Quantitative Price Forecasting - The Quant ScienceThis script is a quantitative price forecasting indicator that forecasts price changes for a given asset.

The model aims to forecast future prices by analyzing past data within a selected time period. Mathematical probability is used to calculate whether starting from time X can lead to reaching prices Y1 and Y2. In this context, X represents the current selected time period, Y1 represents the selected percentage decrease, and Y2 represents the selected percentage increase. The probabilities are estimated using the simple average.

The simple average is displayed on the chart, showing in red the periods where the price is below the average and in green the periods where the price is above the average.

This powerful tool not only provides forecasts of future prices but also calculates the distribution of variations around the average. It then takes this information and creates an estimate of the average price variation around the simple average.

Using a mean-reverting logic, buying and selling opportunities are highlighted.

We recommend turning off the display of bars on your chart for a better experience when using this indicator.

Unlock the full potential of your trading strategy with our powerful indicator. By analyzing past price data, it provides accurate forecasts and calculates the probability of reaching specific price targets. Its mean-reverting logic highlights buying and selling opportunities, while the simple moving average displayed on the chart shows periods where the price is above or below the average. Additionally, it estimates the average variation of price around the simple average, giving you valuable insights into price movements. Don't miss out on this valuable tool that can take your trading to the next level

Statistics

Intrabar Analyzer [Kioseff Trading]Hello!

This indicator (Intrabar Analyzer) presents intrabar data in various derivative forms.

On-Chart Features

Traditional price data down to 1 min.

Heikin-Ashi price data down to 1 min.

Kagi price data down to 1 min.

Point & Figure price data down to 1 min.

Renko price data down to 1 min.

Linebreak price data down to 1 min.

LinReg channel

SMA

EMA

ALMA

Echomorphic Average (A @kaigouthro special!)

HMA

RMA

WMA

VWMA

VWAP

SWMA

SAR

Supertrend

On-Chart Features

Price x Volume graph

Intrabar technical rating

Positive volume index

Negative volume index

Price volume trend

RSI

%k

ROC

MFI

MFC

OBV

CCI

BBW

CMO

COG

KCW

MOM

RANGE

%r

Let's look at the objects populated by the indicator!

The image above shows what data correlates to the populated graphs!

Let's dial in on the price x volume graph.

The image above provides an example/explanation of the price x volume graph. All data is sourced from a lower timeframe (configurable - default = 1 minute).

Colors are configurable; the plot characters are configurable.

The numbers above show an alternative view of the price x volume graph!

Price graph

The price graph can populate 6 variations of price data: traditional, heikin-ashi, renko, point & figure, line break, and kagi.

The subsequent images will show all available forms of price data, in addition to a randomly selected, on-chart technical indicator!

Kagi + LinReg

Traditional + EMA

Renko + SAR

Point & Figure + ALMA

Heikin-Ashi + Supertrend

Line Break + VWAP

You can display up to three indicators concomitantly - all calculated using intrabar data!

Lastly, the indicator displays the TradingView calculated technical rating for the intrabar.

The technical ratings are multiplied by x100 and oriented left & right of the price box. Left values are negative; right values are positive. The "0" value is not shown; therefore, if the technical rating isn't highlighted then the rating is "0".

The image above shows the technical rating system in action (:

That's it!

This was a fun project and I'm certainly willing to add more - let me know if there's anything you'd like included.

Additionally, a future feature involves compatibility with any custom indicator! Stay tuned; thank you for checking this out (:

Thank you to @kaigouthro, TradingView and @PineCoders for providing some cool libraries to play with!

Weekday Change & Volume Average TableHaving a reference point for comparing with current data has always been an important task in market analysis. This script tried to give a better understanding based on weekdays.

This script shows that in the current ticker, what is the average movement of the price (High-Low) and volume for each weekday. Depending on the market and the exchange it should be different.

The Interesting point is that, for example in BINANCE:BTCUSDT , on Saturday and Sunday, volume is about 30% less and the price movement is about 20% less.

The script can be used on any timeframe and any symbol, just remember that the data shown is based on the candles on the chart, so it is different also based on your tradingview's account since Historical bars available for Basic is 5K, Pro & Pro+ is 10K and Premium is 20K; And in lower timeframes it is calculating more recent data.

BTC Performance Table / BTC Seasonality Visualization

This script visualizes Bitcoins "seasonality", in form of a colored table (based on the idea from "BigBangTheory")

The history table shows you which months do statistically perform better/worse in comparison to other months.

How to use this script:

Choose ticker "BLX" ("BraveNewCoin Liquid Index for Bitcoin").

Set the charts time frame to weekly or daily. Tables position on the screen and its colors are configurable.

Table explanation:

Cells show whether a gain or a loss occured from month to month, since BTC came out in 2010.

The price difference, between monthly open and monthly close, determines the cell color (negative -> red, positive -> green).

The year column shows total gain (green) or loss (red) for that particular year.

Each value is presented as a rounded percentage number.

How this script works:

The script calculates the price difference between each monthly and yearly open and close, storing those numbers inside arrays.

Then it populates the table, by using those numbers and doing the cell coloring (there will be a yellow cell, in case no change should occur).

German Short-Description

Prozentuale Übersicht in Tabellenform, der monatlichen, sowie jährlichen, Performance des Bitcoin (basierend auf der Idee von "BigBangTheory").

Hierdurch wird die "Saisonalität" des Bitcoin sichtbar. D.h. welche Monate des Jahres, im Vergleich zu anderen Monaten, statistisch gesehen öfter positiv/negativ schließen.

Zwecks vollständiger Darstellung muss der Ticker "BLX" ("BraveNewCoin Liquid Index for Bitcoin") im weekly oder daily time frame aktiv sein.

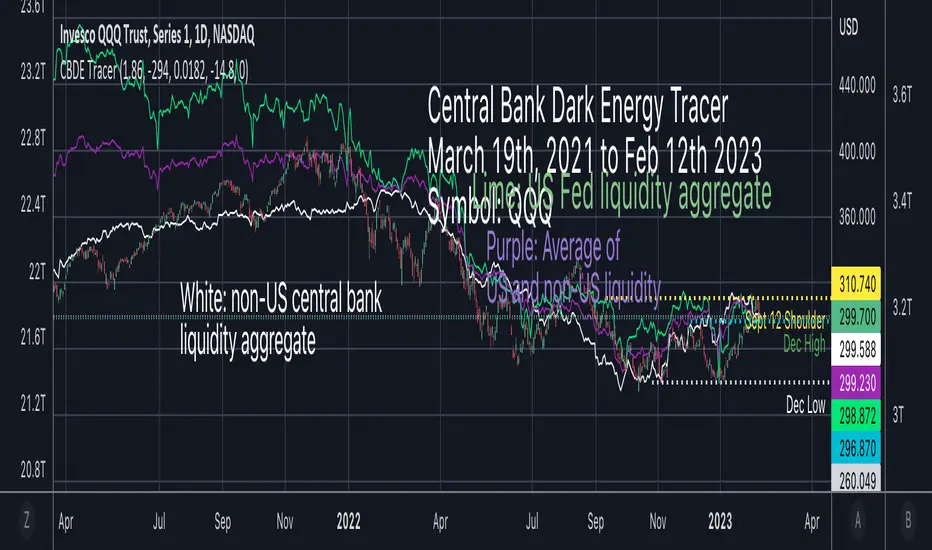

Central Bank Dark Energy TracerCentral Bank Dark Energy Tracer (CBDE Tracer)

What makes The Universe grow at an accelerating pace?

Dark Energy.

What makes The Economy grow at an accelerating pace?

Debt.

Debt is the Dark Energy of The Economy.

The CBDE Tracer is a tool that tracks currency assets in US dollars that can be scaled to fit other assets on TradingView.

The example provided is QQQ with scale factors and offsets applied that best curve fit to the most recent price action.

The white line is non-US assets from the following central banks:

-JPY (Japan)

-CNY (China)

-UK (British Pound)

-SNB (Swiss National Bank)

-ECB (European Central Bank )

The lime green line is for US Federal Reserve data including a midpoint of WRESBAL and the fed liquidity calculation (WALCL - WTREGEN) and then subtracting RRPONTSYD

The purple line is the average of the two, US assets, and non-US.

The settings can be configured so that only the average is showing, which should the closest aggregate of all liquidity data.

TICK - Custom Tickers [Pt]Traditionally, the TICK index is a technical analysis indicator that shows the difference in the number of stocks that are trading on an uptick vs a downtick in a particular period of time. This indicator allows user to choose up to 40 tickers to calculate TICK.

By default, it uses the SPY Top 40 stocks, but can be changed to any tickers.

There are options to show:

- Top 7 , ie. can be used for just showing TICK for FAANGMT => $FB + $AMZN + $AAPL + $NFLX + $GOOG + $MSFT + $TSLA

- Top 10

- Top 20

- Top 30

- Top 40

Data can be displayed in candle bars, line, or both.

Enjoy~

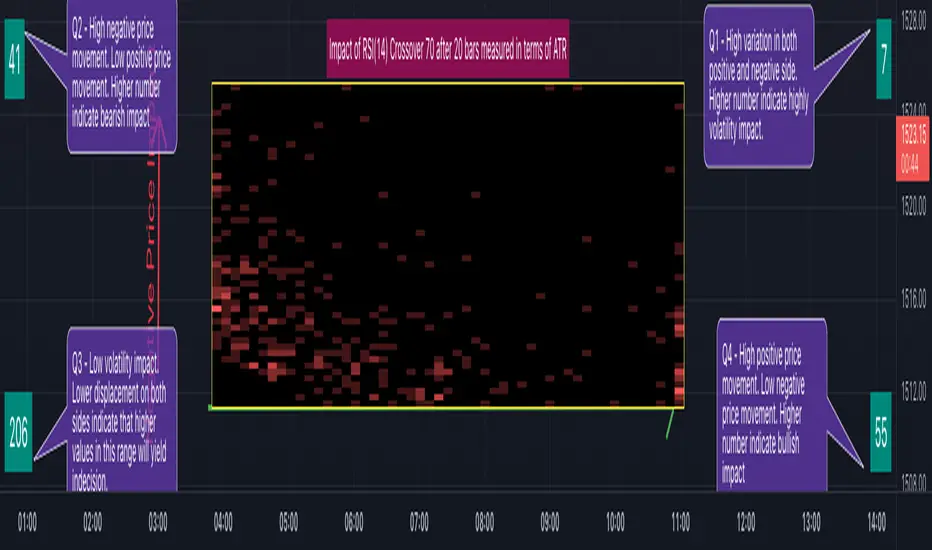

RSI Impact Heat Map [Trendoscope]Here is a simple tool to measure and display outcome of certain RSI event over heat map.

🎲 Process

🎯Event

Event can be either Crossover or Crossunder of RSI on certain value.

🎯Measuring Impact

Impact of the event after N number of bars is measured in terms of highest and lowest displacement from the last close price. Impact can be collected as either number of times of ATR or percentage of price. Impact for each trigger is recorded separately and stored in array of custom type.

🎯Plotting Heat Map

Heat map is displayed using pine tables. Users can select heat map size - which can vary from 10 to 90. Selecting optimal size is important in order to get right interpretation of data. Having higher number of cells can give more granular data. But, chart may not fit into the window. Having lower size means, stats are combined together to get less granular data which may not give right picture of the results. Default value for size is 50 - meaning data is displayed in 51X51 cells.

Range of the heat map is adjusted automatically based on min and max value of the displacement. In order to filter out or merge extreme values, range is calculated based on certain percentile of the values. This will avoid displaying lots of empty cells which can obscure the actual impact.

🎲 Settings

Settings allow users to define their event, impact duration and reference, and few display related properties. The description of these parameters are as below:

🎲 Use Cases

In this script, we have taken RSI as an example to measure impact. But, we can do this for any event. This can be price crossing over/under upper/lower bollinger bands, moving average crossovers or even complex entry or exit conditions. Overall, we can use this to plot and evaluate our trade criteria.

🎲 Interpretation

Q1 - If more coloured dots appear on the top right corner of the table, then the event is considered to trigger high volatility and high risk environment.

Q2 - If more coloured dots appear on the top left corner, then the events are considered to trigger bearish environment.

Q3 - If more coloured dots appear on the bottom left corner of the chart, then the events are considered insignificant as they neither generate higher displacement in positive or negative side. You can further alter outlier percentage to reduce the bracket and hence have higher distribution move towards

Q4 - If more coloured dots appear on the bottom right corner, then the events are considered to trigger bullish environment.

Will also look forward to implement this as library so that any conditions or events can be plugged into it.

Historical Federal Fund Futures CurveUse this indicator to plot the federal funds futures implied rates term structure against historical curves

Based upon the work of @BarefootJoey, @longfiat, @OpptionsOnly

BTC / DXY, BTC / US10Y

The combination of the DXY and US02Y can be used to gauge market sentiment and assess the state of the global economy.

When the DXY is rising, it indicates that the U.S. dollar is strengthening relative to other currencies, which can lead to increased risk aversion among investors as the U.S. dollar is often seen as a safe-haven currency.

When the US02Y is rising, it suggests that market expectations for future inflation and interest rate increases are increasing, which can lead to a decrease in the value of riskier assets such as stocks.

In general, the combination of the DXY and US02Y can provide important information on the direction of global market trends and the state of the economy, and as such, they are important indicators to consider when making investment decisions.

RISK MANAGEMENTHi dear Traders,

Here I would present you my 'Risk Management' tool which is based on your buy orders, trading fees and your desired benefit.

Easily, fulfill the price and volume of each entries. Add to this, you can prepare the info about your next proposed entries, just let them not check at first and by meeting the prices then active the check-box beside it.

Two line will be presented on your candle-plot, one of the indicate the place that without any lose/win you can exit and also the desired exit position by considering user defined benefit.

Use it for free but please do not forget to boost the script.

Best regards and happy trading.

Shakib

Liquidation_linesLibrary "Liquidationline"

f_calculateLeverage(_leverage, _maintainance, _value, _direction)

Parameters:

_leverage

_maintainance

_value

_direction

f_liqline_update(_Liqui_Line, _killonlowhigh)

Parameters:

_Liqui_Line

_killonlowhigh

f_liqline_draw(_Liqui_Line, _priceorliq)

Parameters:

_Liqui_Line

_priceorliq

f_liqline_add(_Liqui_Line, linetoadd, _limit)

Parameters:

_Liqui_Line

linetoadd

_limit

Liquidationline

Fields:

creationtime

stoptime

price

leverage

maintainance

line_active

line_color

line_thickness

line_style

line_direction

line_finished

text_active

text_size

text_color

this library can draw typical liquidation lines, which can be called e.g. by indicator signals

You can see the default implementation in the lower part of the code, starting with RUNTIME

Don't forget to increase max lines to 500 in your script.

It can look like this screenshot here, with only minor changes to your executing script.

The base is the same

Global LiquidityPlots the sum of the balance sheets of the world's major central banks - FED, ECB, BoE, PBoC, BOJ, India and Switzerland - in a currency of your choice. Defaults to USD.

Also shows FED net liquidity (balance sheet - tga - rrp) for comparison. Uses a configurable multiplier to make the two lines viewable on the same price scale.

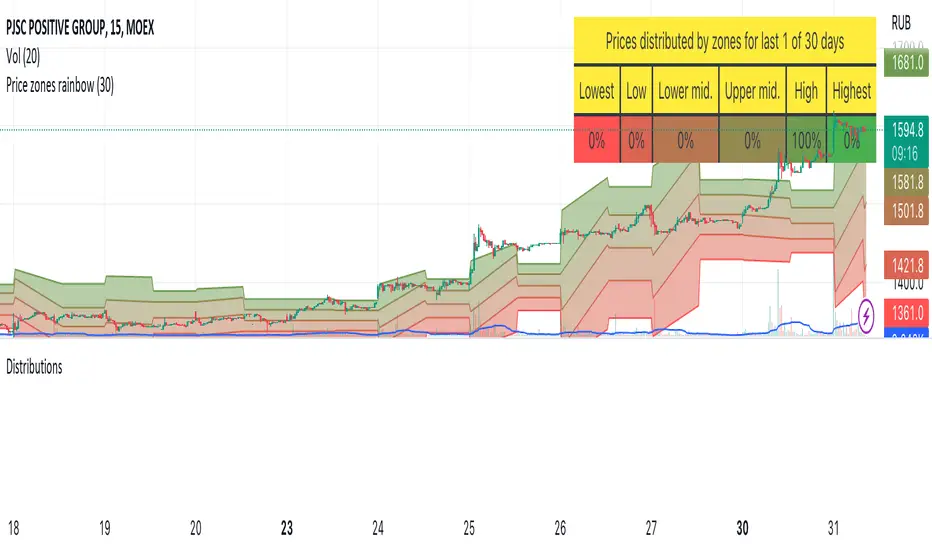

DistributionsLibrary "Distributions"

Library with price distribution zones calculation helpers.

Based on research from "Trading Systems and Methods, 5th Edition" by Perry J. Kaufman

getZones(h, l, c, window)

Returns price distribution zones based on HLC and for some period

Parameters:

h : high price

l : low price

c : close price

window : period to calculate distributions

Returns: tuple of 5 price zones in descent order, from highest to lowest

Balance of Force Day of the Week (BOFDW)The script is a custom technical indicator for TradingView that is based on an analysis of the price movements of a financial instrument over the course of a week. The indicator uses a variety of inputs, including the open and close prices for each day of the week, to determine the "BOF" (BOF) for each day.

The BOF is calculated based on the relative magnitude of bullish and bearish price movements and is then used to determine the average BOF over a moving window of data points. This average BOF is displayed on the chart as an overlay, providing a measure of the average bullishness or bearishness of the financial instrument over the course of a week.

The indicator also allows users to specify the location of the overlay on the chart and to customize the appearance of the overlay with options for text and box colors. The script provides a number of built-in options for chart position, including the top-left, top-middle, top-right, middle-left, middle-center, middle-right, bottom-left, bottom-middle, and bottom-right corners of the chart.

Overall, this custom technical indicator is a useful tool for traders and investors who are looking to gain a deeper understanding of the price trends of a financial instrument over the course of a week. By providing a clear and concise measure of the average POF over time, the indicator can help users identify key patterns in the market and make more informed trading decisions.

PerformanceTableLibrary "PerformanceTable"

TODO: add library description here

This library was created as a library because adding a performance table to an existing strategy script made the strategy script lengthy and inconvenient to manage.

The monthly table script referenced @QuantNomad's code.

The performance table script referenced @myncrypto's code.

To use, copy and paste the code below at the bottom of the strategy script you are using, and the table for strategy performance will be displayed on a chart.

//------------Copy & Paste --------------------------------------//

import Cube_Lee/PerformanceTable/1 as PT

PT = input.bool(true, "Show Performance Table", tooltip = "전략의 성과를 우측상단에 테이블로 표시합니다.", group = "Performance Table")

MT = input.bool(true, "Show Monthly Table", tooltip = "전략의 월별 수익률을 우측하단에 테이블로 표시합니다.", group = "Performance Table")

if PT

PT.PerformanceTable()

if MT

PT.MonthlyTable()

//------------Copy & Paste---------------------------------------//

PerformanceTable()

MonthlyTable()

VIX OscillatorThis is my VIX Oscillator indicator.

About it:

This indicator takes the Z-Score of the VIX and of the current ticker you are on and presents them in the format of an oscillator.

Key parts of the indicator:

A diagram of the key elements of the indicator are displayed above.

Purple Line: Represents the Z-Score of the current Ticker.

Blue Line: Represents the Z-Score of the VIX

Green fill line: Represents bullish divergence

Red fill line: Represents bearish divergence

How to use it:

Characteristics for long entries:

- Look for recent bullish divergence (green fill line)

- Look for the ticker line (purple line) to be holding above 0 (neutrality)

- look for a bullish cross (purple line (ticker) crossing over blue line (VIX))

Characteristics for short entries:

- Look for recent Bearish divergence

- Look for the VIX line (blue line) to be holding above 0 and the Ticker

- Look for the ticker line to be holding below 0

- Look for a bearish cross (blue crossing above purple)

Some principles:

The bands represent oversold, overbought and neutral.

0 is absolute neutrality. No bias here.

Anything towards + 2.5 is considered normal, moving towards overbought (2.5 or higher).

Anything towards -2.5 is considered normal, moving towards oversold (-2.5 or lower).

+2.5 or higher is overbought.

-2.5 or lower is oversold.

As always, I have prepared a quick tutorial video for your reference of this indicator:

Please let me know your questions, comments or suggestions about this indicator below.

Thank you for checking it out!