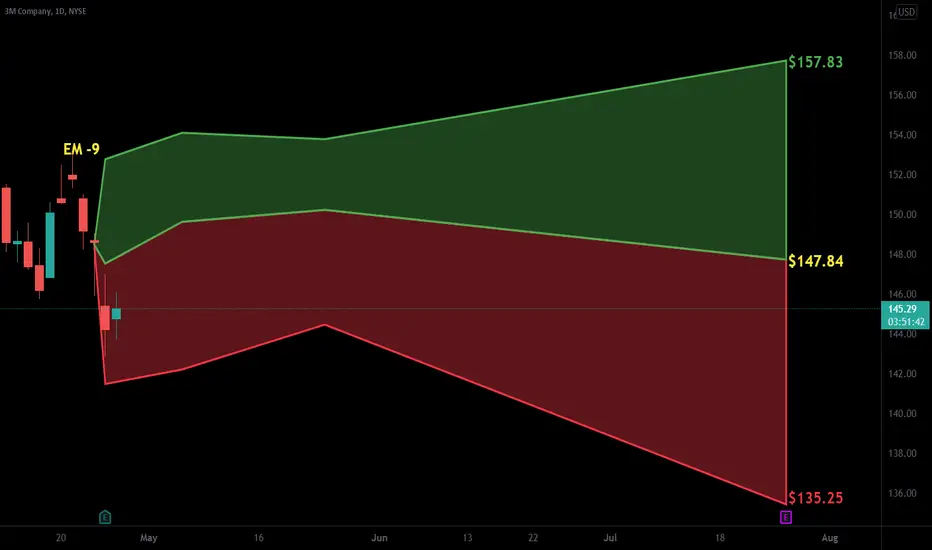

$MMM with a Bearish outlook following its earnings #Stocks The PEAD projected a Bearish outlook for $MMM after a Negative over reaction following its earnings release placing the stock in drift B .

MMM trade ideas

MMM SELL +Earnings spike caused overbought indicators on several time frames and charts, high stochastics, high daily rsi, bollinger bands pierced, gap to fill with cloud resistance. Looking for small scalp. Bought puts this morning around $144 range. Bought August 19 $142 puts. Traders should be wary of buying bear market rallies most stocks today will be lower in a few months. GL

$MMM Longterm Investing OpportunityIs 3M currently a good Stock for a Dividendportfolio? NYSE:MMM

$MMM is coming closer to a level where it's getting interesting for buy opportunities. The overall structure is still bullish on the monthly as well as on the weekly. The orderflow on the weekly is currently corrective as price is inside a very clean pullback (PB)

The stock has been consolidating for the last weeks, which is a good sign because it is building liquidity on the bottom side, which we expect to get taken out before continuing to the upside.

So from the technical side, we can start ticking the boxes if price sweeps the Liquidity that it is currently building up.

From a fundamental perspective, 3M is getting closer to the fair value price, which is an additional confluence for me to open up long-term positions. It will be a good fit for my Dividendportfolio.

I'll make an update if the stock makes significant changes in pricing.

3M A good location to shortHello everyone,

Today i want to share which you my idea on 3M.

The structure of the price look verry bearish, and now the price try to bounce on the previous structure and get rejected.

So we have a good location for a short entry.

The target is on the previous support, and close to an AB CD.

For the more greedy of us, you can try to entry at 176.57

3M Company (NYSE: $MMM) Trading Near Multi-Year Lows ⭐3M Company operates as a diversified technology company worldwide. It operates through four segments: Safety and Industrial; Transportation and Electronics; Health Care; and Consumer. The Safety and Industrial segment offers industrial abrasives and finishing for metalworking applications; autobody repair solutions; closure systems for personal hygiene products, masking, and packaging materials; electrical products and materials for construction and maintenance, power distribution, and electrical original equipment manufacturers; structural adhesives and tapes; respiratory, hearing, eye, and fall protection solutions; and natural and color-coated mineral granules for shingles. The Transportation and Electronics segment provides ceramic solutions; attachment tapes, films, sound, and temperature management for transportation vehicles; premium large format graphic films for advertising and fleet signage; light management films and electronics assembly solutions; packaging and interconnection solutions; and reflective signage for highway, and vehicle safety. The Healthcare segment offers food safety indicator solutions; health care procedure coding and reimbursement software; skin, wound care, and infection prevention products and solutions; dentistry and orthodontia solutions; and filtration and purification systems. The Consumer segment provides consumer bandages, braces, supports and consumer respirators; cleaning products for the home; retail abrasives, paint accessories, car care DIY products, picture hanging, and consumer air quality solutions; and stationery products. It offers its products through e-commerce and traditional wholesalers, retailers, jobbers, distributors, and dealers. The company was founded in 1902 and is based in St. Paul, Minnesota.

MMM Swing Ideamulti-month consolidation with MMM - ranges tightening, and with markets looking like a potential bottom has occurred (even if temporary) we may find enough gusto to break out.

Targeting approx 167+

starter position in October calls, looking for 155+ for size.

Obviously, this is not trading advice, just personal journaling of thoughts at this time with the information/candlesticks & indicators available.

This won't be one I follow closely - moreso one where we just set some alerts for 153, 155+ and ignore it until we hear that *ding*

Time to buy!Hi everyone, Yurii Domaranskyi here. Let's take a look at the chart:

1. Price levels are working good here

2. globally downtrend

3. no report in the following 2 weeks

4. approached with a big bar

5. way down with rollbacks

6. level of a rollback

7. enough room for a move 1 to 5.1 risk/reward

8. yesterday good news "3M guides for 1%-4% sales growth in 2022, in line with estimates"

9. the price came from above

Potential risk/reward ratio = 1 to 5.1 meaning that potential risk 100$ with the possibility to make 510$

If it does make sense to you, press a thumb up! 👍

3M | Fundamental AnalysisThe continued poor performance of 3M stock indicates that investors are beginning to lose patience with the company. At the last investor presentation, management resigned from the full-year outlook it gave at the end of October. Thus, the company's stock is even falling out of favor with value-oriented investors and increasingly evolving an option only for dividend investors.

Let's take a closer look at what's going on and whether 3M has investment potential.

In early December, MMM CEO Mike Roman and CFO Monish Patolawala spoke at the Credit Suisse Industrial Companies Conference. They immediately told investors that organic sales growth in Q4 would be in the "lower half" of the expected growth range of zero to negative 2%.

When a company lowers its sales estimates, it's never good news, but the update from 3M particularly disappointed investors. There are three reasons for this:

First, the lower sales forecast came after management raised its full-year organic sales growth forecast in late October during its Q3 earnings presentation. In the third quarter, full-year organic sales growth was between 6% and 9%, but management noticed fit to increase the lower end of the range to 8%-9%, even as the full-year profit forecast was lowered to $9.70-$9.90 from $9.70 to $10.10.

Considering that the assumed outlook for the fourth quarter has been lowered, investors are justifiably lowering earnings growth expectations. It also begs the question of why Patolawala decreased anticipations weeks after increasing them.

Second, it's no secret that investors are watching 3M's margins closely for clues as to whether its restructuring measures are bringing operational improvements. Of course, it's much harder to judge this during a pandemic, but Patolawala has previously noted the significance of volume gain to 3M's margins. Given that sales growth will be weaker than expected, 3M's margins are likely to come under even more pressure in the fourth quarter.

Third, management noted that it continues to experience supply shortages and high raw material costs. In other words, cost pressures will intensify in the fourth quarter. Consequently, 3M is seeking to raise prices so that the difference between price and raw material costs becomes margin neutral. At the conference, Patolawala was asked about pricing, to which he replied that investors should "wait and see" what prices 3M gets at the end of the quarter.

The disappointing comments about pricing and the fact that 3M has not been able to offset rising costs with pricing actions call into question the company's business model and/or ability to execute it. For the record, 3M prides itself on investing heavily in research and development to produce differentiated products that have pricing power. Unfortunately, that pricing power is not apparent right now.

Moreover, in recent years, company management has taken significant restructuring measures to improve performance. Indeed, during its third-quarter earnings call, Patolawala told investors that restructuring costs in 2021 would be between $300 million and $325 million, up from a previous forecast of $250 million to $300 million.

Moreover, 3M management has restructured the business (business groups are now managed globally rather than by country) and the healthcare segment has been restructured through multibillion-dollar acquisitions and sales.

So far, none of these restructuring actions has resulted in a noticeable improvement in growth or margins.

Still, it's hard to be too critical of a company's management during a difficult trading period. In addition, Patolawala talked about the likelihood of improvements in volume growth, pricing, lower raw material costs, and the benefits of restructuring in the future. All of these factors point to higher margins in the future.

In addition, 3M stock currently has a dividend yield of 3.5% and is well covered by free cash flow. Thus, the stock remains a good option for income-seeking investors.

Finally, it relies on your investment profile. If you're looking for a relatively safe income source, 3M stock is a useful buy. However, poor operating performance and disappointing guidance will worry investors who prefer to see evidence of progress before buying. For those investors, it makes sense to wait and see what 3M reports in its subsequent earnings releases and what margin growth is projected for 2022.

MMM Breakdown Possibility3M has been in a strong downtrend that I believe is just a long winded pullback but we're not there quite yet, right now things look bad to me, both short and long leading clouds are bearish on shorter timeframes with the long leading cloud about to change over to bearish on the weekly.