RSI(2) com Saída por Tempo OU Alvo (máx 2 barras antes)

RSI(2) entry with MA200

Close after 5 days or

Exit if it reaches the high of the 2 candles prior to entry

Everything visual and ready for backtest

Bands and Channels

SMA Ratio w/ RSI, BB & EMAOverview:

This strategy combines signal-based trend logic with advanced volatility filters, RSI confirmation, dynamic stop-loss/take-profit levels, and higher-timeframe (HTF) trend validation. A fully visual dashboard provides live feedback on market conditions, win rates, and current signal strength.

Key Features:

🔁 Dynamic Stop-Loss/Take-Profit based on ATR and signal strength

📶 Gradient Signal Strength using custom SMA/EMA crossovers

📊 Higher Timeframe Trend Filter for directional bias

🌀 Bollinger Band Squeeze Filter to detect low-volatility breakout zones

💹 RSI Filter to avoid overbought/oversold traps

🧠 Signal Classification: Detects LH/HL Buy/Sell setups and displays them as labels (e.g., "LH Buy", "HL Sell")

🧾 Live Dashboard: Displays signal strength, trend status, volatility, win rate, drawdown, and confidence

🎨 Arcade Theme Option for colorful visual feedback

How It Works:

Entry signals are generated using a differential between fast and slow SMAs (sig) and an EMA of the signal for smoothing.

ATR and Bollinger Band widths adjust SL/TP zones based on market volatility.

Higher timeframe EMA determines bullish or bearish market bias.

Confirmations require RSI agreement and a Bollinger Band squeeze breakout.

Trade Classification Logic:

LH Buy/Sell = Lower High → potential weak reversal

HL Buy/Sell = Higher Low → potential strength after correction

These are shown with labels on the chart to help you assess trade strength visually.

Best Use:

Works on various timeframes

Suitable for trend-following strategies with volatility-based exits

Ideal for traders who want clarity and visual feedback on trade quality

⚠️ Disclaimer: This is a strategy script for educational purposes only. Always test thoroughly on demo accounts before using with real capital.

Bollinger Reversão | Take 100% na Média 20🟢 Entry:

Candle 1: closes below the lower band

Candle 2: closes above the lower band

Entry is made at the high of candle 2 (stop order)

🎯 Total Take Profit (100%):

When the price reaches the 20-period average (middle Bollinger line)

🛑 Stop Loss:

It is at the low between candles 1 and 2 (as before)

15-Minute King (VWAP + Z-Score + CVD Oscillator)fridrich instituational secret . ( limited time only 4 free )

Short Only | EMA100 + MACD + Bearish Candle | Risk 3:1

This strategy is designed for short trades only on any market (crypto, forex, stocks).

It combines three simple but effective conditions:

Price below EMA100 – confirms downtrend.

MACD Line crosses below Signal Line and is bearish – momentum confirmation.

Bearish candle pattern – confirms entry timing.

Risk/Reward is set to 1:3, using ATR-based dynamic take profit and stop loss.

Works well on 30m to 1h timeframes.

Suitable for crypto pairs and volatile instruments.

External Signals Strategy Tester v5External Signals Strategy Tester v5 – User Guide (English)

1. Purpose

This Pine Script strategy is a universal back‑tester that lets you plug in any external buy/sell series (for example, another indicator, webhook feed, or higher‑time‑frame condition) and evaluate a rich set of money‑management rules around it – with a single click on/off workflow for every module.

2. Core Workflow

Feed signals

Buy Signal / Sell Signal inputs accept any series (price, boolean, output of request.security(), etc.).

A crossover above 0 is treated as “signal fired”.

Date filter

Start Date / End Date restricts the test window so you can exclude unwanted history.

Trade engine

Optional Long / Short enable toggles.

Choose whether opposite signals simply close the trade or reverse it (flip direction in one transaction).

Risk modules – all opt‑in via check‑boxes

Classic % block – fixed % Take‑Profit / Stop‑Loss / Break‑Even.

Fibonacci Bollinger Bands (FBB) module

Draws dynamic VWMA/HMA/SMA/EMA/DEMA/TEMA mid‑line with ATR‑scaled Fibonacci envelopes.

Every line can be used for stops, trailing, or multi‑target exits.

Separate LONG and SHORT sub‑modules

Each has its own SL plus three Take‑Profits (TP1‑TP3).

Per TP you set line, position‑percentage to close, and an optional trailing flag.

Executed TP/SLs deactivate themselves so they cannot refire.

Trailing behaviour

If Trail is checked, the selected line is re‑evaluated once per bar; the order is amended via strategy.exit().

3. Inputs Overview

Group Parameter Notes

Trade Settings Enable Long / Enable Short Master switches

Close on Opposite / Reverse Position How to react to a counter‑signal

Risk % Use TP / SL / BE + their % Traditional fixed‑distance management

Fibo Bands FIBO LEVELS ENABLE + visual style/length Turn indicator overlay on/off

FBB LONG SL / TP1‑TP3 Enable, Line, %, Trail Rules applied only while a long is open

FBB SHORT SL / TP1‑TP3 Enable, Line, %, Trail Rules applied only while a short is open

Line choices: Basis, 0.236, 0.382, 0.5, 0.618, 0.764, 1.0 – long rules use lower bands, short rules use upper bands automatically.

4. Algorithm Details

Position open

On the very first bar after entry, the script checks the direction and activates the corresponding LONG or SHORT module, deactivating the other.

Order management loop (every bar)

FBB Stop‑Loss: placed/updated at chosen band; if trailing, follows the new value.

TP1‑TP3: each active target updates its limit price to the selected band (or holds static if trailing is off).

The classic % block runs in parallel; its exits have priority because they call strategy.close_all().

Exit handling

When any strategy.exit() fires, the script reads exit_id and flips the *_Active flag so that order will not be recreated.

A Stop‑Loss (SL) also disables all remaining TPs for that leg.

5. Typical Use Cases

Scenario Suggested Setup

Scalping longs into VWAP‐reversion Enable LONG TP1 @ 0.382 (30 %), TP2 @ 0.618 (40 %), SL @ 0.236 + trailing

Fade shorts during news spikes Enable SHORT SL @ 1.0 (no trail) and SHORT TP1,2,3 on consecutive lowers with small size‑outs

Classic trend‑follow Use only classic % TP/SL block and disable FBB modules

6. Hints & Tips

Signal quality matters – this script manages exits, it does not generate entries.

Keep TV time zone in mind when picking start/end dates.

For portfolio‑style testing allocate smaller default_qty_value than 100 % or use strategy.percent_of_equity sizing.

You can combine FBB exits with fixed‑% ones for layered management.

7. Limitations / Safety

No pyramiding; the script holds max one position at a time.

All calculations are bar‑close; intra‑bar touches may differ from real‑time execution.

The indicator overlay is optional, so you can run visual‑clean tests by unchecking FIBO LEVELS ENABLE.

VWMA + ML RSI StrategyVWMA + ML RSI Strategy

This strategy combines the power of Volume-Weighted Moving Average (VWMA) with a Machine Learning-enhanced RSI to generate high-probability long entries.

✅ Buy Logic:

A buy signal is triggered when:

The candle closes above the VWMA

The ML RSI (smoothed using advanced moving averages) is above 60

If only one of the above conditions is met, the strategy waits for the second to confirm before entering.

❌ Sell Logic:

The position is closed when:

The candle closes below the VWMA, and

The ML RSI falls below 40

🎯 Risk Management:

Take Profit: 1.5% above entry

Stop Loss: 1.5% below entry

🤖 ML RSI Explanation:

The ML RSI is a refined version of the traditional RSI using smoothing techniques (like ALMA, EMA, etc.) to reduce noise and enhance responsiveness to price action. It helps filter out weak signals and improves trend confirmation.

🔧 Customization:

Adjustable VWMA length

Configurable ML RSI smoothing method, length, and ALMA sigma

Thresholds for entry/exit RSI levels

VDN 7 - Ichimoku Fibonacci Strategy (Tenkan:13 / Kijun:21)This strategy utilizes a customized Ichimoku system with Fibonacci-based parameters:

• Tenkan-sen (Conversion Line): 13

• Kijun-sen (Base Line): 21

A long position is opened when Tenkan crosses above Kijun.

A short position is opened when Tenkan crosses below Kijun.

This crossover system filters out noise and captures medium-term trends using Fibonacci-inspired smoothing periods. The strategy is designed for use on 60-minute charts and does not rely on fixed take profit or stop loss — positions are closed upon opposite signal only.

Position size is fixed at 1 lot by default.

Bollinger 2-Candle Reversão | Entrada parcial

New simplified logic:

🟢 Entry:

Candle 1: closes below the lower band

Candle 2: closes above the lower band

Entry is made at the high of candle 2 (stop order)

🎯 Total Take Profit (100%):

When the price reaches the 20-period average (middle Bollinger line)

🛑 Stop Loss:

It is at the low between candles 1 and 2 (as before)

Sanuja nuwanThe Zero Fear Indicator is a custom-built trading tool designed for confident and precise entries. Powered by real-time market structure, volume pressure, and volatility logic, it filters out noise and shows clear buy/sell signals with zero hesitation. Perfect for both beginners and experienced traders looking to trade without fear.

FULLY FUNCTIONAL INDICATOR TESTER🎯 Purpose:

A comprehensive strategy testing framework designed to evaluate custom indicators and trading signals with professional-grade risk management and signal detection capabilities.

✨ Key Features:

Multiple Signal Detection Methods - Value changes, crossovers, threshold-based triggers

Advanced Confluence Filtering - Multi-source confirmation system with lookback periods

Professional Risk Management - Static TP/SL, break-even functionality, position sizing

Custom Exit Signals - Independent exit logic for refined strategy testing

Visual Feedback System - Clear signal plots and real-time status monitoring

Flexible Input Sources - Connect any custom indicator or built-in study

🔧 How to Use:

Connect your indicator outputs to the Entry/Exit source inputs

Select appropriate signal detection method for your indicator type

Configure risk parameters (TP/SL/Break-even)

Enable confluence filters if needed for additional confirmation

Backtest and analyze results with built-in performance metrics

📈 Signal Detection Options:

Value Change: Detects when indicator values change

Crossover Above/Below: Traditional crossover signals

Threshold Triggers: Value-based entry/exit levels

⚙️ Technical Specifications:

Compatible with Pine Script v6

Overlay strategy with position tracking

Real-time performance monitoring table

Configurable margin requirements

Full backtesting compatibility

⚠️ Important Notes:

This is a testing framework - not financial advice

Always validate signals in demo environment first

Past performance does not guarantee future results

Use proper risk management in live trading

🔄 Updates:

Enhanced signal detection algorithms

Improved confluence logic

Added break-even functionality

Visual debugging tools

Perfect for traders and developers looking to systematically tes

EMA 9/21 Crossover Strategy w/ Reversals + Shading9 and 21 EMA cross over. Buy and sell signals on cross over

EMA Cross Strategy only Long📈 EMA Cross Strategy – Only Long

Simple. Clean. Powerful. Designed for strong uptrends.

This is a long-only trend-following strategy based on the classic crossover of Exponential Moving Averages (EMAs). It’s designed for growth stocks and trending assets where upward momentum dominates.

⚙️ How it works:

Entry: when the Fast EMA crosses above the Slow EMA

Exit: when the Fast EMA crosses below the Slow EMA

No shorts, no reversals – just pure trend riding.

By default, the strategy uses 50/100 EMA, which has performed exceptionally well on stocks like NVIDIA (NVDA). These settings can be easily customized to fit your preferred asset or timeframe.

📊 Backtest Example – NVIDIA (NVDA, 1D timeframe)

Test parameters:

Initial capital: $10,000

Order size: 50% of equity per trade (adjustable in settings)

Results:

Net profit: +$2,037,563.63 USD

Gross profit: $2,127,432.33

Gross loss: $89,868.70

Max equity growth: $2,708,648.75 (+99.63%)

Drawdown: 20.00%

Buy & Hold profit: +$30,636,000 USD (but with far more exposure)

The strategy dramatically outperformed passive holding on a risk-adjusted basis, while keeping drawdowns and trade count under control.

🔧 Customization & Risk Management

In the Strategy Settings, you can adjust:

EMA lengths (default: 50 fast, 100 slow)

Order size as a % of equity (e.g., reduce below 50% to lower drawdown)

Backtest range and asset type (works well on growth stocks and trending commodities)

Try this on assets with strong bullish cycles like NVDA, AAPL, MSFT, or Gold (XAU/USD).

⚠️ Disclaimer

This script is for educational and backtesting purposes only. It is not financial advice. Please do your own research and test carefully before trading live.

CNCRADIO talked GPT into Watching the YouTube!Referred GPT to the youtube channel and produced PINE script with no errors first try, followed some prompts and this is the result.

Quantum Reversal# 🧠 Quantum Reversal

## **Quantitative Mean Reversion Framework**

This algorithmic trading system employs **statistical mean reversion theory** combined with **adaptive volatility modeling** to capitalize on Bitcoin's inherent price oscillations around its statistical mean. The strategy integrates multiple technical indicators through a **multi-layered signal processing architecture**.

---

## ⚡ **Core Technical Architecture**

### 📊 **Statistical Foundation**

- **Bollinger Band Mean Reversion Model**: Utilizes 20-period moving average with 2.2 standard deviation bands for volatility-adjusted entry signals

- **Adaptive Volatility Threshold**: Dynamic standard deviation multiplier accounts for Bitcoin's heteroscedastic volatility patterns

- **Price Action Confluence**: Entry triggered when price breaches lower volatility band, indicating statistical oversold conditions

### 🔬 **Momentum Analysis Layer**

- **RSI Oscillator Integration**: 14-period Relative Strength Index with modified oversold threshold at 45

- **Signal Smoothing Algorithm**: 5-period simple moving average applied to RSI reduces noise and false signals

- **Momentum Divergence Detection**: Captures mean reversion opportunities when momentum indicators show oversold readings

### ⚙️ **Entry Logic Architecture**

```

Entry Condition = (Price ≤ Lower_BB) OR (Smoothed_RSI < 45)

```

- **Dual-Condition Framework**: Either statistical price deviation OR momentum oversold condition triggers entry

- **Boolean Logic Gate**: OR-based entry system increases signal frequency while maintaining statistical validity

- **Position Sizing**: Fixed 10% equity allocation per trade for consistent risk exposure

### 🎯 **Exit Strategy Optimization**

- **Profit-Lock Mechanism**: Positions only closed when showing positive unrealized P&L

- **Trend Continuation Logic**: Allows winning trades to run until momentum exhaustion

- **Dynamic Exit Timing**: No fixed profit targets - exits based on profitability state rather than arbitrary levels

---

## 📈 **Statistical Properties**

### **Risk Management Framework**

- **Long-Only Exposure**: Eliminates short-squeeze risk inherent in cryptocurrency markets

- **Mean Reversion Bias**: Exploits Bitcoin's tendency to revert to statistical mean after extreme moves

- **Position Management**: Single position limit prevents over-leveraging

### **Signal Processing Characteristics**

- **Noise Reduction**: SMA smoothing on RSI eliminates high-frequency oscillations

- **Volatility Adaptation**: Bollinger Bands automatically adjust to changing market volatility

- **Multi-Timeframe Coherence**: Indicators operate on consistent timeframe for signal alignment

---

## 🔧 **Parameter Configuration**

| Technical Parameter | Value | Statistical Significance |

|-------------------|-------|-------------------------|

| Bollinger Period | 20 | Standard statistical lookback for volatility calculation |

| Std Dev Multiplier | 2.2 | Optimized for Bitcoin's volatility distribution (95.4% confidence interval) |

| RSI Period | 14 | Traditional momentum oscillator period |

| RSI Threshold | 45 | Modified oversold level accounting for Bitcoin's momentum characteristics |

| Smoothing Period | 5 | Noise reduction filter for momentum signals |

---

## 📊 **Algorithmic Advantages**

✅ **Statistical Edge**: Exploits documented mean reversion tendency in Bitcoin markets

✅ **Volatility Adaptation**: Dynamic bands adjust to changing market conditions

✅ **Signal Confluence**: Multiple indicator confirmation reduces false positives

✅ **Momentum Integration**: RSI smoothing improves signal quality and timing

✅ **Risk-Controlled Exposure**: Systematic position sizing and long-only bias

---

## 🔬 **Mathematical Foundation**

The strategy leverages **Bollinger Band theory** (developed by John Bollinger) which assumes that prices tend to revert to the mean after extreme deviations. The RSI component adds **momentum confirmation** to the statistical price deviation signal.

**Statistical Basis:**

- Mean reversion follows the principle that extreme price deviations from the moving average are temporary

- The 2.2 standard deviation multiplier captures approximately 97.2% of price movements under normal distribution

- RSI momentum smoothing reduces noise inherent in oscillator calculations

---

## ⚠️ **Risk Considerations**

This algorithm is designed for traders with understanding of **quantitative finance principles** and **cryptocurrency market dynamics**. The strategy assumes mean-reverting behavior which may not persist during trending market phases. Proper risk management and position sizing are essential.

---

## 🎯 **Implementation Notes**

- **Market Regime Awareness**: Most effective in ranging/consolidating markets

- **Volatility Sensitivity**: Performance may vary during extreme volatility events

- **Backtesting Recommended**: Historical performance analysis advised before live implementation

- **Capital Allocation**: 10% per trade sizing assumes diversified portfolio approach

---

**Engineered for quantitative traders seeking systematic mean reversion exposure in Bitcoin markets through statistically-grounded technical analysis.**

TrendMaster Pro 2.3 with Alerts

Hello friends,

A member of the community approached me and asked me how to write an indicator that would achieve a particular set of goals involving comprehensive trend analysis, risk management, and session-based trading controls. Here is one example method of how to create such a system:

Core Strategy Components

Multi-Moving Average System - Uses configurable MA types (EMA, SMA, SMMA) with short-term (9) and long-term (21) periods for primary signal generation through crossovers

Higher Timeframe Trend Filter - Optional trend confirmation using a separate MA (default 50-period) to ensure trades align with broader market direction

Band Power Indicator - Dynamic high/low bands calculated using different MA types to identify price channels and volatility zones

Advanced Signal Filtering

Bollinger Bands Volatility Filter - Prevents trading during low-volatility ranging markets by requiring sufficient band width

RSI Momentum Filter - Uses customizable thresholds (55 for longs, 45 for shorts) to confirm momentum direction

MACD Trend Confirmation - Ensures MACD line position relative to signal line aligns with trade direction

Stochastic Oscillator - Adds momentum confirmation with overbought/oversold levels

ADX Strength Filter - Only allows trades when trend strength exceeds 25 threshold

Session-Based Trading Management

Four Trading Sessions - Asia (18:00-00:00), London (00:00-08:00), NY AM (08:00-13:00), NY PM (13:00-18:00)

Individual Session Limits - Separate maximum trade counts for each session (default 5 per session)

Automatic Session Closure - All positions close at specified market close time

Risk Management Features

Multiple Stop Loss Options - Percentage-based, MA cross, or band-based SL methods

Risk/Reward Ratio - Configurable TP levels based on SL distance (default 1:2)

Auto-Risk Calculation - Dynamic position sizing based on dollar risk limits ($150-$250 range)

Daily Limits - Stop trading after reaching specified TP or SL counts per day

Support & Resistance System

Multiple Pivot Types - Traditional, Fibonacci, Woodie, Classic, DM, and Camarilla calculations

Flexible Timeframes - Auto-adjusting or manual timeframe selection for S/R levels

Historical Levels - Configurable number of past S/R levels to display

Visual Customization - Individual color and display settings for each S/R level

Additional Features

Alert System - Customizable buy/sell alert messages with once-per-bar frequency

Visual Trade Management - Color-coded entry, SL, and TP levels with fill areas

Session Highlighting - Optional background colors for different trading sessions

Comprehensive Filtering - All signals must pass through multiple confirmation layers before execution

This approach demonstrates how to build a professional-grade trading system that combines multiple technical analysis methods with robust risk management and session-based controls, suitable for algorithmic trading across different market sessions.

Good luck and stay safe!

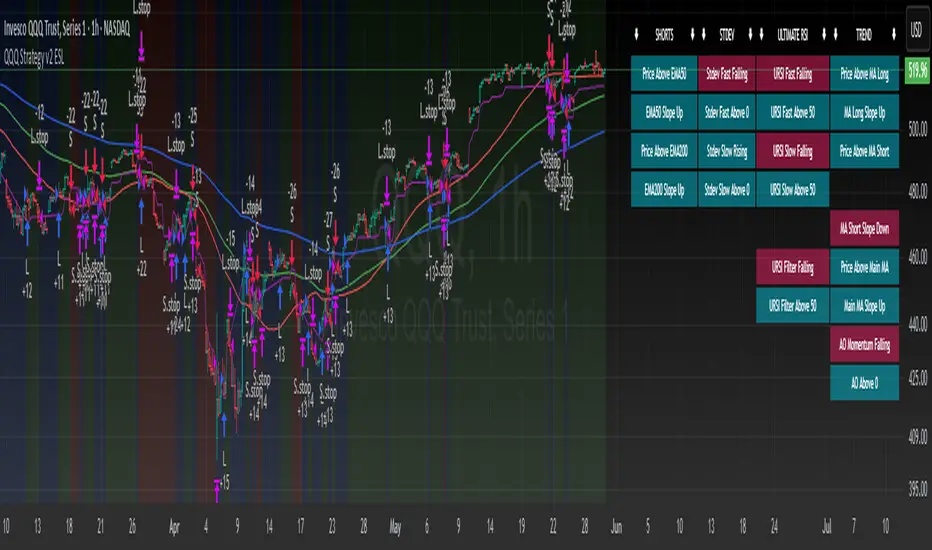

QQQ Strategy v2 ESL | easy-peasy-x This is a strategy optimized for QQQ (and SPY) for the 1H timeframe. It significantly outperforms passive buy-and-hold approach. With settings adjustments, it can be used on various assets like stocks and cryptos and various timeframes, although the default out of the box settings favor QQQ 1H.

The strategy uses various triggers to take both long and short trades. These can be adjusted in settings. If you try a different asset, see what combination of triggers works best for you.

Some of the triggers employ LuxAlgo's Ultimate RSI - shoutout to him for great script, check it out here .

Other triggers are based on custom signed standard deviation - basically the idea is to trade Bollinger Bands expansions (long to the upside, short to the downside) and fade or stay out of contractions.

There are three key moving averages in the strategy - LONG MA, SHORT MA, BASIC MA. Long and Short MAs are guides to eyes on the chart and also act as possible trend filters (adjustable in settings). Basic MA acts as guide to eye and a possible trade trigger (adjustable in settings).

There are a few trend filters the strategy can use - moving average, signed standard deviation, ultimate RSI or none. The filters act as an additional condition on triggers, making the strategy take trades only if both triggers and trend filter allows. That way one can filter out trades with unfavorable risk/reward (for instance, don't long if price is under the MA200). Different trade filters can be used for long and short trades.

The strategy employs various stop loss types, the default of which is a trailing %-based stop loss type. ATR-based stop loss is also available. The default 1.5% trailing stop loss is suitable for leveraged trading.

Lastly, the strategy can trigger take profit orders if certain conditions are met, adjustable in settings. Also, it can hold onto winning trades and exit only after stop out (in which case, consecutive triggers to take other positions will be ignored until stop out).

Let me know if you like it and if you use it, what kind of tweaks would you like to see.

With kind regards,

easy-peasy-x

SOXL Trend Surge v3.0.2 – Profit-Only RunnerSOXL Trend Surge v3.0.2 – Profit-Only Runner

This is a trend-following strategy built for leveraged ETFs like SOXL, designed to ride high-momentum waves with minimal interference. Unlike most short-term scalping scripts, this model allows trades to develop over multiple days to even several months, capitalizing on the full power of extended directional moves — all without using a stop-loss.

🔍 How It Works

Entry Logic:

Price is above the 200 EMA (long-term trend confirmation)

Supertrend is bullish (momentum confirmation)

ATR is rising (volatility expansion)

Volume is above its 20-bar average (liquidity filter)

Price is outside a small buffer zone from the 200 EMA (to avoid whipsaws)

Trades are restricted to market hours only (9 AM to 2 PM EST)

Cooldown of 15 bars after each exit to prevent overtrading

Exit Strategy:

Takes partial profit at +2× ATR if held for at least 2 bars

Rides the remaining position with a trailing stop at 1.5× ATR

No hard stop-loss — giving space for volatile pullbacks

⚙️ Strategy Settings

Initial Capital: $500

Risk per Trade: 100% of equity (fully allocated per entry)

Commission: 0.1%

Slippage: 1 tick

Recalculate after order is filled

Fill orders on bar close

Timeframe Optimized For: 45-minute chart

These parameters simulate an aggressive, high-volatility trading model meant for forward-testing compounding potential under realistic trading costs.

✅ What Makes This Unique

No stop-loss = fewer premature exits

Partial profit-taking helps lock in early wins

Trailing logic gives room to ride large multi-week moves

Uses strict filters (volume, ATR, EMA bias) to enter only during high-probability windows

Ideal for leveraged ETF swing or position traders looking to hold longer than the typical intraday or 2–3 day strategies

⚠️ Important Note

This is a high-risk, high-reward strategy meant for educational and testing purposes. Without a stop-loss, trades can experience deep drawdowns that may take weeks or even months to recover. Always test thoroughly and adjust position sizing to suit your risk tolerance. Past results do not guarantee future returns. Backtest range: May 8, 2020 – May 23, 2025

Range Filter Strategy with ATR TP/SLHow This Strategy Works:

Range Filter:

Calculates a smoothed average (SMA) of price

Creates upper and lower bands based on standard deviation

When price crosses above upper band, it signals a potential uptrend

When price crosses below lower band, it signals a potential downtrend

ATR-Based Risk Management:

Uses Average True Range (ATR) to set dynamic take profit and stop loss levels

Take profit is set at entry price + (ATR × multiplier) for long positions

Stop loss is set at entry price - (ATR × multiplier) for long positions

The opposite applies for short positions

Input Parameters:

Adjustable range filter length and multiplier

Customizable ATR length and TP/SL multipliers

All parameters can be optimized in TradingView's strategy tester

You can adjust the input parameters to fit your trading style and the specific market you're trading. The ATR-based exits help adapt to current market volatility.

Big Mover Catcher BTC 4h🧠 Big Mover Catcher (BTC 4H Strategy) — Educational Tool

⚠️ Disclaimer: I am not a financial advisor. This script is for educational and testing purposes only. Cryptocurrency trading is highly volatile and involves significant risk. You can lose all of your invested capital.

📌 Overview

The Big Mover Catcher strategy is a work-in-progress trading system designed for Bitcoin (BTC) on the 4-hour chart. It aims to identify strong breakout moves by combining multiple technical indicators and conditions, allowing for high customization and filter-based confirmations.

This script is part of a personal project to learn Pine Script and backtesting on TradingView. It is currently in the testing and research phase.

🎯 Strategy Objective

Catch large, high-momentum breakout moves in the BTC market using:

Bollinger Band breakouts for entry signals

Momentum, volatility, and trend filters for trade confirmation

🧰 Features & Filters

The script provides a flexible set of filters that can be turned ON/OFF and adjusted directly from the settings panel:

✅ Entry Conditions

Price must break above or below Bollinger Bands

All selected filters must align before entry

🧪 Available Filters:

Relative Strength Index (RSI) with EMA/SMA smoothing

Average Directional Index (ADX) with EMA/SMA smoothing

Average True Range (ATR) with EMA/SMA smoothing

MACD Signal above or below zero

EMA 350 trend filter

ATR / ADX / RSI Threshold toggles for added control

🔥 Additional Feature:

Force Take Profit: Optionally closes the trade immediately if a candle closes with more than a defined % movement (default: 5%). This can help lock in quick profits during high volatility moves.

⚙️ Customizable Inputs

You can configure:

Stop loss percentage

All indicator lengths

Smoothing types (EMA/SMA)

Threshold activation toggles

Individual filter ON/OFF switches

This makes the strategy highly adaptable for educational exploration and optimization.

📊 Best Used For

Learning Pine Script and strategy structure

Testing filter combinations for BTC on the 4H timeframe

Understanding how different indicators interact in live markets

⚠️ Note: ❌ Short trades are currently disabled by default, as short-side logic is still under development.

❗ Final Reminder

This script is not financial advice. It is an educational tool. Use it to learn and explore trading logic. Trading cryptocurrencies carries high risk — only invest what you can afford to lose.

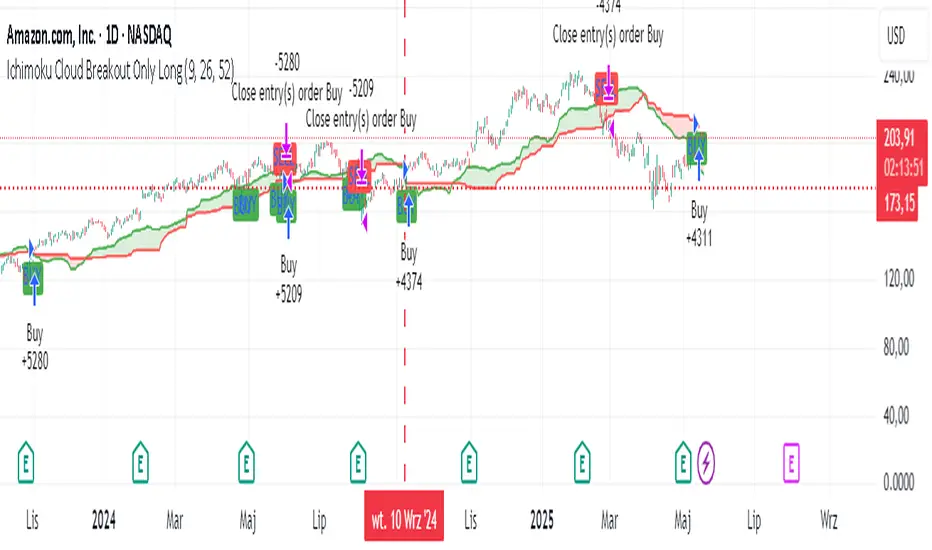

Ichimoku Cloud Breakout Only LongThis is a very simple trading strategy based exclusively on the Ichimoku Cloud. There are no additional indicators or complex rules involved. The key condition is that we only open long positions when the price is clearly above the cloud — indicating a bullish trend.

For optimal results, the recommended timeframes are 1D (daily) or 1W (weekly) charts. These higher timeframes help filter out market noise and provide more reliable trend signals.

We do not short the market under any circumstances. The focus is purely on riding upward momentum when the price breaks out or stays above the cloud.

This strategy works best when applied to growth stocks with strong upward trends and good fundamentals — such as Google (GOOGL), Tesla (TSLA), Apple (AAPL), or NVIDIA (NVDA).

Gold Breakout Strategy - RR 4Strategy Name: Gold Breakout Strategy - RR 4

🧠 Main Objective

This strategy aims to capitalize on breakouts from the Donchian Channel on Gold (XAU/USD) by filtering trades with:

Volume confirmation,

A custom momentum indicator (LWTI - Linear Weighted Trend Index),

And a specific trading session (8 PM to 8 AM Quebec time — GMT-5).

It takes only one trade per day, either a buy or a sell, using a fixed stop-loss at the wick of the breakout candle and a 4:1 reward-to-risk (RR) ratio.

📊 Indicators Used

Donchian Channel

Length: 96

Detects breakouts of recent highs or lows.

Volume

Simple Moving Average (SMA) over 30 bars.

A breakout is only valid if the current volume is above the SMA.

LWTI (Linear Weighted Trend Index)

Measures momentum using price differences over 25 bars, smoothed over 5.

Used to confirm trend direction:

Buy when LWTI > its smoothed version (uptrend).

Sell when LWTI < its smoothed version (downtrend).

⏰ Time Filter

The strategy only allows entries between 8 PM and 8 AM (GMT-5 / Quebec time).

A timestamp-based filter ensures the system recognizes the correct trading session even across midnight.

📌 Entry Conditions

🟢 Buy (Long)

Price breaks above the previous Donchian Channel high.

The current channel high is higher than the previous one.

Volume is above its moving average.

LWTI confirms an uptrend.

The time is within the trading session (20:00 to 08:00).

No trade has been taken yet today.

🔴 Sell (Short)

Price breaks below the previous Donchian Channel low.

The current channel low is lower than the previous one.

Volume is above its moving average.

LWTI confirms a downtrend.

The time is within the trading session.

No trade has been taken yet today.

💸 Trade Management

Stop-Loss (SL):

For long entries: placed below the wick low of the breakout candle.

For short entries: placed above the wick high of the breakout candle.

Take-Profit (TP):

Set at a fixed 4:1 reward-to-risk ratio.

Calculated as 4x the distance between the entry price and stop-loss.

No trailing stop, no break-even, no scaling in/out.

🎨 Visuals

Green triangle appears below the candle on a buy signal.

Red triangle appears above the candle on a sell signal.

Donchian Channel lines are plotted on the chart.

The strategy is designed for the 5-minute timeframe.

🔄 One Trade Per Day Rule

Once a trade is taken (buy or sell), no more trades will be executed for the rest of the day. This prevents overtrading and limits exposure.

Smart Fib StrategySmart Fibonacci Strategy

This advanced trading strategy combines the power of adaptive SMA entries with Fibonacci-based exit levels to create a comprehensive trend-following system that self-optimizes based on historical market conditions. Credit goes to Julien_Eche who created the "Best SMA Finder" which received an Editors Pick award.

Strategy Overview

The Smart Fibonacci Strategy employs a two-pronged approach to trading:

1. Intelligent Entries: Uses a self-optimizing SMA (Simple Moving Average) to identify optimal entry points. The system automatically tests multiple SMA lengths against historical data to determine which period provides the most robust trading signals.

2. Fibonacci-Based Exits: Implements ATR-adjusted Fibonacci bands to establish precise exit targets, with risk-management options ranging from conservative to aggressive.

This dual methodology creates a balanced system that adapts to changing market conditions while providing clear visual reference points for trade management.

Key Features

- **Self-Optimizing Entries**: Automatically calculates the most profitable SMA length based on historical performance

- **Adjustable Risk Parameters**: Choose between low-risk and high-risk exit targets

- **Directional Flexibility**: Trade long-only, short-only, or both directions

- **Visualization Tools**: Customizable display of entry lines and exit bands

- **Performance Statistics**: Comprehensive stats table showing key metrics

- **Smoothing Option**: Reduces noise in the Fibonacci bands for cleaner signals

Trading Rules

Entry Signals

- **Long Entry**: When price crosses above the blue center line (optimal SMA)

- **Short Entry**: When price crosses below the blue center line (optimal SMA)

### Exit Levels

- **Low Risk Option**: Exit at the first Fibonacci band (1.618 * ATR)

- **High Risk Option**: Exit at the second Fibonacci band (2.618 * ATR)

Strategy Parameters

Display Settings

- Toggle visibility of the stats table and indicator components

Strategy Settings

- Select trading direction (long, short, or both)

- Choose exit method (low risk or high risk)

- Set minimum trades threshold for SMA optimization

SMA Settings

- Option to use auto-optimized or fixed-length SMA

- Customize SMA length when using fixed option

Fibonacci Settings

- Adjust ATR period and SMA basis for Fibonacci bands

- Enable/disable smoothing function

- Customize Fibonacci ratio multipliers

Appearance Settings

- Modify colors, line widths, and transparency

Optimization Methodology

The strategy employs a sophisticated optimization algorithm that:

1. Tests multiple SMA lengths against historical data

2. Evaluates performance based on trade count, profit factor, and win rate

3. Calculates a "robustness score" that balances profitability with statistical significance

4. Selects the SMA length with the highest robustness score

This ensures that the strategy's entry signals are continuously adapting to the most effective parameters for current market conditions.

Risk Management

Position sizing is fixed at $2,000 per trade, allowing for consistent exposure across all trading setups. The Fibonacci-based exit system provides two distinct risk management approaches:

- **Conservative Approach**: Using the first Fibonacci band for exits produces more frequent but smaller wins

- **Aggressive Approach**: Using the second Fibonacci band allows for larger potential gains at the cost of increased volatility

Ideal Usage

This strategy is best suited for:

- Trending markets with clear directional moves

- Timeframes from 4H to Daily for most balanced results

- Instruments with moderate volatility (stocks, forex, commodities)

Traders can further enhance performance by combining this strategy with broader market analysis to confirm the prevailing trend direction.

Reverse Keltner Channel StrategyReverse Keltner Channel Strategy

Overview

The Reverse Keltner Channel Strategy is a mean-reversion trading system that capitalizes on price movements between Keltner Channels. Unlike traditional Keltner Channel strategies that trade breakouts, this system takes the contrarian approach by entering positions when price returns to the channel after overextending.

Strategy Logic

Long Entry Conditions:

Price crosses above the lower Keltner Channel from below

This signals a potential reversal after an oversold condition

Position is entered at market price upon signal confirmation

Long Exit Conditions:

Take Profit: Price reaches the upper Keltner Channel

Stop Loss: Placed at half the channel width below entry price

Short Entry Conditions:

Price crosses below the upper Keltner Channel from above

This signals a potential reversal after an overbought condition

Position is entered at market price upon signal confirmation

Short Exit Conditions:

Take Profit: Price reaches the lower Keltner Channel

Stop Loss: Placed at half the channel width above entry price

Key Features

Mean Reversion Approach: Takes advantage of price tendency to return to mean after extreme moves

Adaptive Stop Loss: Stop loss dynamically adjusts based on market volatility via ATR

Visual Signals: Entry points clearly marked with directional triangles

Fully Customizable: All parameters can be adjusted to fit various market conditions

Customizable Parameters

Keltner EMA Length: Controls the responsiveness of the channel (default: 20)

ATR Multiplier: Determines channel width/sensitivity (default: 2.0)

ATR Length: Affects volatility calculation period (default: 10)

Stop Loss Factor: Adjusts risk management aggressiveness (default: 0.5)

Best Used On

This strategy performs well on:

Currency pairs with defined ranging behavior

Commodities that show cyclical price movements

Higher timeframes (4H, Daily) for more reliable signals

Markets with moderate volatility

Risk Management

The built-in stop loss mechanism automatically adjusts to market conditions by calculating position risk relative to the current channel width. This approach ensures that risk remains proportional to potential reward across varying market conditions.

Notes for Optimization

Consider adjusting the EMA length and ATR multiplier based on the specific asset and timeframe:

Lower values increase sensitivity and generate more signals

Higher values produce fewer but potentially more reliable signals

As with any trading strategy, thorough backtesting is recommended before live implementation.

Past performance is not indicative of future results. Always practice sound risk management.