last price bar!) are plotted as a frequency-domain power spectrum , where “power” is a measure of the significance of the component in the dataset. In the spectrum, lower frequencies (longer cycles) are on the right, higher frequencies are on the left. The graph does not display the 0th component, which contains only information about the mean value. Frequency components that are allowed to pass through the filter (see below) are highlighted in magenta .

Dominant Cycles, Rows :

If this option is activated, the periods and relative powers of several dominant cyclical components that is, those that have a higher power, are listed in the table. The number of the component in the power spectrum (N) is shown in the first column. The number of rows in the table is defined by the user.

Show Inverse Fourier Transform (Filtered) :

When enabled, the reconstructed and filtered time-domain dataset (for the last price bar!) is displayed.

Apply FFT Filter in a Moving Window :

When enabled, the FFT filter with the same parameters is applied to each bar. The last data point of the reconstructed and filtered dataset is used to build a new time series. For example, by getting rid of high-frequency noise, the FFT filter can make the data smoother. By removing slowly evolving low-frequency components (including non-periodic constituents), one can reveal and analyze shorter cycles. Since filtering is done in real-time in a moving window (similar to the moving average), the modified data can potentially be used as part of a strategy and be subjected to other technical indicators.

Lowest Allowed N :

Indicates the number of the lowest frequency component used in the reconstructed time series.

Highest Allowed N :

Indicates the number of the highest frequency component used in the reconstructed time series.

Filtering Time Range block:

Specifies the time range over which real-time FFT filtering is applied. The reason for the presence of this block is that the FFT procedure is relatively computationally intensive. Therefore, the script execution may encounter the time limit imposed by TradingView when all historical bars are processed.

As always, I look forward to your feedback!

Also, leave a comment if you'd be interested in the tutorial on how to use this tool and/or in seeing the FFT filter in a strategy.

Financial Astrology Vesta SpeedVesta (asteroid) speed provides a good indicator to determine the periods of dominant trend. During the direct phase (when the speed accelerated and reached highest value) we can observe that BTCUSD experienced a clear trend, perfect for trend following. In the contrary when speed was decelerating and speed started backward motion (retrograde) the price was in congestion experiencing sideways moves. From statistical analysis we noted that when Vesta speed is in direct motion 56% of the days resulted in price increase. When speed was stationary (starting to move retrograde) we observed that in 62% of the days the price decreased, finally, during retrograde phase in 54% of the days the price increased. Is clear that direct motion also offers more bullish days. However, in the statistical analysis of the price is not evident the price change range, with visual exploration in the chart is clear that when Vesta speed is in direct phase the range of the price is wider, therefore, direct motion provides the most interesting risk/reward ratio.

Note: The Vesta speed indicator is based on an ephemeris array that covers years 2010 to 2030, prior or after this years the data is not available, this daily ephemeris are based on UTC time so in order to align properly with the price bars times you should set UTC as your chart timezone.

Financial Astrology Vesta DeclinationVesta (asteroid) declination show a strong correlation with the BTCUSD trend, we can clearly see that all the most intense bullish periods have occurred when declination was moving from South to Node direction (when the slope is positive). In the events when declination was moving toward North and have penetrated the zero declination boundary (horizontal dashed line) we can observe a periods where price experienced more volatility.

Note: The Vesta declination indicator is based on an ephemeris array that covers years 2010 to 2030, prior or after this years the data is not available, this daily ephemeris are based on UTC time so in order to align properly with the price bars times you should set UTC as your chart timezone.

Financial Astrology True Lilith (Black Moon) LongitudeTrue Lilith (Black Moon) represents the wildly perturbed Moon apogee orbit, is not averaged (as Mean Lilith) and shows an erratic path with constant change of direction and speed. This Lilith uses the actual, real orbit rather than the average used by Mean Lilith. This perturbations are caused due to the gravitational pull of the Sun and the change of the orbit center which is the Earth-Moon Barycenter. The move of this apogee point toward all the Zodiac signs takes around 9 years to complete and as we can observe, the True Lilith moves back and forward within two consecutive zodiac signs during a prolonged period. In this erratic motion we can note that the peaks and valleys of this waves usually present a swing trade opportunities, is really impressive to note how a full or half True Lilith wave period correlates with short term local peaks and valleys in the BTCUSD price.

Note: The True Lilith (Black Moon) longitude indicator is based on an ephemeris array that covers years 2010 to 2030, prior or after this years the data is not available, this daily ephemeris are based on UTC time so in order to align properly with the price bars times you should set UTC as your chart timezone.

Financial Astrology Mean Lilith (Black Moon) LongitudeMean Lilith (Black Moon) represents the apogee of the lunar orbit (point where the Moon is farthest from Earth) as the Moon experience perturbations due to the gravitational pull of the Sun and don't orbit in elliptical path due the fact that don't follow the Earth center but the Earth-Moon Barycenter cause that an average projection of this apogee point location needs to be calculated, for this reason, we need to differentiate the Mean Lilith and True Lilith. The move of this apogee point toward all the Zodiac signs takes around 9 years to complete so in BTCUSD asset we only have one complete revolution so is difficult to emit any clear judgement of the zodiac sign location influence in the trend. However this imaginary body named Lilith is widely adopted by astrologers and is very important in Chinese Astrology, for this reason, we decided to contribute the indicator to support the research of Chinese astro-traders.

Note: The Mean Lilith (Black Moon) longitude indicator is based on an ephemeris array that covers years 2010 to 2030, prior or after this years the data is not available, this daily ephemeris are based on UTC time so in order to align properly with the price bars times you should set UTC as your chart timezone.

Financial Astrology North Node (Rahu) LongitudeThe Moon Nodes are the points where Moon crosses the ecliptic and transition from North to South latitude, North Node (Rahu) in Vedic astrology is considered to cause a bull trend when Eclipse occurs at this Moon node. Moon nodes are important because when Moon and Sun are in conjunction or opposition close very close to the degree of a Moon Node, then a Solar or Lunar eclipse occurs.

The effect of the trend will be coloured by the Zodiac sign where the Moon Node is located at, based on statistical research we have noted that the periods where North Node (Rahu) was located in Geminis the 56% of days was bullish, in Virgo 62% of the days was bullish. The most bearish location was Libra with 51% of days bearish. However the transition of North Node around all the Zodiac takes 19 years so in all BTCUSD price history we don't have yet a complete revolution to have a complete understanding of all the energy frequencies.

Note: The North Node (Rahu) longitude indicator is based on an ephemeris array that covers years 2010 to 2030, prior or after this years the data is not available, this daily ephemeris are based on UTC time so in order to align properly with the price bars times you should set UTC as your chart timezone.