PhinkTrade Risk Manager EssentialsHello there, fellow traders!

So, happy to bring you a new, free tool: my Risk Manager Essentials .

(To use it, click on "Add to favorite indicators" below, and then look for it in your charts’ "Indicators & Strategies" dialog window, inside "Favorites" tab.)

The main objective of this indicator is to help and incentivize as many traders as possible to adopt essential risk management practices .

First and foremost, it helps you define how much you can buy or sell, at your chosen price levels, in order to keep your risk always under control (in other words: in order to limit the amount you can potentially lose with a trade if your stop loss order is hit).

This is fundamental if you want to have a lasting and successful trading career: protect your capital, always . Because without it, you know: it’s game over.

Indicator also helps you visualize where minimum ideal target / take profit level is , given your risk, using the popular 3:1 Return/Risk ratio (R/R) .

3:1 R/R ratio is popular because with it you only need to “be right” (have price reach your targets) about 33% of the time, in order to be profitable : in other words, the fewer successful trades will pay you more than the sum of your unsuccessful ones will take from you.

So, make sure your strategy has a success rate greater than 33% and apply 3:1 R/R to your trades . This indicator will help you that, and with developing the necessary discipline . For example, by knowing where the ideal target should be, given your choices, you can assess the likelihood of it being reached in current price context. If that would look like a hard to happen scenario, it would probably be a good idea to avoid taking that particular trade.

Now, let’s see how it works:

When you deploy the indicator to the chart for the first time, you’ll be asked to define:

Your 1st entry price (interactively: you can define and adjust levels directly on the chart, thanks to the new Interactive Mode introduced by TradingView (ty, TV team!))

Your stop loss price (likewise)

Your 1st target price (likewise)

Your starting capital (via initial Input dialog)

Your risk (likewise)

Your risk is how much of your starting capital you are willing to lose if your stop loss is hit (define it as a % of your starting capital).

There’s a good practice here too: to risk only 1 percent of your capital per trade . This way, you can reinforce the odds of making more money than you lose and keep your peace of mind in all trades – and avoid messing up with your plans – and statistics – along the way.

Successful trading is a statistics-based endeavor. So, you want to implement and maintain consistency. Again, this indicator helps with that.

After initial setup:

You can also define additional entries and targets (up to 3 each) . Just open indicator’s Settings window and adjust accordingly.

If you have more than one entry – or target, the amounts involved will be split evenly between them. You can also enable the display of the Average Entry and Average Target labels , to see the equivalent, should you have taken (or take) a single order for each.

You can also define (via Settings, then interactively) a particular date and time for the trade . This way, labels will be presented near that moment, instead of constantly show near the latest bar.

Finally, you can personalize some other display settings: levels precision (number of decimal places), labels positions , and labels colors .

In conclusion:

You are very welcome to check it out – and adopt it on your daily use!

Please let me know your feedbacks as well. If you find any issues, or have any suggestions, I’ll be glad to hear. You can contact me here, via TradingView, or Telegram.

Finally, check the updates section below , as new stuff may show from time to time.

Thank you very much for your attention, and enjoy!

PhinkTrade

Statistics

Portfolio of open positions ENGHello, I became interested in investing and trading, and there was a huge problem where and how to manage my portfolio,

I tried websites, got a spreadsheet in microsoft excel, and eventually it became possible to manage a portfolio in TradingView.

You enter data about purchases and follow the dynamics of your shares anytime, anywhere.

Added automatic transfer to one currency if the shares are traded in different currencies

The last column is how many percentages each share occupies of the total portfolio

Thanks to the TradingView team for the unique opportunity!

Collective IndicatorKey notes are that this indicators markets the High and Low of the previous day, week month and quarter. It also marks the open of the day, week, month and quarter. These are levels that can be important areas to take trades towards and away from.

It includes additional features some may wish to use that I've included for your convenience that I don't personally use anymore. This is the 50 and 200 EMAs and high volume candle coloring. EMAs can be helpful for identifying the average markup and markdown of a a trend on any given timeframe. Be careful with mean reversion strategies alone since they tend not to have great entries and could result in high losses if used in isolation.

The "Length" and "High Volume" settings control how the coloration of candles is applied. Length is the amount of bars it will use to calculate a volume average. "High Volume" is the multiplier used to distinguish how much additional volume you want to be considered "high" volume. 1x meaning average 2x meaning double volume and etc.

High volume identification can help show distributive or accumulative characteristics around key areas.

I personally focus on the Open, Low, High close data, apply SMC concepts and Wyckoff concepts to look for trades around these key areas.

ATH ATL ATX FinderHello!

This is an indicator to determine ATH, ATL and ATX:

ATH - All time high

ATL - All time low

ATX - All time X

X to ATH - how many X is possible to get when reach ATH

ATH from X - how many X is already archieved from ATL

How to use:

Select any market and see abovementioned parameters.

You may alter initial date to start from in the settings.

Enjoy!

Yearly Percentage ReturnsAn indicator that lets you visualize the historical Yearly Percentage returns of any symbol .

Key Features:

Displays the yearly returns from start to end of each year

Displays a table showing all yearly returns for current symbol

Displays start of each year as a vertical line

Displays up to 5 custom horizontal levels

Table Settings:

Enable table - Show/Hide the table

Size - Sets the size of the table

Position - Sets the position of the table on the screen

Direction - Sets the direction of the table to display the data (Vertically or Horizontally)

seasonThis script is meant to help verify the existence of a seasonal effect in asset returns, using a Z-test. There are three steps:

1. Think of a way to identify a season. The available methods are: by month, by week of the year, by day of the month, by day of the week, by hour of the day, and by minute of the hour.

2. Set the chart to the unit of your season. For example, if you want to check whether a crop commodity's harvest season has a seasonal implication, select "month". If you want to investigate the exchange's opening or close, select "hour".

3. Using the inputs, select the unit (e.g. "month", "dayofweek", "hour", etc.) and the range that identifies the season. The example natural gas chart has set "start" to 8 and "end" to 12 for September through December.

The test logic is as follows:

The "season" you select has a fixed length; for example, months eight through twelve has a length of four. This length is used to compute a sample mean, which is the mean return of all September-December periods in the chart. It is also used to calculate the mean/stdev of every other four-month period in the chart history. The latter is considered the "population." Using a Z-test, the script scores the difference between the sample returns and the population returns, and displays the results at two levels of significance (P = 0.05 and P = 0.01). The null hypothesis is "there is no difference between the seasonal periods and the population of ordinary periods". If the Z-score is sufficiently large or small, we can reject the null hypothesis and say that there is a seasonal effect at the given level of confidence. The output table will show green for a rejection of the null hypothesis (meaning there is a seasonal effect) or red of acceptance (there is no seasonal effect).

The seasonal periods that you have defined will be highlighted on the chart, so you can make sure they are correct. Additionally, the output table shows the mean, median, standard deviation, and top and bottom percentiles for both the seasonal and population samples.

Many news sites, twitter feeds, influences, etc. enjoy posting statistics about past returns, like "the stock market has gone up on this day 85 out of the past 100 years" and so on. Unfortunately, these posts don't tell you that many of these statistics are meaningless, as even totally random price fluctuations will cause many such interesting figures to occur. This script provides a limited means of testing some such seasonal effects so you can see if they are probably just random, or if they may have some meaning.

Note that Tradingview seems to use 1-based indexing for daily or higher timeframes, and 0-based indexing for intraday timeframes:

Months: 1-12

Weeks: 1-52

Days (of month): 1-31

Days (of week): 1-7

Hours (of day): 0-23

Minutes (of hour): 0-59

Front Angler Percent CJA nice little gadget.

Can be used to visually hint on volatility.

Will show a leading vertical bar which shows percentage of price, both up and down, in relation to current price.

[blackcat] L3 Financial Minesweeper: Altman Z ScoreLevel: 3

Background

The Altman Z-score is the output of a credit-strength test that gauges a publicly traded manufacturing company's likelihood of bankruptcy. The Altman Z-score is a formula for determining whether a company, notably in the manufacturing space, is headed for bankruptcy.

Function

The possibility of financial failure or bankruptcy of the enterprise is analyzed and predicted through the comprehensive score. The lower the Z value, the more likely the enterprise will go bankrupt. By calculating the Z value of an enterprise for several consecutive years, we can find out whether the enterprise has signs of financial crisis. Generally speaking, when the Z value is greater than 2.675, it indicates that the financial situation of the enterprise is good, and the possibility of bankruptcy is small; When the value is less than 1.81, it indicates that the enterprise is in a potential bankruptcy crisis; when the Z value is between 1.81 and 2.675, it is called a "gray area, indicating that the financial situation of the enterprise is extremely unstable.

Remarks

STOCKs ONLY which require financial data.

X1~X5 coefficients can be customized for different stock markets.

Compared to TradingView official Altman Z-Score Indicator.

Feedbacks are appreciated.

Correlation Coefficient Comparison (2 inputs)Same as Correlation Coefficient, but allows you to specify both inputs.

normalize_heatmap

Description:

This was a simple indicator to indicate the heatmap area of an asset price, in a relative given time period. In default the lookback period was set to 50 bars, indicating the current state of the price within the previous lookback period. The color scheme was using the rainbow palette, which set blue as the cooling-off area, and red as the heating area. The indicator doesn't take into account momentum strategy and thus doesn't consider the future direction of the asset price. Note: cooling-off area, can be considered to entry or adding position as a DCA strategy.

Data Normalize:

norm = (x - min) / (max - min)

Feature:

Heatmap color condition

Weighted Moving average (Additional)

% Price change (by OP)To visually evaluate the percentage change in price over any time period

This handsome indicator shows exact % price change at each candle by displaying a circle at the level of the change. To read numerical value, point at the circle of the relevant bar corresponding to the candle you are interested in, and look at the scale.

TotalCap Structure CandlesIdeal to see the overvaluation or undervaluation of the market observing the structural divergences.

You can also do your technical analysis on this structure, helping to understand the total market.

Let the simplicity of your strategy be your strength, successes.

VarianceVariance is a measure of dispersion, simply put, it is measuring how distant data is from it's mean(average). This indicator allows you to see when variance is increasing or decreasing, as well as when it is at an extreme value. Thru this, you can get a more accurate description of risk. When variance is increasing/high, you know to expect larger moves, as data(price) is far and getting farther from the mean. and when it is low/decreasing, you know that price movement is more likely to be less volatile due to data clustering closer to the mean, ie ; smaller values.

Variance is not a signal generating indicator in and of itself, but is more a tool to help tell you WHEN to trade. Use in conjunction with signal generating indicators such as Z-score to find entries.

For example, trading z score extremes when variance is increasing.

Variance works well alongside measurements of historical volatility to get a more accurate measurement of market risk/ volatility .

Volume CompressorTurns volume into a more informative representation, ready to be further analyzed

...

Rationale

Volume

Back in the "before the quant" days I was a big fan of market & volume profile. Thing is J. Steidlmayer had lotta different ideas & works aside of profiling, it's just most of them ain't got to mainstream, one of them was "Hot / Cold volume" (yes, you can't really google it). From my interpretation, the idea was that in a given asset there is a usual constant volume that stays there no matter what, and if it ever changes it changes very slow and gradually; and there's another kind of, so to say, 'active' volume that actually influences price dynamics and very volatile by its nature. So I've met concept lately, and decided to quantify & model it one day when I'll have an idea how. That day was yesterday.

Compression

When we do music we always use different kinds of filters (low-pass, high pass, etc) for equalization and filtering itself. That stuff we use in finance as well. What we also always use in music are compressors, there dynamic processors that automatically adjust volume so it will be more consistent. Almost all the cool music you hear is compressed (both individual instruments (especially vocals) and the whole track afterwards), otherwise stuff will be too quite and too weak to flex on it, and also DJing it would be a nightmare. I am a big adept of loudness war. So I was like, how can I use compression in finance, when ima get an idea? That day was yesterday as well.

Volume structure

Being inspired by Steidlmayer's idea, I decided to distinguish volume this way:

1) Passive / static volume. The ~ volume that's always there no matter what (hedges, arbitrages, spread legs, portfolio parts etc etc), doesn't affect things;

2) Active / dynamic volume. The volume that flows from one asset to another, really matters and affects things;

3) Excess volume. The last portion of number 2 volume, that doesn't represent any powerful value to affect things.

Now it's clear that we can get rid of number 1 and number 3, the components that don't really matter, and concentrate on number 2 in order to improve information gain, both for ourselves and for the models we feed this data. How?

Model

I don't wanna explain it all in statistical / DSP way for once.

First of all, I think the population of volumes is log-normally distributed, so let's take logs of volumes, now we have a ~ normally distributed data. We take linearly weighted mean, add and subtract linearly weighted standard deviation from it, these would be our thresholds, the borders between different kinds of volumes explained before.

The upper threshold is for downward compression, that will not let volume pass it higher.

The lower threshold is for upward compression, all the volumes lower than this threshold will be brought up to the threshold's level.

Then we apply multipliers to the thresholds in order to adjust em and find the sweet spots. We do it the same way as in sound engineering when we don't aim for overcompression, we adjust the thresholds until they start to touch the signal and all good.

Afterwards, we delete all the number 1 and number 3 volume, leaving us exclusively with the clear main component, ready to be processed further.

We return the volumes to dem real scale.

About the parameters, based on testing I don't recommend changing the thresholds from dem default values, first of all they make sense statistically and second they work as intended.

Window length can and should be adjusted, find your own way, or leave the default value. ML (moving location) length is up to you as well.

So yeah, you can see now we can smooth the data and make it visually appealing not only by applying a smooth filter over it.

All good TV?

All Central Bank Interest RatesWith another period of mass interest rates manipulation, I created this indicator to show them all. It reveals latest interest ratest (at a time of the last update) and a date when each central bank manipulated the rates.

If you would rather view a single pair data check: and

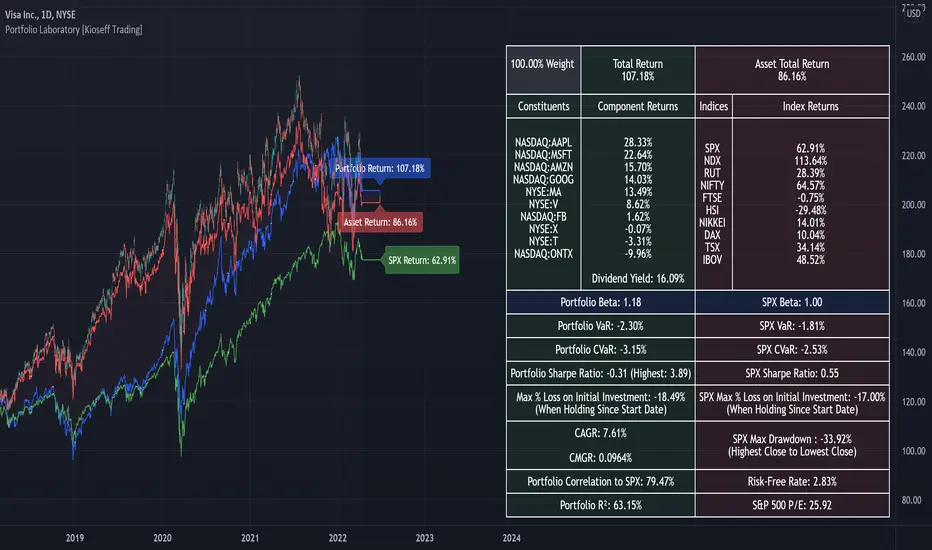

Portfolio Laboratory [Kioseff Trading]Hello!

This script looks to experiment with historical portfolio performance. However, a hypothetical cash balance is not used; weighted percentage increases and decreases are used.

You can select up to 10 assets to include in the portfolio. Long and short positions are possible.

Show in the image are the portfolio's weight, the total return of the portfolio and the total return of the asset on the chart over the selected timeframe.

Shown in the image above are the constituents of the portfolio, which can include any asset, the weighted percentage gain/loss of the constituents in addition to 10 major indices and their respective total percentage gain/loss over the timeframe.

Shown in the image above are the dividend yield % of the portfolio and relevant portfolio metrics - ex-post calculations are applied and are predicated on simple returns.

Shown in the image above is a portfolio of all short positions; portfolio calculations adjusted to the modifications.

Also shown is a change in the index the portfolio is calculated against. I have been asked a few times to include NIFTY 50 in my scripts - I made sure this was achieved, lol!

Show in the image is a performance line of performance of percentage increases/decreases for the index calculated against, the asset on the chart, and the portfolio.

All lines start simultaneously on the selected start date at the close price of the session for the asset on your chart.

However, the right-hand scale, whether displaying price or percent, cannot be used to assess the performance of each line - they are useful for visualization only and can extend below zero on a low-priced asset. Calculations will not execute correctly when selecting a start date prior to any asset in the portfolio's first trading session; calculations do not begin on the first bar of the asset on your chart.

I decided to code the script this way so statistics remain fixed when moving from asset to asset!

To compensate for this limitation, I included a label plot and background color change at the first session in which all assets in the portfolio had at least one bar of price data. You can adjust the calculation start date to the date portrayed on the label to test al possible price data!

The statistics table, and the performance lines, can be hidden in the user input section.

I plan on putting a bit more work into this script. I have some ideas on what to include; however, any input is greatly appreciated! If there's something you would like me to include please let me know.

@scheplick mentioned me in a script he recently coded:

My inspiration came from his script! I thank him for that!